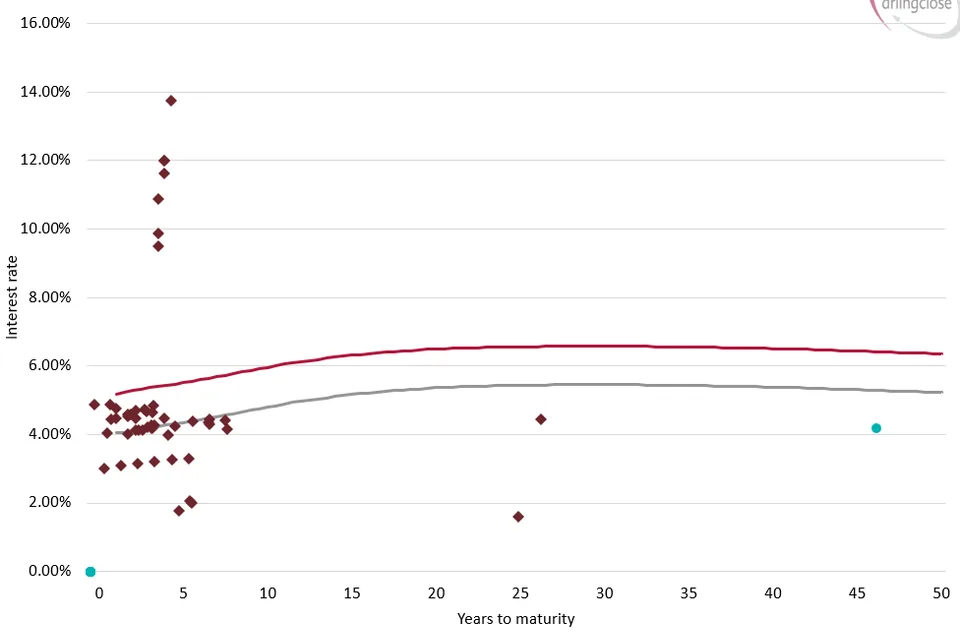

For local authorities, selecting the most appropriate debt structure is a key treasury management decision. The PWLB offers three main loan structures: maturity, equal instalments of principal (EIP), and annuity. Using these structures, we are then able to assess how each repays interest and principal in a different way. It is important to understand and compare the features of each option before deciding which structure is most suitable.

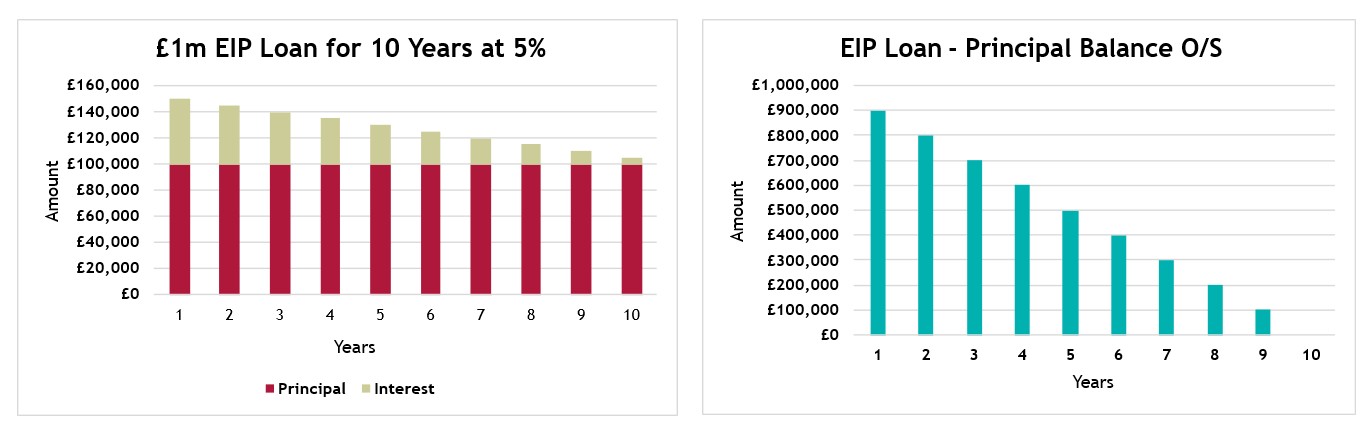

Under an EIP structure, the principal is repaid in equal amounts. Interest is charged on the outstanding balance, so the interest element falls steadily over time. The chart shows this clearly: payments are highest at the start and gradually decline as the debt is repaid. For local authorities, EIP borrowing can help reduce interest rate risk and refinancing risk, as the outstanding principal gradually reduces rather than falling due in full at maturity.

