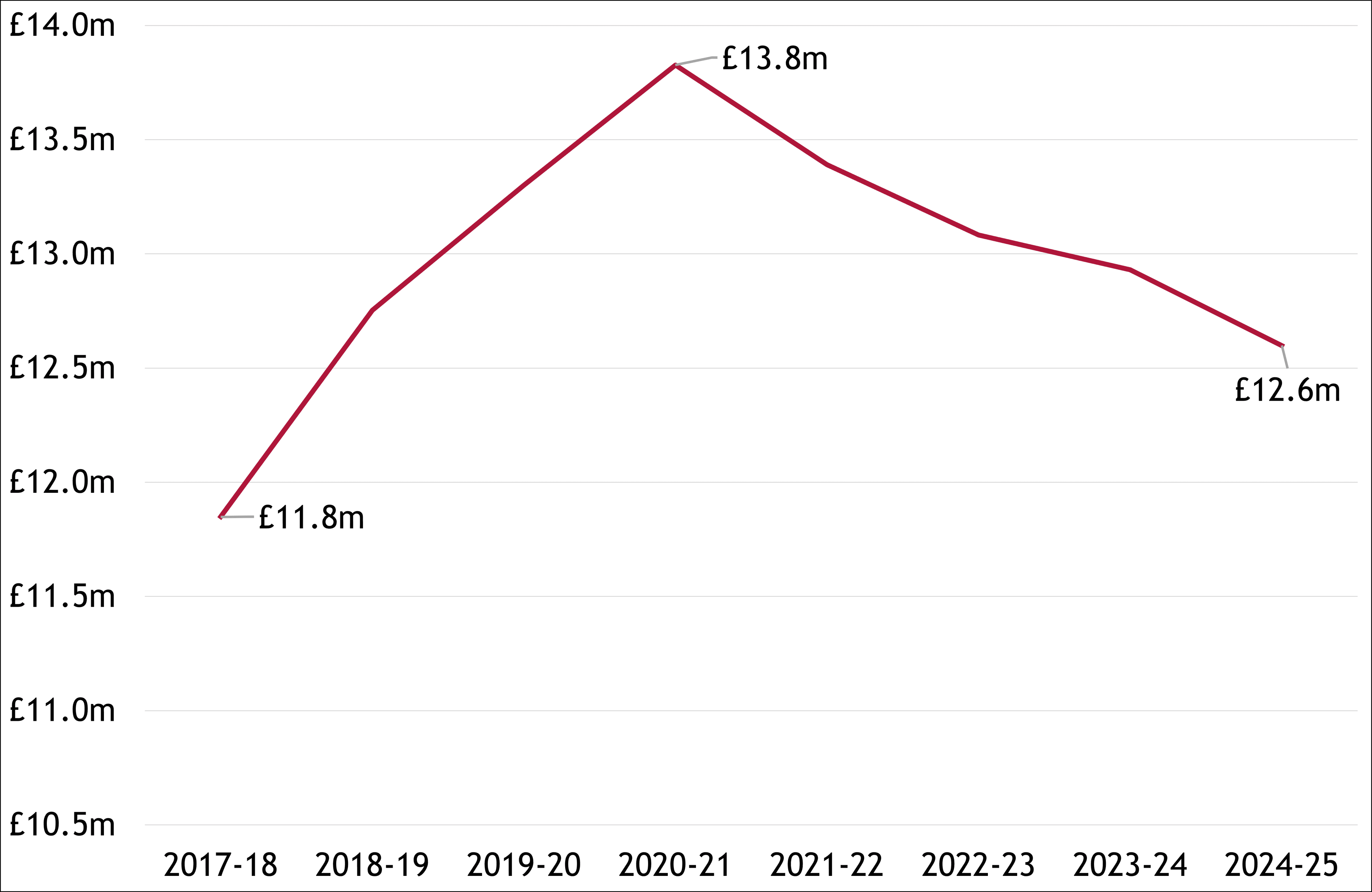

At first glance, University borrowing appears to be moving in a more sustainable direction. After increasing steadily during the late 2010s and through the pandemic, aggregate external borrowing peaked at approximately £13.8bn in 2020/21 and fell to around £12.6bn by 2024/25. Repayments have exceeded new borrowing in each of the past four years, suggesting that the sector has moved away from debt-funded expansion towards gradual deleveraging.

Yet borrowing is neither inherently positive nor negative as its value depends on whether it supports productive long-term investment. A falling debt balance can reflect stronger cash generation and disciplined repayment, but it can also result from higher interest costs, weaker credit quality, or an inability to secure finance for worthwhile projects. The data shows that although the sector is borrowing less, many institutions have less capacity to absorb recruitment shortfalls, cost increases or delays in planned savings.

