Throughout the current interest rate cycle, the term premium has been a hot topic in bond markets. This is understandable given its influence on long-term bond yields, the steepness of the yield curve, and borrowing conditions across the real economy. Despite its importance, the term premium is inherently unobservable, which makes it not only difficult to forecast but also challenging to estimate and analyse. Nevertheless, understanding the term premium, its effects, and its drivers is essential for investors and treasury professionals when assessing debt funding conditions, asset allocation, duration risk and fiscal risk.

Term premium is commonly defined as the additional yield required by investors to hold long-term bonds rather than short-term bonds, in other words, the slope of the yield curve. However, this is not strictly accurate. Longer-term sovereign bond yields can be conceptually divided into two components: the expected future path of short-term interest rates and the additional yield required by investors to compensate for the risk that interest rates may deviate from those expectations. The latter component is the term premium. Put differently, the term premium is the difference between the total yield and the average of expected short-term rates over the same horizon.

Unfortunately, the term premium is not directly observable and must be estimated econometrically. This is because expectations of average short-term interest rates are also unobservable. One might ask whether the fixed leg of an OIS provides a solution. While swap markets broadly capture investors’ short-term rate expectations, the fixed rate reflects the average future overnight rate implied by arbitrage free pricing once risk premia are embedded, not the market’s true central expectation of future rates. Investors require additional compensation for bearing duration and rate volatility risk, and that compensation is incorporated into swap rates. As a result, longer-term SONIA OIS rates contain their own time varying term premium. Because we only observe prices, which reflect risk adjusted expectations, the underlying physical expectations of short-term rates cannot be read directly from the curve and must instead be inferred empirically through an econometric term structure model that separates expected rates from risk premia.

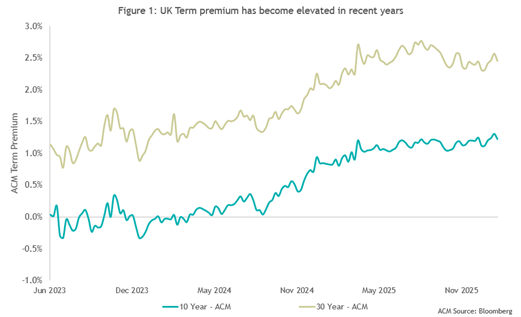

Several approaches exist for estimating the term premium, and while this insight does not examine their individual nuances, the ACM model is the most widely used. One trend is clear from Figure 1: the UK term premium has risen steadily over the past few years. As borrowers will have noticed, the yield curve is steep. Consistent with Figure 1, this steepness appears to be driven more by higher term premia than by changes in the expected path of short-term interest rates.

An increased term premium is not unique to the UK and is also evident in the US, France, Germany, Japan and other advanced economies in the post pandemic inflationary environment. That said, the UK’s term premia are generally higher than those of its peers, with the exception of France. Additionally, the UK’s sovereign curve was historically flatter than those of other advanced economies but has become steeper since the pandemic. This shift is not entirely attributable to the term premium, as concerns about persistent inflation have also lifted interest rate expectations. However, it does suggest that idiosyncratic features of the UK economy and financial system are contributing to higher term premia and a steeper yield curve.

The reasons behind the elevated UK term premia are multifaceted. First, regulatory and LDI driven demand for long dated UK gilts, particularly from pension funds, has historically been relatively inelastic, in that demand persisted regardless of the level of yields. This mechanically suppressed the compensation required for bearing duration risk and reduced the free float available to price sensitive investors, thereby compressing the term premium. However, the LDI crisis and the 2022 mini-Budget fiasco exposed the fragility of certain LDI structures and led to larger short-term liquidity buffers and lower leverage. Combined with the gradual closure of defined benefit pension schemes, structural demand for long-term gilts has declined. As a result, the marginal investor in long-term gilts is now more return sensitive and requires higher yields to compensate for interest rate volatility, inflation uncertainty, fiscal risk, and elevated supply, thereby contributing to a higher term premium.

