Inflation has arguably been the most important and persistent economic problem facing policy makers globally over the past half-decade. It pulled interest rates up and out of the zero interest rate era, contributed to political instability by eroding trust in institutions, and intensified financial pressures on businesses, governments, local authorities and third-sector organisations alike. Although inflation has fallen back from its 2022 peak, it has remained persistently and materially above the 2% level targeted in the euro area, UK and US, leading many to question whether something more structural has changed.

In this context, a structural shift means an economy is generally more prone to generating above-target inflation, alongside a higher risk of inflation rates remaining elevated after a price shock, suggesting monetary policy needs to be tighter on average to keep inflation on target.

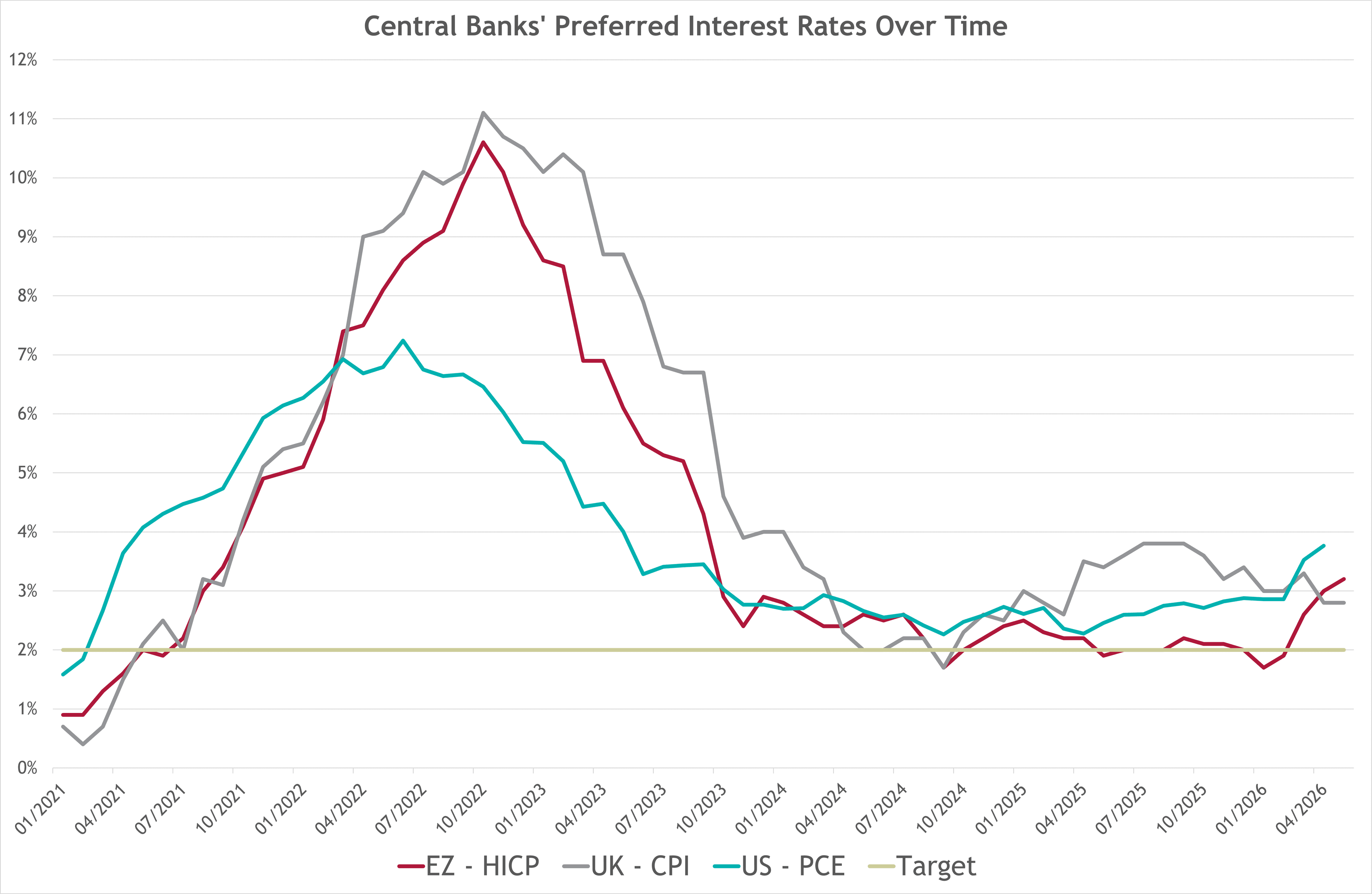

How has inflation changed over the past 5 years?

The broad shape of the story in the chart below will be familiar to most, with inflation climbing steeply from early 2021, spiking in 2022, and then falling back over the following two years before stabilising above target. UK and euro-area inflation both returned to 2% in 2024, only for the UK to turn higher almost immediately due to fiscal policy measures and energy price base effects. More recently, euro area inflation has been lifted by the energy cost effects of the Iran conflict, after persistently weak economic activity since 2024 had contained pricing pressures. Notably, US inflation has been above the 2% target since 2021, when large Biden-era fiscal stimuli added materially to demand at a time when global supply chains were already stretched.

In the UK and US, the disinflation since the peak in prices has been real but incomplete, although the US never suffered the same prolonged inflationary peak as the UK. The most recent UK CPI reading was 2.8% in May 2026. Headline inflation has hovered around 3% through much of 2026, and most independent forecasters surveyed by HM Treasury expect it to push back up to roughly 3.5% by Q4 2026, primarily driven by the increase in the retail energy price cap in July following the Iran War’s effect on wholesale gas and electricity prices.