The emerging picture is therefore one of deleveraging without necessarily becoming less exposed.

The end of borrowing expansion

Much of the university sector’s existing debt was accumulated during a period of low interest rates, growing student numbers and significant investment in campuses, accommodation and research facilities. In this context, long-term loans and private placements provided an appropriate and relatively inexpensive way to spread the cost of assets with long economic lives.

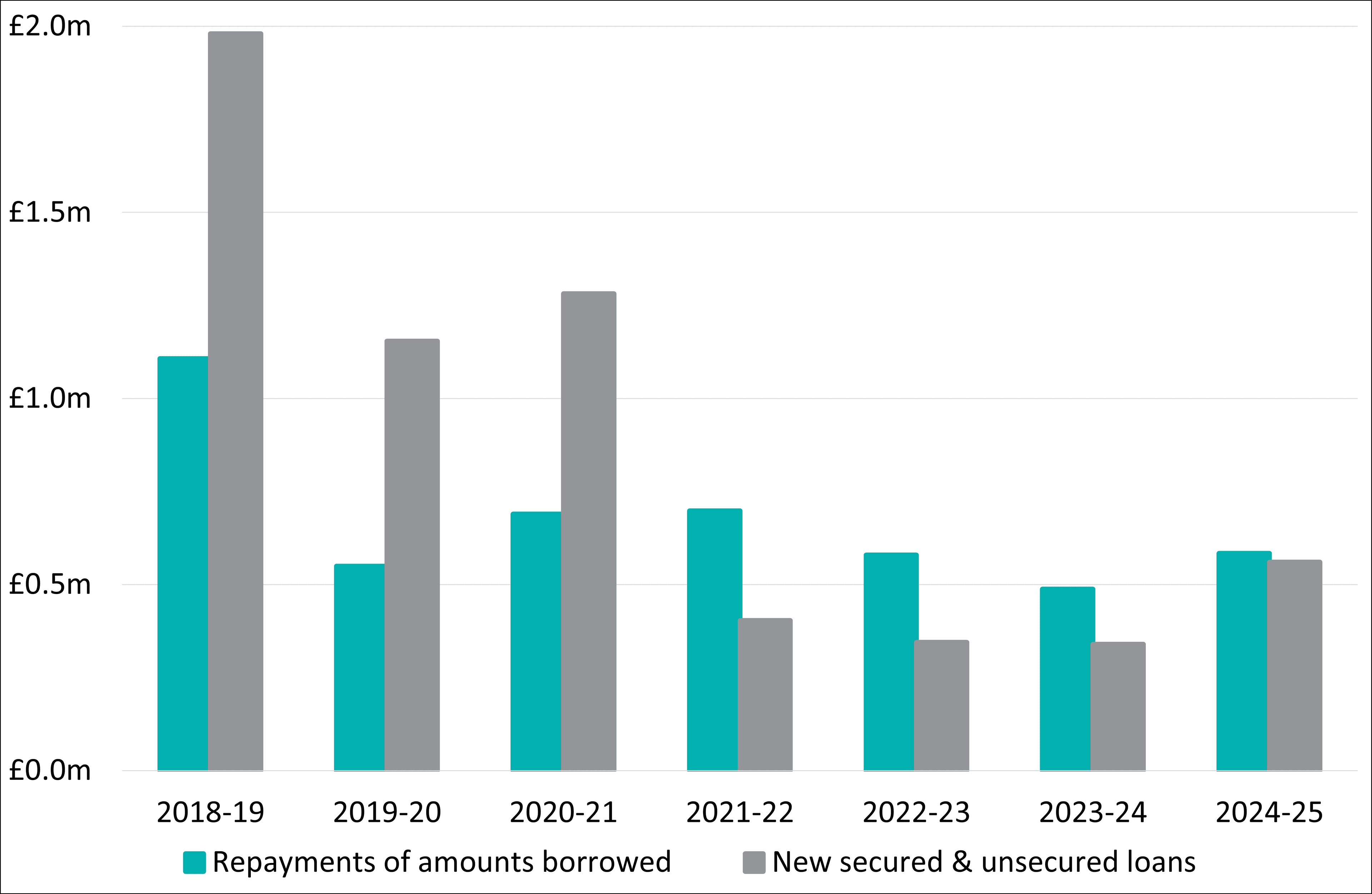

That expansion has now ended. Figure 1 shows that external borrowing has fallen by around 9% from its 2020/21 peak, while Figure 2 shows that repayments have exceeded new loans since 2021/22. That latter gap narrowed considerably in 2024/25, as Figure 3 shows, and demonstrates how, while borrowing activity has not stopped, it is no longer producing a material increase in the sector’s aggregate debt stock.

