PWLB – a cash cow?

It was recently suggested that the Government may reverse its recent decision to increase the pricing of PWLB loans once it realised the lost income it would suffer from less PWLB loan activity. May be.

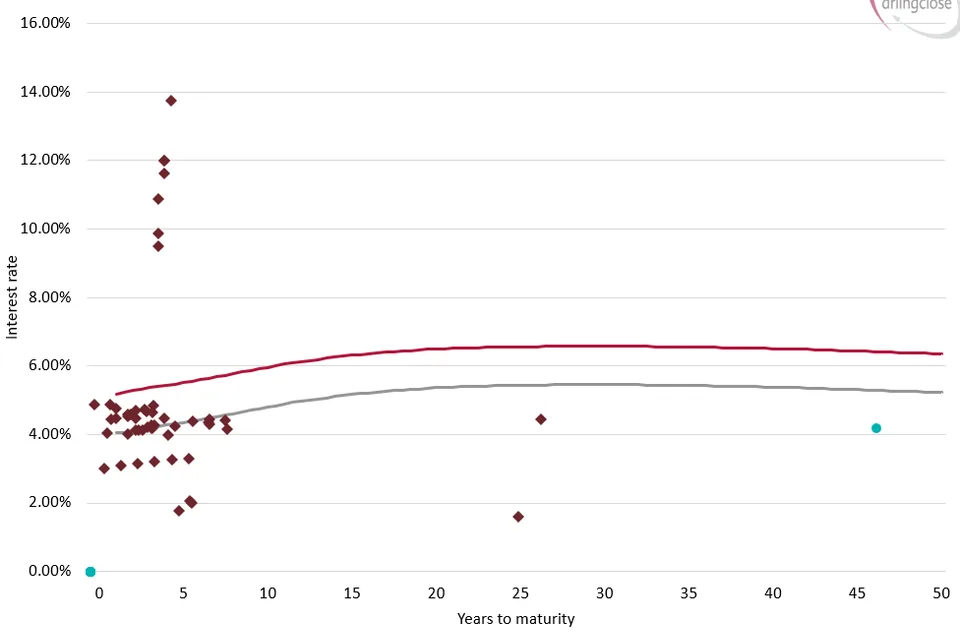

UK local authorities (excluding town and parish councils) borrowed £13bn in the twelve months ending 31st October 2019 almost entirely at the Certainty Rate. A margin of 80bps (0.8%) over Gilts equates to an annual local authority funded boost to HM Treasury coffers of just over £100m.

The weighted average life of the £13bn of PWLB loans borrowed by local authorities was just over 30 years.

PWLB fee income on the £13bn of borrowing alone amounted to £4.6m and with the net cost of operations of the entire Debt Management Office reported at £18m we roughly estimate the annual cost of the PWLB operations to be £0.8m.

Our assessment, therefore, would be that HM Treasury is less sensitive to the risk of income foregone since it has already locked in a reasonably rich return.

HM Treasury – First amongst equals

The policy shift was driven by what was deemed to be excessive borrowing on commercially orientated activities rather than prudent treasury management. The balance between these two activities has become somewhat blurred in recent years.

But there is no denying that a number of authorities have found themselves classified as high profile through the scale and nature of their borrowing activities and this has been matched in some instances by a somewhat combative approach towards the principles of financial codes and capital finance regulations. It was inevitable that this would not go unnoticed or unchecked by HM Treasury although the adopted draconian response was disappointing.

But we are where we are and there are new horizons to consider as a consequence of the sharp increase in PWLB rates.

Local authorities are being bombarded with offers of alternative and cheaper borrowing opportunities from a variety of new sources and means. It is not long since the last dose of public scrutiny and criticism regarding the widespread use of an alternative to the PWLB, in the form of LOBO loans, was levied so are there steps that can be taken to ensure that one is not simply replaced by another this time?

The answer is a resounding yes.

Funding Options

Whilst the PWLB has become significantly more expensive, the underlying fundamentals associated with treasury management, the prudential code and capital financing remain. There is now just the potential for greater choice in funding sources and structures that may provide an attractive alternative to the previously go-to option of the PWLB.

But caveat emptor remains a key consideration as is the need to detach the link between proposals that promise everything and the reality of the possible.

Arlingclose Funding Options

At Arlingclose we are positioned as your independent eyes and ears on your interaction with the financial markets.

We believe that the right way to explore these new horizons is to objectively assess what is known and what is possible in a logical appraisal of funding options for your specific authority and circumstances.

Looking at your current funding requirements and analysis of optimum mixture of funding solutions against robust risk assessments will ensure that any exploration of available alternatives is focused and relevant to your circumstances. It will be supplemented with detailed credit assessment and funding structure requirements including potential hedging strategies. Only then will we advise on the best route to market to ensure resources are maximised and will provide realistic indicative pricing, costs and a detailed savings analysis alongside any accounting treatment of the alternatives under consideration.

There are undoubtedly opportunities to secure new funding solutions that provide benefits in terms of risk management and lower costs than the PWLB. But we know that the increasingly wide range of offers emerging in the local authority market provide little in the way of clarity.

Far better, therefore, to take demonstrable steps to independently assess what is claimed and what is possible. It will ensure that the desired outcome is realistically achievable.

We will, of course, be discussing funding strategy and alternatives at current and forthcoming strategy meetings but to discuss our specific Funding Options Service then please do not hesitate to contact our Debt Advisory team on advisory@arlingclose.com or 08448 808200