A liability benchmark is a long-term treasury planning tool that shows the level of external borrowing a local authority is expected to need, and when that borrowing is likely to be required. It compares an authority’s existing loans with its forecast need for debt, after allowing for usable reserves, working capital and the planned capital programme.

The liability benchmark was introduced into the CIPFA Treasury Management Code as part of the 2021 revisions, with a soft launch in 2022/23 before becoming part of the reporting framework from 2023/24. CIPFA introduced it to support better financing risk management of the capital financing requirement, and the indicator is expected to be shown in chart form for at least ten years, with material differences between the benchmark and actual loans explained.

The benchmark should not be viewed as either a borrowing limit or a forecast of future borrowing with certainty. It is better understood as a “debt requirement” line: the amount of borrowing that would be required if an authority were to avoid holding more cash than it needs while still financing its capital programme and maintaining adequate liquidity. Where actual debt is above the benchmark, the authority may have surplus borrowing or cash balances. Where actual debt is below the benchmark, it may need to borrow in future, or it may be deliberately using internal borrowing.

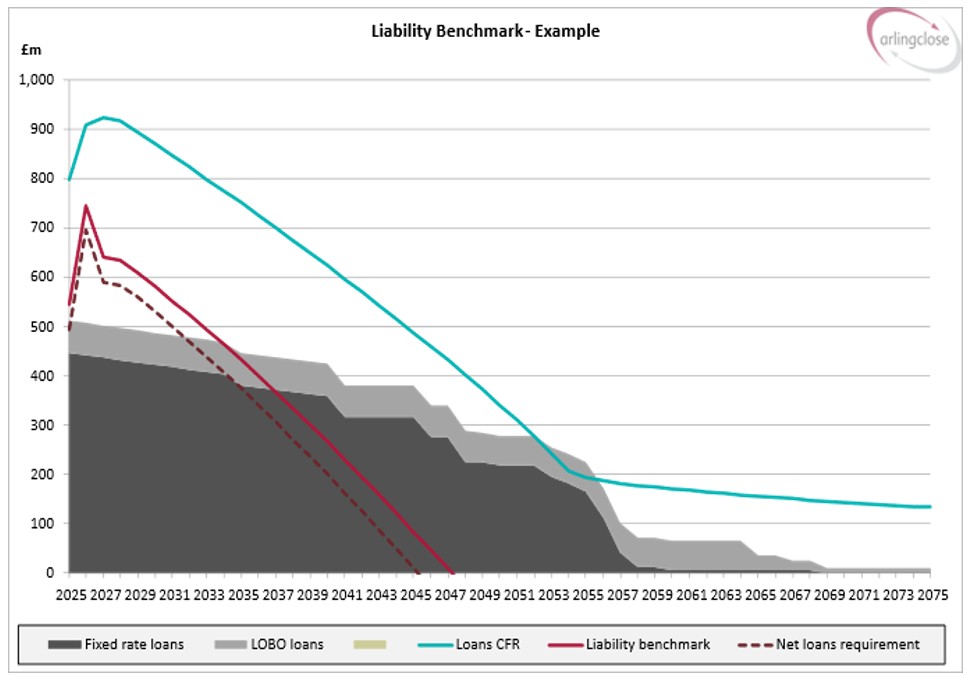

The illustrative chart below shows how the liability benchmark compares existing debt with the authority’s underlying need to borrow, helping officers and members assess the timing and scale of future borrowing decisions.

This is also why the liability benchmark is a prudential indicator. The Prudential Framework gives authorities freedom to borrow and invest, provided their plans are prudent, affordable and sustainable. The liability benchmark helps demonstrate that borrowing decisions are being made with reference to the authority’s underlying capital financing need rather than short-term market conditions alone. It links the capital strategy, treasury strategy, revenue budget and reserves forecast into one coherent picture.

The liability benchmark is normally reported in the annual Treasury Management Strategy Statement, alongside other prudential and treasury indicators. It may also appear in mid-year and outturn treasury reports, particularly where there have been material changes to the capital programme, reserves forecast or borrowing plans. Progressive authorities also use it internally throughout the year to support decisions on the timing, maturity and type of borrowing. The most useful benchmark is therefore not a once-a-year compliance chart, but a live model that informs treasury decisions as circumstances change.

Several key terms build up the model. The starting point is the capital financing requirement, or CFR, which represents historic and planned capital expenditure that has not yet been financed from grants, receipts, revenue contributions or reserves. The CFR is then adjusted for usable reserves and working capital, because these internal cash resources can reduce the immediate need to borrow externally. The model also includes the minimum revenue provision, or MRP, which is the annual revenue charge authorities make to reduce the underlying borrowing need over time; government guidance requires authorities to determine a prudent level of MRP.

The shape of the liability benchmark tells a story. A rising benchmark suggests future borrowing need, usually driven by a capital programme that exceeds available internal resources. A falling benchmark may indicate debt repayment, MRP reducing the CFR, capital receipts being applied, or reserves increasing. A large gap between actual debt and the benchmark should prompt questions: is the authority over-borrowed, under-borrowed, relying too heavily on internal borrowing, or holding cash for good reasons?

Used well, the liability benchmark brings discipline to treasury management. It supports proportionality, transparency and forward planning. Most importantly, it helps ensure that borrowing is linked to need, affordable over the medium term, and consistent with the authority’s wider financial strategy.

Arlingclose supports authorities in developing and interpreting their liability benchmark, helping to turn the model from a reporting requirement into a practical tool for borrowing, cash flow and treasury strategy decisions. To find out more, please email info@arlingclose.com.

16/06/2026

Related Insights

What Changes Are Required by the New CIPFA Code?

How Ready Is Your Treasury Strategy for the Fair Funding Review?

How Can Treasury Issues Be Prevented from Becoming Audit Failures Under the Local Audit Backstop?

-960x640.webp&w=3840&q=75)