Figure 1: UK University borrowing has declined from its 2020/21 peak

Figure 2: Repayments have exceeded new borrowing since 2021/22

Rising interest rates obviously provide part of the explanation. With persistent inflation and concerns about the long-term fiscal reliability of the UK government, leading to high term premia amid broad market uncertainty, new long-term borrowing rates are significantly higher than those in the ultra-low-rate environment of the 2010s. This, combined with the weaker financial performance of universities in recent years, have made many lenders more cautious about affordability, covenant headroom and the credibility of institutional forecasts.

The Office for Students has observed a decline in longer-term commercial borrowing arrangements alongside greater interest in overdrafts and revolving credit facilities. This shift towards shorter-term borrowing is an expected response to the current steepness of the yield curve and is a trend we have observed across the sectors we advise. These facilities provide useful flexibility but are principally liquidity tools rather than substitutes for structural borrowing used to finance long-term investment. They can also expose borrowers to variable interest rates and refinancing or renewal risk.

The pressure is cash flow, not simply debt

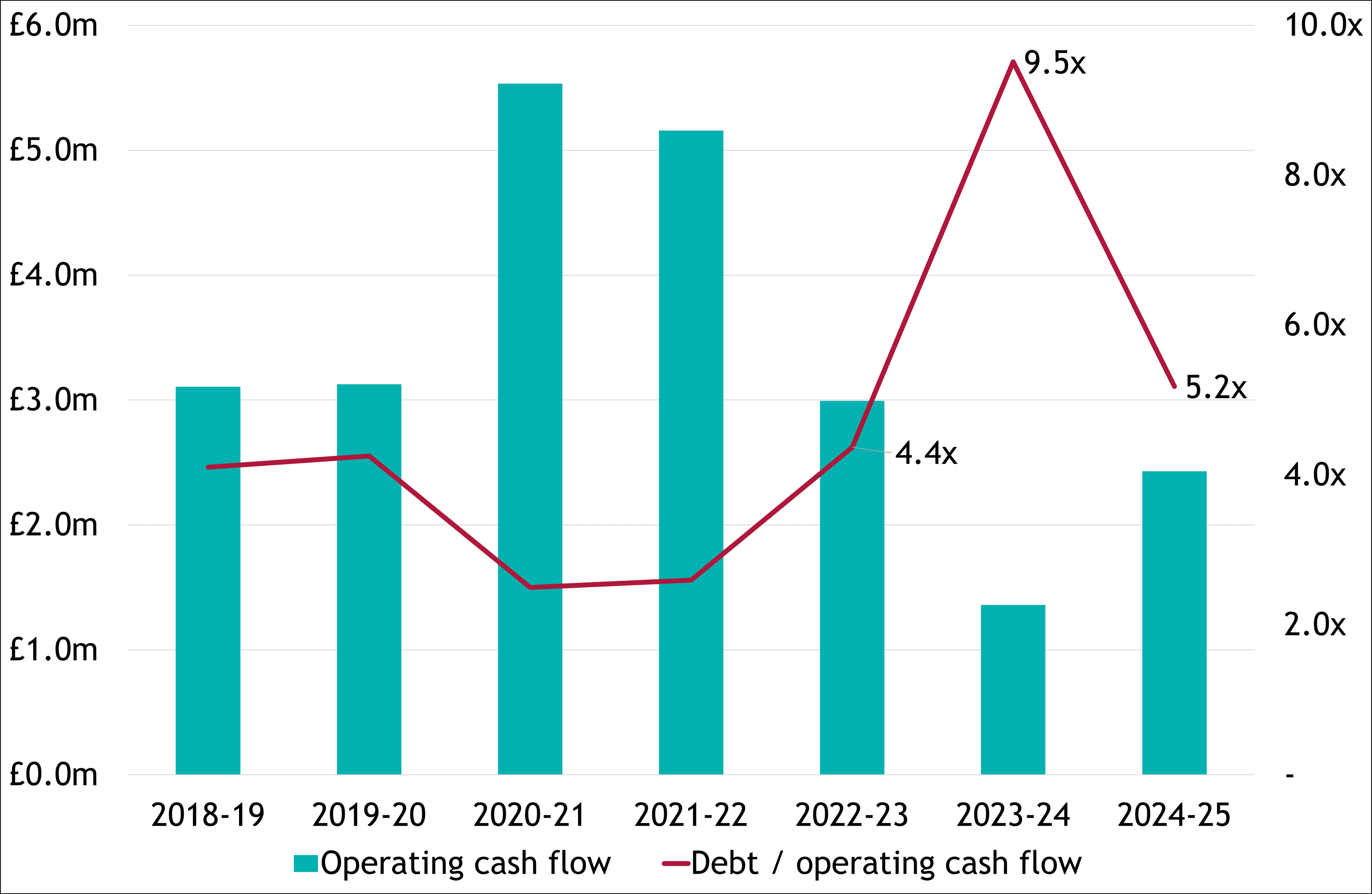

The most significant deterioration has been in operating cash generation. As Figure 3 shows, aggregate operating cash flow within the data fell from £5.5bn in 2020/21 to £1.4bn in 2023/24. It recovered to approximately £2.4bn in 2024/25 but remained below pre-pandemic levels.