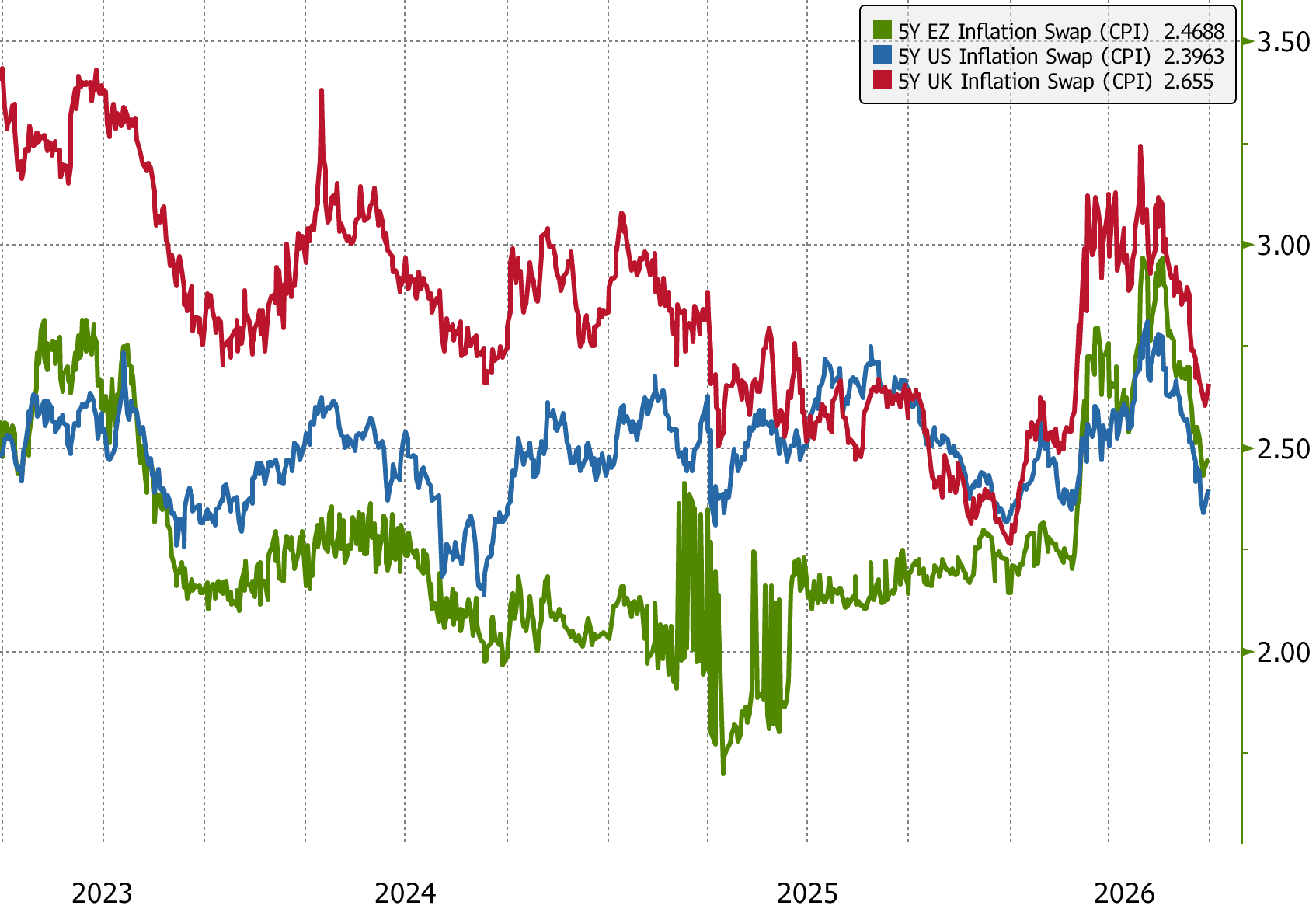

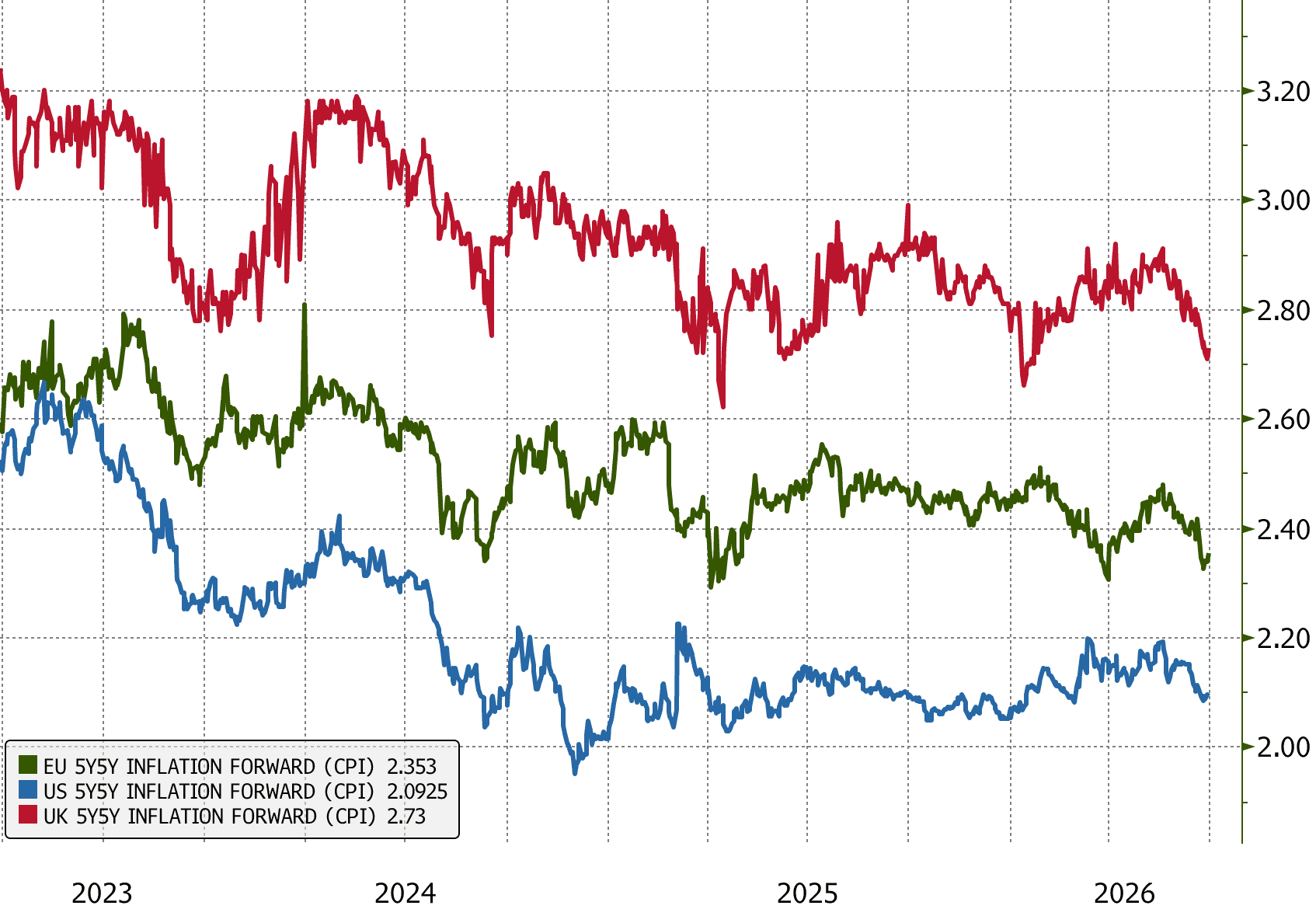

Despite the Iran War being a global shock, medium-term market-implied inflation expectations shown in the inflation swap rate figure below are pricing higher UK inflation than elsewhere and have done so for most of the past 3 years. Similarly, the 5y5y CPI swap rate shows the market’s expected average inflation rate over the five-year period that begins five years from now and is a useful measure of whether investors think inflation will return to target over the medium term or remain structurally higher. On that measure, the UK continues to stand out. Market pricing implies that medium-term UK inflation expectations remain above those in the US and euro area, suggesting investors still attach a premium to the UK’s inflation risk. This is reasonable, given the