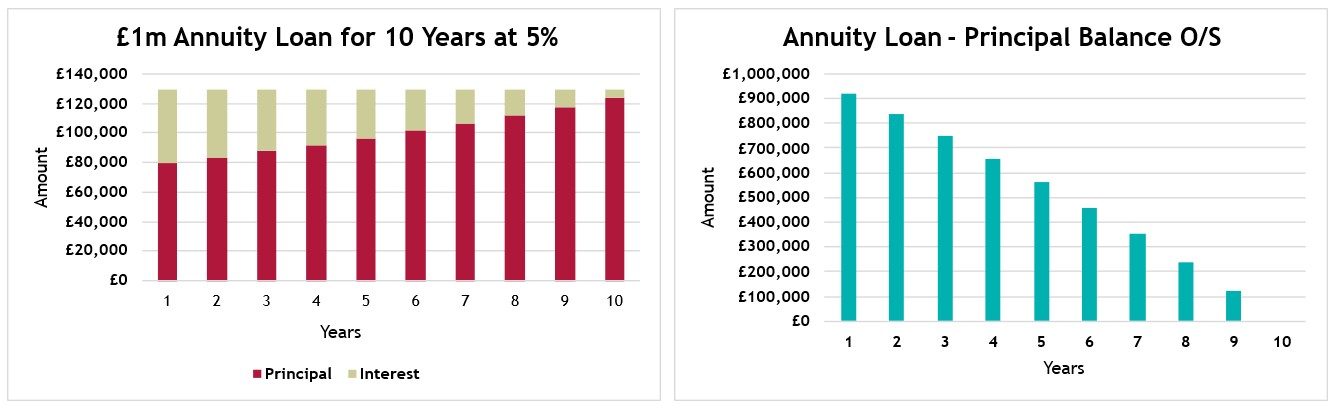

An annuity loan produces a broadly level payment over the life of the loan, which is a structure comparable to mortgage repayments. The balance between principal and interest changes over time: interest falls as the loan amortises, while the principal element increases. Compared with EIP, the outstanding principal reduces more slowly in the early years. The chart shows this as payments remain steady, with principal repayment rising gradually over time. This structure is attractive for local authorities as it provides predictable costs. The fixed repayment structure therefore makes cashflow forecasting a more simple and manageable process.

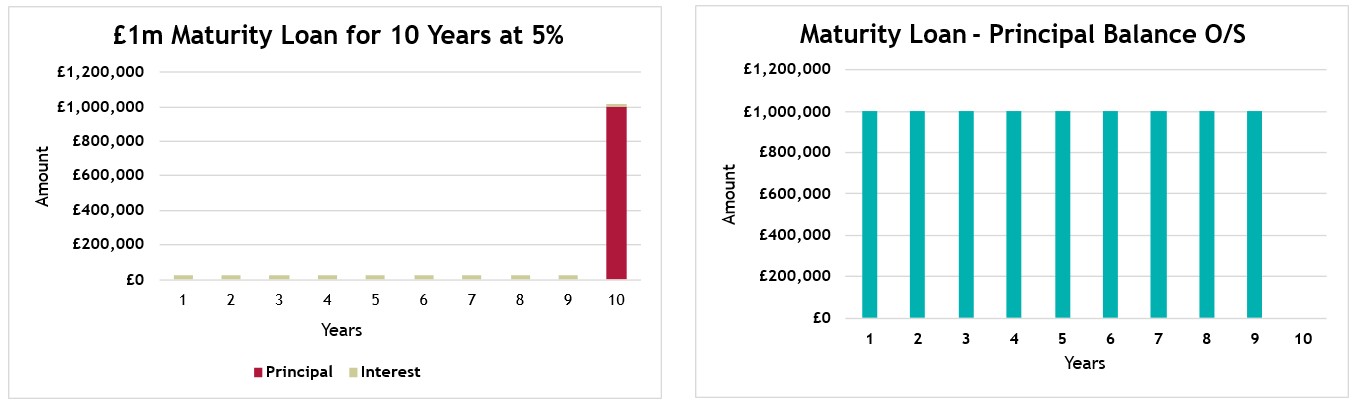

A maturity loan is interest only during the life of the loan, with the full principal repaid at the end. The charts below demonstrate this, with the full principal outstanding being maintained until the maturity date. One benefit of this loan structure is that the absence of regular scheduled repayments potentially reduces the need for regular refinancing. Maturity borrowing also provides flexibility, as the authority retains cash that would otherwise have been used for principal repayment. This debt structure means there is a reduced administrative burden, but it does mean the authority faces a single repayment date at maturity. This therefore can also create refinancing risks.

Each debt structure serves a different treasury purpose. For local authorities, the most appropriate approach will depend on the purpose of the borrowing, the life of the asset and appetite for refinancing risk. A balanced debt portfolio may include all three structures, and helps to manage risks involved with different debt structures.

If you would like to learn more about these services we offer at Arlingclose, please contact us on info@arlingclose.com.

Related Insights

11/06/2026

Are Higher Rates Making Debt Prepayment More Attractive?

What Is the Term Premium, and Why Is It High?

Is Your Debt Portfolio Ready for Local Government Reorganisation?