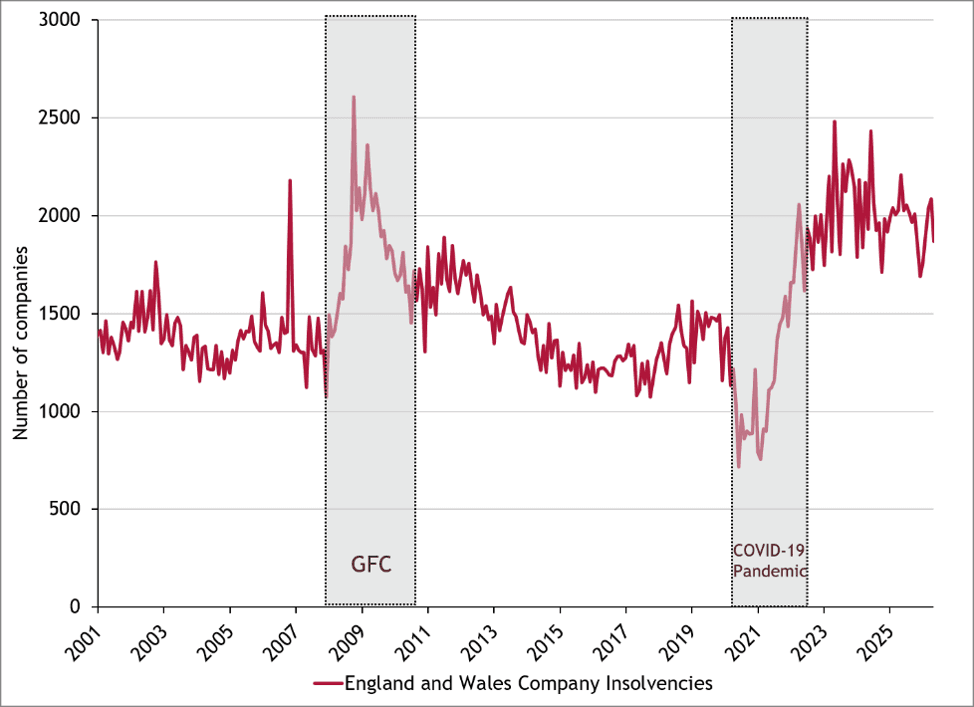

My previous insight on Contractor Due Diligence highlighted Carillion and ISG as examples of the risks organisations face when entering into major contracts without properly understanding a contractor’s financial resilience. That warning remains highly relevant in 2026. Company insolvencies in England and Wales remain materially above pre-pandemic levels, despite some monthly volatility.

The latest data continues to show a difficult trading environment. Registered company insolvencies in England and Wales stood at 2,087 in April before falling to 1,868 in May. The fall in May is welcome, but it does not change the broader picture: insolvencies remain high by historic standards, and the post-pandemic rise has not unwound.

Monthly insolvencies have regularly sat around the 1,700 to 2,500 range since 2022, underlining that this is a sustained higher-risk environment rather than a temporary spike.

Source: The Insolvency Service, Company Insolvency Statistics, May 2026.

The chart shows the scale of the problem clearly. Insolvencies rose during the Global Financial Crisis, before settling at lower levels through much of the 2010s. However, that period was supported by exceptionally low interest rates, which reduced debt servicing costs and helped many weaker businesses continue trading. Insolvencies then fell sharply during the pandemic, when government support and temporary creditor protections suppressed failures, before rising significantly from 2022 onwards as support unwound and higher inflation and higher borrowing costs placed renewed pressure on companies.

The construction sector remains particularly exposed. In May 2026, construction firms accounted for 16% of all insolvencies in England and Wales, with 281 registered construction business insolvencies. Over the 12 months to May 2026, 3,803 construction firms became insolvent, 18% higher than the equivalent pre-pandemic 2019 figure. Across all sectors, construction experienced the highest number of insolvencies over that period.

Many contractors are still dealing with the after-effects of fixed-price contracts agreed before the full impact of inflation, labour shortages, higher materials costs and higher financing costs had fed through. Even where inflation has moderated, margins have already been damaged, balance sheets have weakened, and working capital remains under pressure.

The survey data reinforces this. The S&P Global UK Construction PMI fell to 38.6 in May 2026, indicating the fastest fall in UK construction output for six years, with sharper declines in housing and commercial activity, shrinking order books, rising economic uncertainty, higher purchasing costs and widespread supplier delays.

Recent failures show that this risk is not theoretical. ISG entered administration in September 2024, affecting more than 2,000 employees and leaving a large number of public sector projects exposed, including school and prison schemes. Buckingham Group entered administration in 2023, with significant disruption across its project base and substantial amounts owed to its supply chain. Henry Construction Projects also entered administration in 2023, leaving thousands of creditors caught in the fallout. These cases underline a simple point: a contractor can appear established, active and commercially successful, but still carry financial weaknesses that are not obvious without proper analysis.

Contractor failure is not simply an accounting issue. If a contractor fails mid-project, the consequences can include immediate disruption, additional professional fees, re-procurement costs, contractual disputes and delayed service delivery. In practice, the organisation may end up paying more for the same project, with delivery pushed back and risk materially increased.

This is why financial due diligence should be undertaken before entering into significant contracts, not once warning signs have become obvious. Arlingclose’s contractor due diligence work can include an assessment of recent economic and sector conditions, review of financial statements, analysis of profitability, liquidity, gearing and interest cover, ownership structure review, indicative credit rating, default probability analysis, and practical recommendations on mitigations such as parent company guarantees, performance bonds, contractual protections and ongoing monitoring.

For further details on how Arlingclose can support due diligence on contractors, financial counterparties, grant recipients or business plans, please contact pmarshom@arlingclose.com.