UK’s heavy reliance on food and energy imports and its more inflation-prone recent history. But looking beyond the most recent energy shock, what reasons do analysts have to view the UK as uniquely susceptible to higher inflation?

5-Year CPI Swap Rates

Source: Bloomberg

5y5y CPI Swap Rates

Source: Bloomberg

The case that something has structurally changed...

Several factors make the UK particularly susceptible to higher inflation over the medium term, although many of the same arguments also apply to other advanced economies:

1. Continued geopolitical uncertainty, combined with the UK’s relatively high dependency on food and energy imports, will lead to more frequent supply shocks, such as the current Iran War debacle, leading to more frequent bouts of inflation.

In a September 2025 speech, the BoE’s Megan Greene argued that monetary policymakers now operate in a world of recurrent relative-price shocks and supply fragmentation, rather than the unusually stable supply conditions of the Great Moderation. Her central claim is that supply shocks are likely to become more frequent, and that when they arrive simultaneously or in succession, they interact multiplicatively (e.g. pandemic recovery and Russian invasion of Ukraine).

Greene is not alone. The argument echoes points made by Jerome Powell, who has emphasised that supply-side disturbances have become more important drivers of inflation dynamics and a partial reversal of globalisation may expose central banks to larger and more persistent supply shocks than those of the Great Moderation.

In other words, a less stable geopolitical environment may make inflation more volatile and harder to return sustainably to target.