Second, this dynamic has been further accentuated by the Bank of England’s quantitative tightening programme, which has increased the supply of long dated gilts and, by extension, the amount of duration that must be absorbed by the private sector. This has raised the compensation investors require for bearing that risk. In response to the impact on market functioning, the Bank has recently slowed the overall pace of QT and tilted gilt sales more towards shorter maturities, thereby reducing pressure on the long end of the curve and implying that, all else equal, the upward pressure on term premia arising from QT should ease over time.

Third, concerns surrounding fiscal sustainability have increased the term premium. Much like pension fund behaviour and quantitative tightening, fiscal unsustainability implies a higher net supply of duration in the future, with investors requiring greater compensation to absorb it. Fiscal pressures also create increased uncertainty around future taxation, public spending, inflation persistence, and the risk of financial repression. Even where outright default is not expected, the higher macroeconomic risk premium feeds into the term premium, thereby raising gilt yields. That said, the Debt Management Office has shown flexibility recently by skewing issuance more towards the short and medium maturities and reducing the proportion of long dated supply, which helps limit the immediate amount of duration risk placed with the private sector, and all else equal, should temper some of the upward pressure on long end term premia.

A fourth factor is the rise in geopolitical and political uncertainty across advanced economies. Ongoing conflicts, renewed trade disputes, and the potential for abrupt policy shifts following major elections, particularly in the United States, have increased uncertainty around global growth, inflation and fiscal trajectories. In that environment, investors require greater compensation for committing capital at long maturities, which has pushed up term premia across the UK and other sovereign bond markets.

Looking ahead, the term premium, which has remained elevated over the past year, could move in either direction. Its future path is inherently uncertain and will depend largely on the credibility of fiscal policy and the perceived sustainability of public debt, both of which are ultimately political matters.

From a historical perspective, both the 10- and 30-year UK term premia are currently above their long run averages since Bank of England independence in 1998. The 10-year term premium stands at 1.22%, compared with a long run average of 0.71%, while the 30-year term premium is 2.45% against a long run average of 1.06%. A simple mean reversion assumption would therefore imply some scope for decline from present levels. Although the 10-year measure remains below the extremes observed in the mid to late 1990s and around the financial crisis, the 30-year term premium is now close to the upper end of its historical range.

One scenario in which the term premium rises further is a marked deterioration in fiscal sustainability. Persistent deficits, changes in issuance strategy and investor confidence in the medium-term fiscal framework will all affect the compensation markets’ demand to hold long dated gilts. If the current Starmer government, or a successor, were to shift towards a less sustainable fiscal stance, term premia would likely increase. Conversely, if the government adheres to its existing plans or adopts a more fiscally conservative approach, the term premium could fall back towards its longer-term average.

The stance of the Bank of England is also significant. The pace and scale of QT, and any future return to QE in response to economic stress, will directly influence the net supply of duration risk held by the private sector. If, as widely expected, QT slows or stops as disinflation progresses, upward pressure on term premia should ease, allowing them to decline from current levels. However, a sustained reduction in term premia is unlikely to be supported by structural demand from pension funds, which has diminished. More broadly, global capital flows, inflation volatility, interest rate uncertainty, and geopolitical risk will continue to shape the equilibrium term premium.

From a treasury management perspective, a higher term premium translates directly into higher long-term borrowing costs, even if expectations for Bank Rate are unchanged. For borrowers, that raises the cost of locking in long dated funding and affects the economics of capital investment decisions. In a rising term premium environment, duration becomes more expensive to secure, and treasury strategy must weigh the cost of certainty against the risk of future rate volatility.

If fiscal credibility and the other factors described above remain in focus, elevated term premia may prove to be a persistent feature of the UK economy, keeping long-term yields high even if policy rates continue to decline.

As always, if you would like to see how Arlingclose can help support your organisation through economic forecasting and other treasury advice, please contact us at fwatson@arlingclose.com or 08448 808 200.

03/03/2026

Related Insights

How Will the National Housing Bank Change the Way Housing Associations Finance Development?