The PWLB has recently announced a reduction in the margin applied to loans that will be used to fund capital expenditure within the Housing Revenue Account (HRA), from the 15th June 2023 qualifying loans will attract a margin of 0.40% above Gilts, a reduction of 0.40% against the PWLB Certainty Rate (currently 0.80% above Gilts).

The PWLB interest rate has been a subject of discussion and concern in the UK's social housing sector for some time following hikes that have occurred over recent years which have made investment in council owned housing stock unaffordable when combined with the increase in the underlying Gilt yields.

In October 2019 following an attempt to reduce the amount of borrowing being carried out by local authorities, the Treasury made a significant change to the interest rate charged by the PWLB. The interest rate was increased by 1% above the then prevailing PWLB rate (effectively 2% above the Gilt rate), resulting in a substantial rise in borrowing costs for local authorities. This decision had a direct impact on HRA borrowing, making it more expensive for local councils to fund new housing developments or carry out repairs and maintenance on existing properties. The 2019 increase came hot on the tail of the abolition of the HRA debt cap in 2018 so the perceived freedoms to spend on housing from this measure was counteracted by an increase in borrowing costs.

Critics of the 2019 interest rate hike have argued that it would lead to a slowdown in social housing development and a decrease in the quality of existing housing stock. They raised concerns that local housing authorities would have to divert funds from other areas, such as maintenance and repairs, to cover the increased borrowing costs. This would potentially result in a backlog of maintenance issues and a decline in the living conditions for council housing tenants.

The provision of social housing in the UK has a long and complex history. The modern social housing sector began to take shape after the First World War when there was a severe shortage of housing, particularly for the working classes. The government responded by establishing local authorities with the responsibility to build affordable homes for rent. This led to the creation of council housing, which became the dominant form of social housing in the UK for several decades.

In the 1980s, the UK government introduced the Right to Buy scheme, which allowed council tenants to purchase their homes at discounted prices. While this policy was popular among tenants, it resulted in a reduction in the available social housing stock, as many properties were sold into private ownership. The funds generated from the sales were intended to be reinvested in new social housing, but this did not happen at a sufficient scale to replace the sold homes with much of the capital receipts raised returned to central government coffers.

In recent years, the UK has faced a significant housing crisis, with high demand for affordable homes and a shortage of supply. The government has introduced various initiatives to address this issue, including funding programs for social housing development. These programs aim to incentivise housing associations and local authorities to build new affordable homes and improve existing housing stock.

However, the funding for social housing has often fallen short of the levels required to meet the demand. The PWLB interest rate increase in 2019 further exacerbated this challenge by increasing borrowing costs for local authority housing providers.

In March 2020 the first acknowledgement of the pressures facing HRA related borrowing costs saw the introduction of a reduction of 1% for HRA loans meaning that the HRA rate was now back at the pre October 2019 margin. A similar reduction was applied to all other lending in November 2020 meaning that the distinction between HRA and General Fund borrowing was short lived, but not as short lived reduction of March 2012 which saw the lending margin reduced for one day to fund the HRA subsidy reform exercise.

This latest reduction puts the HRA at an advantage over the General Fund in terms of its cost of debt, but it is currently only in place for one year and with rates at now elevated levels it is too early to see if it boosts investment in local authority house building and maintenance and repairs.

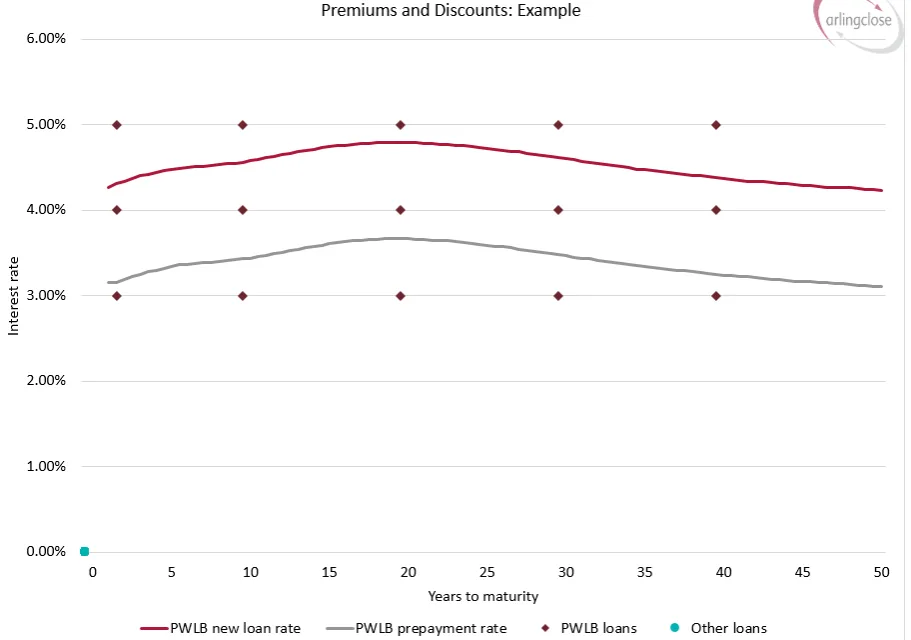

Higher interest rates do not always mean bad news for local authorities as it presents opportunities to repay debt, the reduction in HRA margins on new loans may present options for housing authorities to look at their existing HRA debt portfolios to identify restructuring options or even reexamine the debt pooling that has been in place since that 2012 subsidy reform.

At Arlingclose, we have significant experience in providing debt management advice linked to HRA capital investment and debt restructuring opportunities. Our online liability benchmarking and debt rescheduling tools give our clients the power to assess the impact of these issues on a real time basis, if you are a client and want to see how then get in touch with your client relationship manager, if you’re not currently a client and want to discuss HRA related issues then please get in touch to see how we can help you in managing your HRA debt portfolio.

Related Insights