UK gilt yields have risen sharply since the start of the Iran conflict at the end of February. This has weakened expectations that Bank Rate cuts would steadily reduce borrowing costs during 2026.

The main driver has been inflation risk. Higher energy prices, concerns over oil and gas supply routes, and renewed pressure on transport and household costs have shifted market expectations, with a rate hike now seen as more likely than a cut.

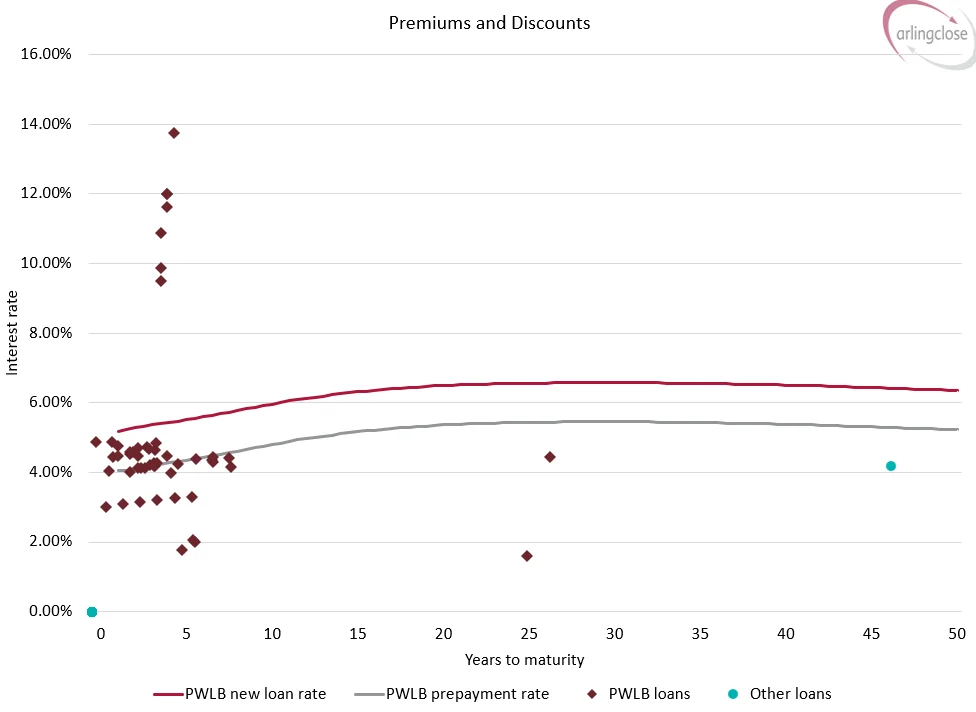

For local authorities, this matters because PWLB rates are priced as a margin over gilt yields. Higher rates increase the cost of new borrowing, but they can also improve the economics of prepaying existing fixed-rate debt.

Where an authority holds older fixed-rate loans with coupons below current premature repayment rates, prepayment may be possible at a discount. The PWLB may effectively compensate the borrower because the old loan is less valuable in today’s higher-rate environment.

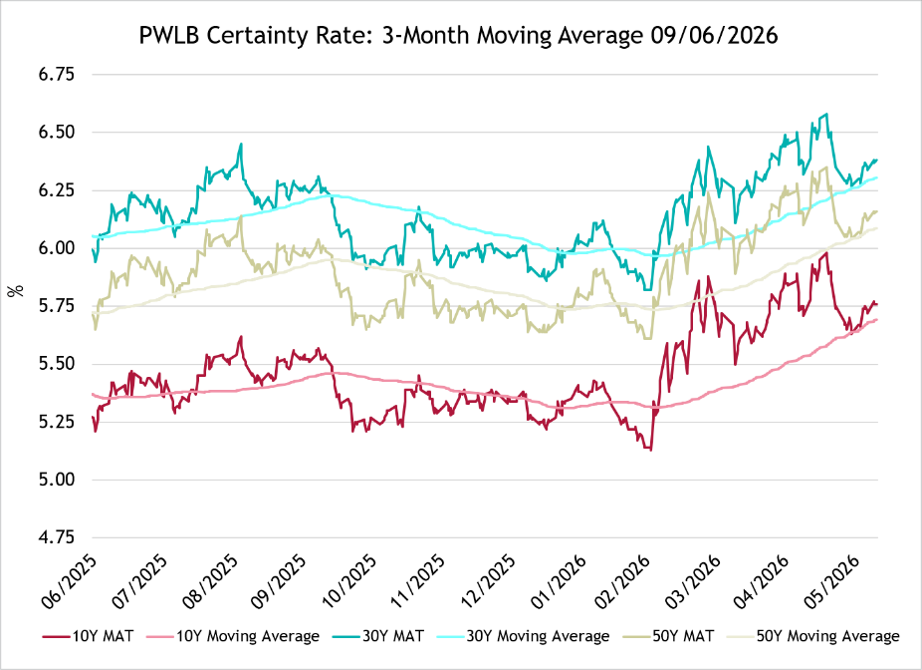

The recent PWLB Certainty Rate moving average chart shows this clearly. The 10-year, 30-year and 50-year rates have all moved higher since March, with current rates sitting above their recent three-month moving averages. This increases the likelihood that selected loans can be prepaid at a discount, particularly where original coupons are materially lower than current repayment rates.

This does not mean every prepayment is attractive. A discount on day one is only a small part of the calculation. Authorities need to assess replacement loan costs, the amortisation of any discount, short-term cash effects, accounting treatment, maturity profile and the impact on the liability benchmark.

However, the opportunity is real.

Last year, Arlingclose supported a Council through a targeted debt prepayment and refinancing exercise when gilt yields were elevated due to UK fiscal credibility concerns ahead of the November Budget. The work identified loans that could be prepaid at a discount and refinanced on terms that generated measurable savings. Benefits were unlocked for both the General Fund and the Housing Revenue Account, while the authority’s debt maturity profile was also improved.

Authorities do not necessarily need surplus cash balances to benefit from this type of opportunity. Prepayment can be combined with refinancing, using replacement borrowing structured to meet the authority’s objectives. That might mean securing revenue savings, smoothing the maturity profile, reducing refinancing risk, or managing the accounting outcome.

The accounting treatment is important. Depending on the lender, timing and cash flow profile of the replacement borrowing, a transaction may be treated as an extinguishment or as a loan modification. Neither is automatically right or wrong. The preferred treatment depends on what the authority is trying to achieve.

Nor is this limited to PWLB debt. Commercial loans, LOBOs and other market borrowing can also present opportunities. Unlike PWLB repayment rates, which are formula-driven, private sector lender terms may be negotiable.

The current market backdrop makes this a sensible time to review debt portfolios. Elevated yields do not guarantee savings, and market conditions can change quickly.

Arlingclose has live tools to support this analysis, including our Debt Rescheduling Calculator, which models the revenue, accounting and present-value impact of repaying fixed-rate borrowing, with or without replacement loans. The final outcome will depend on live rates, loan terms, accounting treatment, execution timing and the authority’s wider treasury strategy.

If you would like to discuss whether current PWLB or market loan conditions create an opportunity for your authority, including options to smooth the maturity profile of debt, please contact pmarshom@arlingclose.com.

09/06/2026

Related Insights

What Should Treasury Teams Do Now to Prepare for LGR?