As interest rates rise, an increasing number of local authority LOBO loans are being “called” by lenders, with notification given of their intention to increase the rate. Often, the rate proposed is very high, making the borrower’s option to prepay at par, rather than accept the higher rate, an easy choice.

However, while we have seen some rate revisions that are slightly lower than prevailing PWLB rates that look tempting, we urge caution. While the rate revision may look “cheaper” than PWLB debt, it only provides protection from further rate rises until the next option date. If rates subsequently fall, the Council is locked into an even higher rate. Beware the required accounting treatment too; accepting a new rate on a LOBO could present a costly one-year hit.

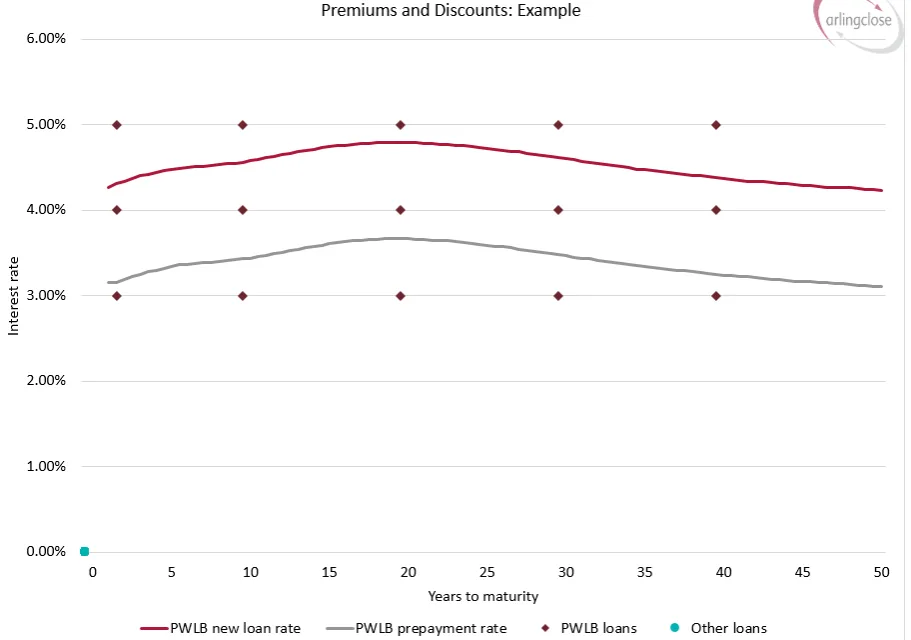

LOBO Cost / Benefit Analysis:

Comparing a LOBO with fixed rate debt ignores the value of the options, the theoretically unlimited upside to which a council is exposed. Although there is also a “borrower’s option” to repay, this is of little value as it forces refinancing in a higher rate environment, bringing with it increased cost. To compensate the borrower for the remaining options in a LOBO, the rate offered would need to be substantially lower than PWLB debt.

Indeed, with rates elevated and market volatility high, options are incredibly valuable to the lender, reflecting a significant potential cost to the borrower. To compensate for this risk, Arlingclose calculate a new LOBO rate would have to be more than 2% below PWLB rates on some loans. Arlingclose has yet to see a revised LOBO rate that is attractive to the borrower, reinforcing our view that most local authorities should exit these deals when given the opportunity.

The value of options, and risk relating to these loans, must also be considered when reviewing restructuring or repayment scenarios; you can’t directly compare against a fixed rate loan.

Banks typically have third party hedging costs to unwind, meaning they need to charge borrowers a premium to exit LOBOs early. However, as rates rise, these costs reduce and, as the bank’s break cost approaches £0, they can “call” loans at par, although some lenders may not call loans until market rates are substantially higher than the interest rate on the loan. The problem here is, the higher rates go, the higher the potential refinancing cost for those authorities that don’t have spare cash to repay debt.

The good news is that higher rates have reduced LOBO premium costs in absolute terms and some lenders are willing to negotiate on prepayment and restructuring loans. This can enable authorities to reduce risk and refinance debt whilst also achieving savings. A proactive approach to these loans is preferable, rather than responding to calls that can require loan refinancing with just two days’ notice, creating a liquidity headache and exposing councils to potentially costly refinancing.

Related Insights

Low Cost Funding and Interest Rate Risk Management