Arlingclose produces an investment benchmark every quarter from its clients base, but what does this actually tell us and why is it important? Well the report covers all investments made for treasury purposes, including externally managed funds, however it excludes investments made for service purposes.

The report is a snapshot of our client base at the end of each quarter, and offers an insight into how the local authority investment market is evolving, in much greater detail and much timelier than other investment submissions, such as to MHCLG (Arlingclose’ 2 weeks vs 3 months!!). Therefore, the breakdown of local authority’s investment portfolios can be assessed and addressed in a vastly improved manner.

The investment benchmark looks at a number of different aspects of an investment profile; including absolute value, duration, liquidity, credit, bail-in risk, rate of return, fund volatility as well as including a comparison across the Arlingclose client base and within each type of authority.

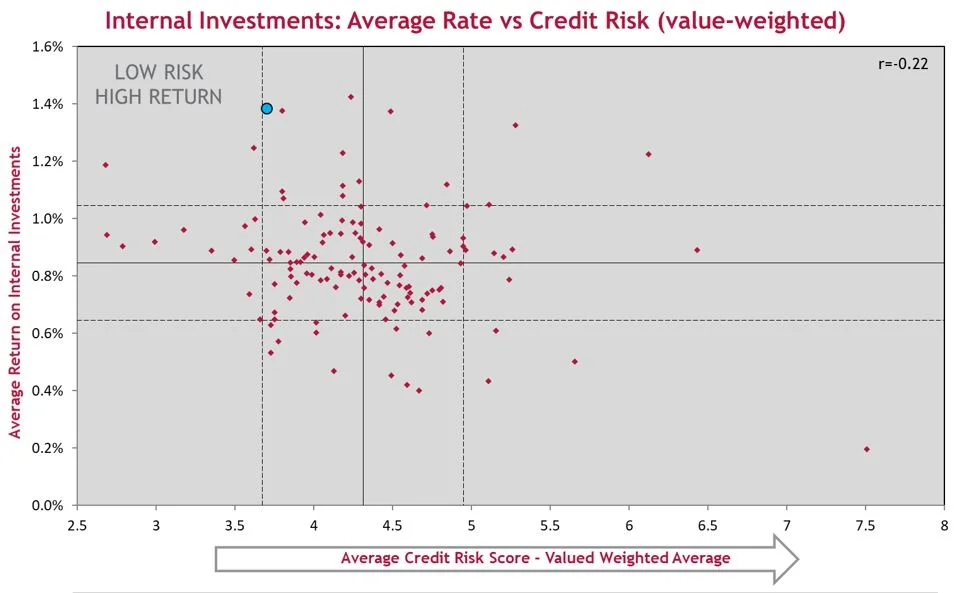

The trends from local authority returns are fascinating. LAs are each different and unique, and one size certainly does not fit all. Some LAs have significant liquidity requirements, some LAs have capacity to take on longer duration risk. Some LAs implement a laddering structure to deposits to increase their average days to maturity and increase return. One thing that remains certain through routine benchmarks is that there seems to be no correlation between taking on additional credit risk with increasing investment returns. And whilst banks certainly have a role to play in the financial system, they may not be offering enough return for the risk they pose.

Looking at the changes over time, those looking to diversify can mimic those at the more diverse end. Subsequently, it can be said those with externally managed portfolios tend to earn a higher rate of return on their investments. The current coronavirus crisis has had an impact on the capital values of these funds; however these are long term investments, and no one is compelling LAs to realise this loss at the moment. Therefore, it being an unrealised capital loss, it is an inconvenience to bear.

For LAs with significant liquidity requirements, it is surprising to see so many LAs with single counterparty exposure. For example a call account that earns a 0% rate of return, versus the slight uptick in return offered by a money market fund, which also offers diversification whilst still offering the liquidity Councils need.

A large and growing portion of portfolios recently has been the prevalence of government deposits and local government deposits. It is a brilliant thing that locals are happy to lend to each other during this crisis, the total amount of LA lending has increased dramatically. These deposits are not exposed to bail-in and offer a higher rate than deposits with the DMO, whose rates have often barely covered the CHAPS fees involved.

Lastly corporate and covered bonds and registered providers are a diversifier, but often small part of some portfolios. Direct bond exposure can offer the potential for an increase in rates and diversification with the potential to sell bonds on the market as and when necessary or hold to maturity. Registered providers can provide RCFs and deposits with a potentially higher return on investment.

For enquiries on any of the above aspects on local authority treasury investments, please contact the Arlingclose team on treasury@arlingclose.com. If you would like to discuss your investment benchmarking report, please contact your client director, contact details here.