For some time now, our proprietary bank bail-in analysis has formed one of the cornerstones of our creditworthiness service. In the years since the global financial crisis, the risks of depositing with a bank have changed and our analysis has changed with it.

We update the analysis in line with six-monthly bank financial reporting and with the latest update due to be published very soon, it’s worth having a refresher on what the bail-in process consists of and why it’s important from a credit perspective.

Bail-in allows a failing bank to be stabilised and recapitalised by imposing losses on shareholders and eligible creditors, rather than relying on public sector/taxpayer support (bail-out). Bail-in is no longer just a policy designed to end “too big to fail”, but a process to maintain banking services, recapitalise a firm, and impose losses on shareholders and eligible creditors in line with the creditor hierarchy.

Bail-in should be understood as a transaction with defined stages, legal certainty, and operational infrastructure. The objective is not simply to absorb losses, but to ensure continuity of critical banking services while restoring the viability of the bank.

For systemically important firms, bail-in is expected to be the primary resolution strategy. Traditional insolvency is unlikely to be suitable given the potential disruption to financial stability. Instead, resolution is designed to take place over a short timeframe, with key actions often executed over a “resolution weekend” ahead of market reopening. But resolution is only credible if it can be delivered quickly and effectively.

The credibility of bail-in relies on firms maintaining sufficient loss-absorbing capacity through Minimum Requirement for Own Funds and Eligible Liabilities (MREL). These instruments are designed to absorb the losses, support the recapitalisation and stabilise market confidence.

MREL is not simply a regulatory buffer but the primary tool (i.e. the first liabilities used in a bail-in) through which a bail-in is executed. The structure, distribution and investor base of these liabilities therefore has direct implications for how a resolution proceeds.

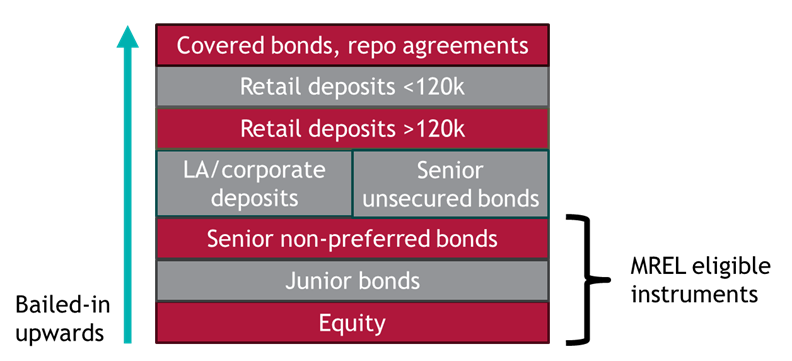

For investors and depositors, this reinforces the importance of understanding where instruments (such as their deposits) sit within the creditor hierarchy and how they might be treated in a bail-in event. A simplified graphic is shown below, with bail-in losses starting from the bottom and going upwards.

Independent valuation is key to the process. It determines both the scale of losses and how much recapitalisation is required, forming the basis for how losses are allocated across stakeholders.

This valuation process is one of the most important safeguards in the resolution framework and ensures that no creditor should be worse off than they would have been in insolvency. Resolution credibility therefore rests as much on valuation discipline as on legal powers.

For market participants, this introduces an element of uncertainty in timing but also provides a degree of legal and economic protection. The robustness of valuation is therefore central to maintaining confidence in the process.

Once a resolution is triggered, control of the firm changes quickly, and the “resolution weekend” is where the process becomes visible to markets. Typically, shareholders are effectively wiped out or diluted, and relevant liabilities are written down or converted. Trading and settlement in affected instruments are suspended or cancelled as needed.

Rather than immediately issuing new equity to creditors at the point of resolution, Certificates of Entitlement are used. These ‘interim’ instruments represent a future claim, typically in the form of shares. Creditors receive certificates representing their entitlement, which can be traded during the bail-in period.

This allows time to finalise valuations, determine the recapitalisation needed and appropriate exchange ratios, as well as enabling price discovery during the resolution period and providing operational flexibility in managing the restructuring. From a market perspective, this reflects a practical approach to balancing speed with accuracy.

Bail-in is not the end of the process, but the beginning of a restructuring phase. During this period, the firm operates under close oversight while a business reorganisation plan is developed.

This plan must demonstrate how the firm will return to long-term viability, addressing the causes of failure and setting out a credible path forward. The eventual allocation of equity to creditors, which is based on exchange ratios determined by the Bank of England, marks the transition from stabilisation to the intended outcome of re-privatisation.

Once this is achieved and the recapitalised firm is returned to private ownership, control passes back from the resolution authority, trading resumes, and the firm exits resolution. This reinforces the overarching objective of bail-in not to nationalise failing banks, but to reset them.

The implication for our credit analysis is straightforward. Credit risk must be assessed on the basis that losses can and will be imposed. The focus should therefore be on robust counterparty selection, clear understanding of your position in the creditor hierarchy, and disciplined risk management.

If you want to find out more about our bail-in analysis or any aspect of our creditworthiness service, please contact us at info@arlingclose.com

27/04/2026

Related Insights

How to measure local authority creditworthiness?

EU Bank Failure Reform: Why Does Depositor Hierarchy Matter?

How Do Credit Ratings and CDS Spreads Help Us Assess Creditworthiness?