For quite some time now we have held a positive view of the creditworthiness of the UK local authority sector. Despite what the press might otherwise suggest, no authority is ‘going bust’ nor can they.

In general, local authorities are highly creditworthy institutions. Their standing is backed by various legislative and structural safeguards, notably the requirement to set a balanced budget, the section 114 and exceptional financial support regimes to correct budgets that become unbalanced, the ability to raise taxes, the Prudential Code controls on capital expenditure, and the presence of the PWLB as lender of last resort.

But the sector undoubtedly faces challenges. Some deemed of sufficient magnitude, such as SEND, to be national news. What has also made the news is the support being provided to help with some of those challenges, while other assistance such as exceptional financial support is almost at the point of being unexceptional given the number of councils which have agreed help.

Despite this support, many councils’ finances still remain under pressure, and in some cases have been for many years, but what does this mean for their creditworthiness and lending into the sector?

To clarify our general position, for over 99% of councils we consider their creditworthiness to be sufficiently strong that we are happy for our clients to lend to them.

However, this credit strength does not mean that further due diligence is not necessary, quite the contrary. When considering who to lend your money to, a creditworthiness assessment as part of a due diligence process is just as essential for local authorities as it is for other types of counterparties.

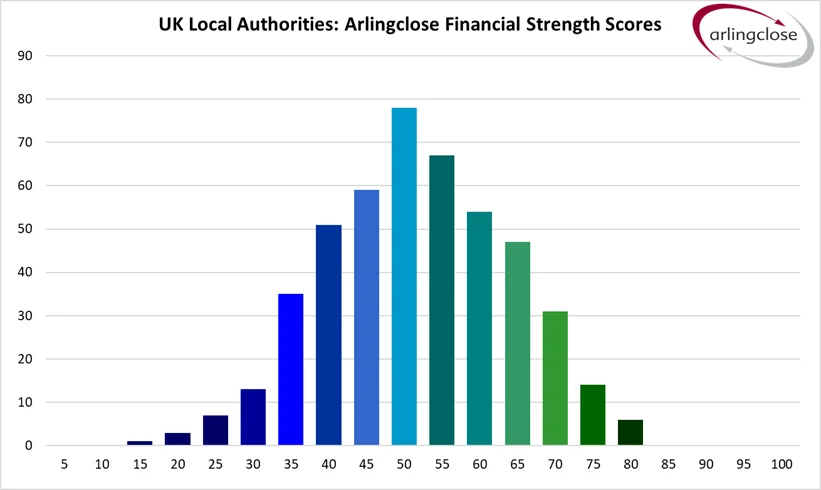

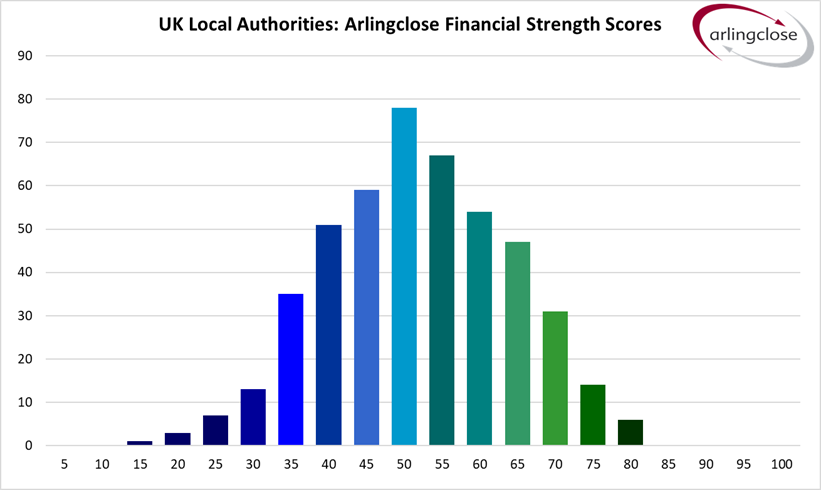

Given the number of local authorities in the UK, performing a detailed creditworthiness work on all of them would be quite the challenge. While do we do undertake more detailed work on a number of them, for the sector as a whole we have devised our Financial Strength Scores. The aim of these scores is to help clients make that initial decision-making easier by providing a clear and easily understandable measure of relative credit strength.

