Local authorities are generally extremely creditworthy given the statutory framework effectively prohibits default. It does this by providing lenders recourse to council revenue raising powers in the event on default and is underpinned by access to the Public Works Loan Board as a lender of last resort. There is also no history of a local authority defaulting on a loan in the UK. For these reasons, 99% of UK local authorities are on Arlingclose’s approved counterparty list.

Arlingclose’s Financial Strength Scores provide a consistent and transparent assessment of the relative financial resilience of UK local authorities. First launched in 2018, the scores were developed in response to increasing divergence in credit risk across the sector, driven by prolonged funding pressure, rising commercial activity and, more recently, a series of section 114 notices. The scores are designed to support lenders and counterparties in meeting the expectations of the CIPFA Treasury Management Code, particularly the requirement to maintain well documented and up to date assessments of counterparty standing.

Each local authority is scored out of 100 using ten financial indicators, with individual indicator scores ranging from 0 to 10. The indicators span four core areas: debt, interest cost, income flexibility and reserves. Higher scores indicate stronger financial positions. The dataset covers 467 UK local authorities, excluding parish councils, national parks and some newly established combined authorities. Where bodies report on a consolidated basis, such as the Greater London Authority and its functional bodies, they are treated as a single authority for scoring purposes.

The indicators focus on financial characteristics that are commonly associated with elevated risk. These include higher levels of borrowing relative to income and reserves, greater reliance on short term or variable rate debt, higher interest costs, lower proportions of locally determined income, lower reserve levels and sustained use of reserves to support budgets. Unless explicitly stated otherwise, indicators include both General Fund and Housing Revenue Account data, ensuring that the full financial position of relevant authorities is reflected.

Scores are calculated by ranking all authorities for each indicator across the full dataset. The median authority receives a score of five for each metric, with stronger or weaker positions scoring proportionately higher or lower. The overall score is the sum of the ten individual indicator scores.

The methodology also applies adjustments to reflect risks not captured directly within the financial ratios. Deductions are made where authorities submit late or missing data, with penalties increasing the longer the delay persists. Further deductions are applied for recent section 114 reports, recognising that these represent material financial weakness that may not yet be fully visible in published statistics. Overall scores are floored at zero.

The methodology was refreshed in January 2024 to improve robustness and relevance. Measures of performance against budget were removed due to concerns over data reliability and UK wide coverage. Greater weight was placed on debt and reserves, reflecting the primary drivers of recent local authority failures, while the relative influence of interest and income flexibility was reduced. Where current year data is unavailable, earlier data is now used with an explicit negative adjustment, ensuring that all authorities remain scorable.

While the Financial Strength Scores are grounded in comprehensive national datasets, they are not intended to replace full credit analysis. Limitations in published data and differences in reporting practices remain. Instead, the scores provide a structured, comparative starting point for understanding relative financial strength across the local government sector, using a methodology that is transparent, consistently applied and aligned with observed sector risks.

Taken as a whole, Arlingclose continues to view the UK local authority sector as strong credit, supported by a robust statutory framework, central government borrowing as a backstop, and the high likelihood of government support in the case of failure. That said, financial pressures and differing responses to them mean that resilience is no longer uniform across the sector. Some authorities are demonstrably stronger than others. Financial Strength Scores are therefore not a judgement on the sector’s creditworthiness as a whole, but a practical tool for distinguishing relative strength and weakness within it, enabling proportionate, informed and well evidenced treasury decisions.

iDealTrade users can access their own Financial Strength Score by logging onto the site. The score of any counterparty that you lend to is also revealed before deal completion. If you would like more information on how you can access Financial Strength Scores outside of iDealTrade, please contact jscottsoane@arlingclose.com.

16/12/2025

Related Insights

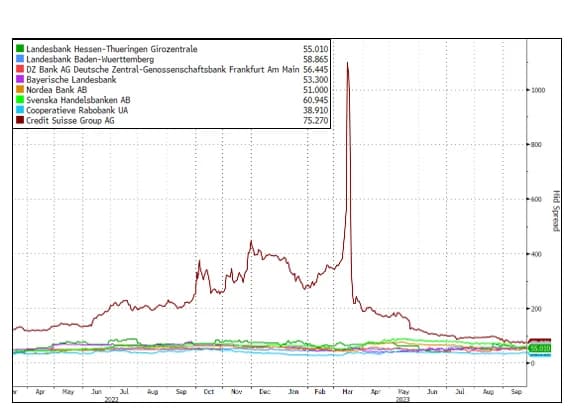

How Do Credit Ratings and CDS Spreads Help Us Assess Creditworthiness?