2. With government debt across advanced economies now at levels not seen outside wartime, the cost of servicing debt has become a real constraint on policy. One possible response, still unlikely but growing in relevance, is to let inflation run a little hot while holding real interest rates below the rate of growth, so that the real value of the debt is gradually eroded. This is what we mean by financial repression and inflation bias. It can work through regulation that nudges institutional money into government bonds, through a greater tolerance for above-target inflation at the central bank, or simply through a reluctance to keep rates high enough for long enough. Either way, heavy indebtedness tilts the balance of risks towards inflation rather than away from it.

The UK is not obviously there yet. The Bank of England’s continued quantitative tightening, despite the pressure it can place on gilt yields and debt servicing costs, suggests monetary policy is still being run primarily with inflation control in mind rather than as a tool of debt management. That pushes back against the strongest version of the financial repression argument. Even so, higher debt makes the political and fiscal cost of tight monetary policy more visible, which may matter more in future downturns or periods of market stress.

3. For three decades, the integration of low-cost producers, China above all, into global supply chains exerted a powerful and persistent downward pull on goods prices. In effect, it imported disinflation into the UK and other advanced economies. As labour and other production costs increased in these producers, the disinflationary effect has ebbed. More recently, China’s weak domestic demand and excess industrial capacity have reduced its export prices in some sectors, but the politics around this trade has changed as tariffs, trade restrictions and industrial policy in the US, EU and UK show that cheap imports are increasingly being weighed against security, resilience and domestic industrial objectives. Over time, that reduces the likelihood that globalisation will provide the same clean disinflationary impulse it did through the 2000s and 2010s.

4. Demographics may turn out to be one of the most significant structural forces despite unfolding more gradually. The argument is that the demography of the past forty years, a surging working-age population in Asia and eastern Europe, was disinflationary, because it expanded the world's effective labour supply and held wages down. That trend is now going into reverse. As populations age, the working-age share of the population shrinks, labour becomes scarcer and more expensive, and a growing number of retirees consume without producing. On balance that pushes inflation up rather than down. Ageing also adds to the fiscal pressures noted above, through higher health and pension spending, which reinforces the bias towards financial repression.

The case that it has not...

The counterargument is that the recent overshoot is better understood as a sequence of one-off level shocks working their way through the system and that the underlying inflation process and the structural factors in the economy that lead to it are unchanged.

Unsurprisingly, this is the position that the Bank of England’s February 2026 Monetary Policy Report takes, judging that the risk of greater inflation persistence had continued to diminish, that lower near-term inflation should feed through into lower household and business expectations, and that new evidence on wage-setting suggested there had not been a structural shift that would keep adding to inflationary pressure.

And on r*, the rate at which inflation is at target and economic growth is at its potential level, applications of macroeconomic models such as Holston-Laubach-Williams point to materially lower equilibrium real rates and that the rise in long-term real yields reflects a higher term premium (the compensation for uncertainty in the path of future interest rates), rather than higher expected policy rates.

Where this leaves us

My reading is that the evidence does not yet support the strong claim that the UK is moving to a regime of structurally higher inflation. Expectations matter because they are the channel through which temporary shocks can become embedded in wages, prices and contracts. On that test the case for a regime shift is still not proven: expectations remain broadly anchored despite recent increases, the labour market is loosening, and the bulk of the post-2022 overshoot is still traceable to identifiable shocks such as energy, supply chain, policy and tax changes, rather than to a self-sustaining wage-price process. Prior to the latest energy shock, disinflation was moving fairly decisively back towards target. The most likely path is still a gradual return towards 2% as the economy processes the Iran shock and in the absence of further supply disruption, particularly given the weakness of the broader economy.

That said, the risk profile has changed. Demographic pressure, higher public debt, geopolitical instability and a less benign global trading environment all point towards a world in which inflation shocks may be more frequent and more difficult to look through from a monetary policy perspective. The practical implication is not necessarily that inflation will sit permanently above target, but that interest rates may need to be higher on average to keep inflation at target. That makes the old assumption of dependable, low and stable inflation much harder to rely on.

For more information on our economic forecasting services, market intelligence, or how to position your treasury strategy in a more uncertain inflation environment, please get in touch with fwatson@arlingclose.com.