As we outlined in an earlier Insight, our Financial Strength Scores use a variety of publicly-available statistics to calculate a number of key metrics and provide a consistent and transparent assessment of financial resilience. They are scored between 0 and 100, with a score of 50 representing the median authority. A score lower than 50 indicates the authority has weaker metrics than the median, while over 50 indicates stronger metrics. We produce the analysis on a quarterly basis and an example of one of the charts we produce is shown below.

Based on the chart and the text above, readers may be thinking, well, all I need to do is lend to those local authorities within the darkest green bars. In an ideal world, that would be a great approach, however, the further to the right of the median an authority is, it will typically have a much lower requirement for debt (if at all) than those closer to and below the median, making those investment decisions a little more subtle and challenging.

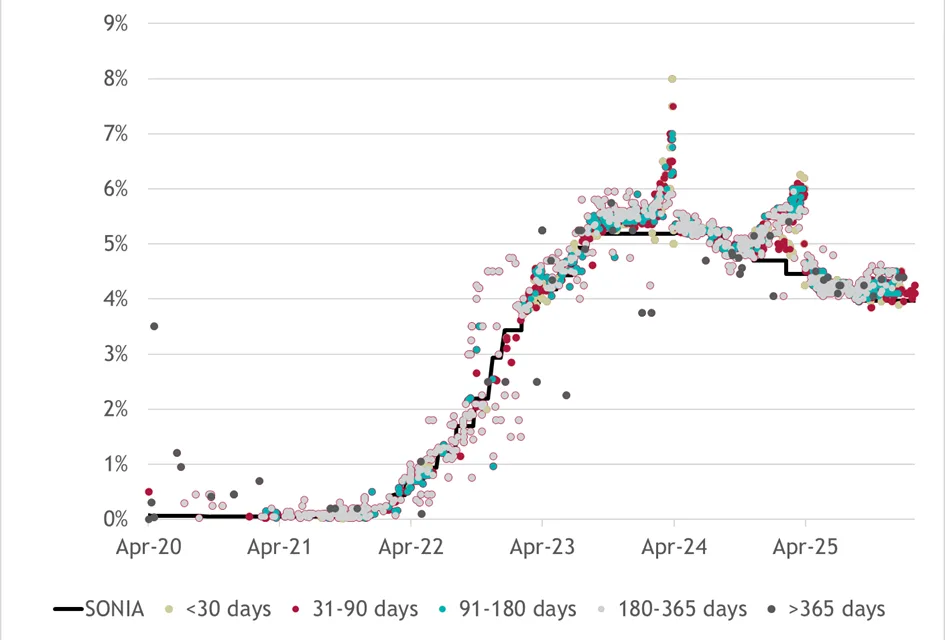

In addition to the sector’s credit strengths, another positive factor for investors are the returns that are available. Throughout most the year, returns are broadly in line with SONIA for shorter investments and 6-month cash rates for longer investments. However, market dynamics over the last few years have seen rates to spike in the few months ahead of the end of the public sector financial year in March as liquidity reduces and the need for cash increases.

Over the last few years, the spike in rates towards year end has seen yields of up to SONIA + 150bps on offer. Although these rates fall away after year end, while available they provide excellent opportunities to make outsized returns for a short period, whilst also helping provide liquidity to the market and those authorities requiring short-term fund to help cash flow over year end.

As was outlined at the very beginning, overall, we are supporters of the sector. Strong creditworthiness and good returns continue to make a compelling investment case in our view. While there are many challenges, we can provide support to clients looking to navigate some of these.

For anyone interested in finding our more about our Financial Strength Scores or any element of our local authority due diligence work and how it may help you, please get in touch at info@arlingclose.com.

02/03/2026

Related Insights

How to Measure Local Authority Creditworthiness?