This movement has had a substantial effect on debt capacity. Figure 3 also shows that external borrowing was equivalent to around 2.5x operating cash flow in 2020/21. The ratio increased to 9.5x in 2023/24 before improving to 5.2x in 2024/25. Despite the improvement, the 2024/25 level remains the second highest since 2018/19.

Notably, aggregate cash interest paid has remained relatively stable despite higher prevailing interest rates. While HESA unfortunately does not disclose the sector’s fixed and variable-rate mix, which would allow us to assess the extent of interest rate repricing, most borrowing is long-term and fixed-rate, limiting immediate repricing.

This is an important distinction, as if much of the existing debt stock is likely to be fixed rate or otherwise protected from immediate interest rate movements, the greater near-term risk is that volatile recruitment, cost pressures and delayed savings reduce covenant headroom and the capacity to service future loans. Higher rates become more significant when facilities are refinanced or amended, particularly where cash flow cover is already limited.

Our experience of lender discussions across sectors shows that banks are conscious of the practical and reputational risks associated with formal enforcement, and we have also seen lenders amending lending terms and covenants. The Financial Times has reported that banks are working with universities on turnaround plans, but this support should not be mistaken for unlimited flexibility. The Education Committee has noted that external borrowing costs exceeded 50% of income at 30 UK providers, showing how widely risk varies.

That said, the 2024/25 recovery in cash flow is encouraging, and HESA has reported that 60% of providers recorded a surplus in 2024/25, compared with 58% in the previous year. Nevertheless, the recovery should not obscure the variation between institutions.

Figure 3: Debt affordability has been driven by changes in operating cash flow

A maturity wall, or a more gradual refinance challenge?

The aggregate data does not demonstrate an immediate sector-wide maturity wall. Only around 3% of external borrowing was classified as repayable within one year in 2024/25, a proportion that has remained broadly stable.

Most university debt is therefore long-term, thereby providing valuable protection against immediate refinancing and liquidity pressure. Unfortunately, HESA data only distinguishes between borrowing due within one year and borrowing due after more than one year, meaning that we cannot know whether longer-term maturities are concentrated in 2027, 2030, or considerably later and even dispersed across institutions.

Grant Thornton has suggested that a meaningful volume of private placement refinancing may arise from 2027 as arrangements entered ten to fifteen years ago begin to mature. However, without a detailed sector maturity schedule, this should be viewed as evidence of an emerging refinancing issue rather than proof of a single maturity wall.

For individual universities, the relevant question is whether their own repayment dates, covenant tests and refinancing assumptions remain compatible with a more difficult operating environment.

The cost of protecting the balance sheet

Lower borrowing also has consequences for investment. Loans used to finance capital expenditure fell from approximately £981 million in 2018/19 to £347 million in 2024/25. Universities are increasingly funding projects without resorting to borrowing, reducing their scope or delaying them altogether.

Deferring spending or reducing scope may support liquidity and reduce costs in the short term, but sustained underinvestment can create maintenance backlogs, inefficient buildings and less attractive facilities. Using deposits and investments for operating or capital expenditure also reduces liquidity headroom and future investment income. Universities must balance the benefit of avoiding debt against the cost of using finite cash or deferring investment.

Falling bank debt may also understate wider commitments. Finance lease and service concession liabilities reached approximately £1.5 billion in 2024/25, accounting for just over 10% of broader financial commitments, while growing lending from funding councils has offset some of the reduction in commercial lending. Debt strategies should consider these obligations alongside conventional loans.

A more active approach to debt management

The sector is not facing a uniform debt crisis. Some universities have no external borrowing, while others have low debt, strong liquidity and ample covenant headroom. A smaller but important group faces high leverage, weak cash flow and limited access to additional facilities.

Universities should review their debt portfolios before refinancing or covenant pressure becomes urgent. This includes mapping maturities, reviewing prepayment provisions, assessing rate exposure, testing covenant headroom and distinguishing structural borrowing from facilities for temporary liquidity.

Arlingclose can support universities with independent debt advice, including portfolio reviews, prepayment and restructuring options, capital planning, cash flow forecasting and stress testing. We can also assess refinancing options, prepare information for lenders, negotiate covenants and facility terms, and engage with funders before decisions become time-critical.

Early planning generally provides more options and a stronger position. If you would like to discuss how Arlingclose could support your university’s debt strategy, please contact fwatson@arlingclose.com.