The monthly public finance data is somewhat overlooked in the grand scheme of economic updates, it certainly doesn’t grab market attention the way that inflation or labour market data has in recent months. Nonetheless, the detail included in these data releases offers a good insight into the fiscal health of the country, an especially important consideration as the economy weakens and uncertainty is elevated.

Government borrowing has gone through a turbulent couple of years after the level of public sector net borrowing ballooned during the pandemic to support the economy at the same time as shutting it down to stem the spread of covid. Borrowing reached its highest point in March 2021 before it began to ease over the remainder of the year and through 2022 into 2023. However, recent months have seen this begin to worsen once again as the government is forced to borrow to support energy prices amid the cost-of-living crisis.

In April government net borrowing was reported as £25.6bn which was higher than the Office for Budget Responsibility’s (OBR) forecast for the period and was the second highest April borrowing figure since records began. This was despite growth in receipts over the period which boosted income but not by enough to offset the increasing costs of the energy support scheme, increases in benefit payments, and the ever-increasing cost of debt interest.

As inflation began to rise following the lifting on lockdown restrictions, there was talk of “inflating away government debt” which is where the value of existing debt is eroded by inflation, theoretically making it easier to pay down as inflation rises. Fast forward to today and that certainly has not translated into reality. Government debt interest payable was £9.8 billion in April 2023, the highest April figure since records began and £3.1 billion higher than the same period a year ago. Although inflation has certainly eroded the value of the pound, it has not got anywhere near outpacing the increase in debt servicing costs the government currently faces.

This is not the strong data that the government was hoping for in the first month of the new financial year. At this rate, the chancellor would overshoot the OBR’s full year borrowing forecast by roughly £3.2bn. The level of government debt currently sits at a worrying 99.2% of GDP at the end of April 2023, up from 96.8% in April 2022. This puts the UK in the top 5 G20 countries in terms of their debt to GDP ratio.

Overall, not much good news in the most recent set of public finances data to draw out. One area where there was good news came from the downward revision to last year’s level of government borrowing which was £2.1 billion lower than previous estimates suggested leaving it £15.3 billion lower than the OBR estimates. Borrowing for the year still stood at a total of £137.1 billion so these revisions were not enough to move the needle any great deal.

The outlook for public finances is relatively bleak going forward, with the outlook for economic growth set to slow to near recession levels over the remainder of the year and interest rates forecast to continue upwards until there is a material reduction in the level of inflation, the government may have to contend with falling tax income receipts at the same time as increasingly high debt repayments. Overall, it looks unlikely that the level of government debt will significantly fall any time in the next two to three years, despite reducing the budget being high on the government’s agenda.

Related Insights

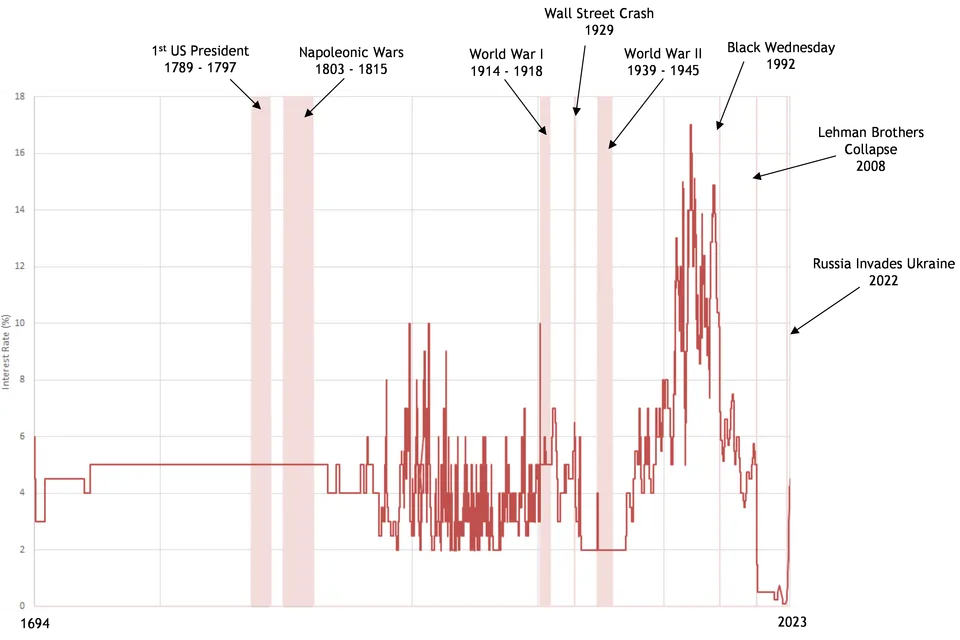

An Updated History of Base Rate