When borrowing money, it can be easy to stick to the tried and tested loan structure of a maturity loan. The simple structure of borrowing money on one date and repaying that loan (plus interest) is the bread and butter of borrowing and creates very little administrative burden. Although maturity loans are simple and easily accessible from the PWLB (or the Department of Finance in Northern Ireland), they are not the only loan type out there.

If we focus on the three loan types offered by the PWLB rather than other special arrangements available on the wider market, the loan types available are maturity, equal instalments of principal (EIP) and annuity. The three loan structures repay interest and principal in different proportions and at different times which creates a different ‘repayment profile’ for each loan type which can be useful in different situations.

Starting with maturity loans which are a straightforward loan type where money is borrowed, interest is paid on set dates and the full principal is repaid upon maturity. This is like an interest only mortgage where the principal is not paid down at all until the maturity date. Maturity loan structures are simple and do not require much management of cashflows as only the interest portion needs to be repaid during the life of the loan rather than any principal. However, there can be issues with refinancing due to 100% of the principal needing to be repaid at once on maturity.

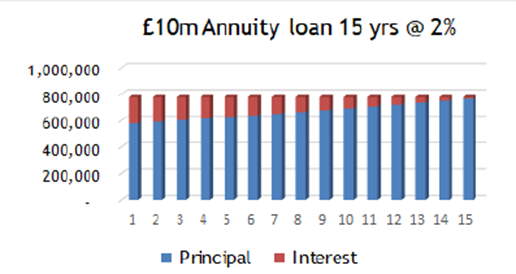

On to annuity loans, a structure that many may be familiar with from mortgage repayments, these loans involve making fixed repayments of principal and interest. This means that in each repayment period the total amount repaid would be the same but the proportion of interest and principal being repaid varies as shown in the chart below. This structure also has the benefit of providing predictable payments, making cashflow forecasting more manageable due to the fixed repayment amounts.

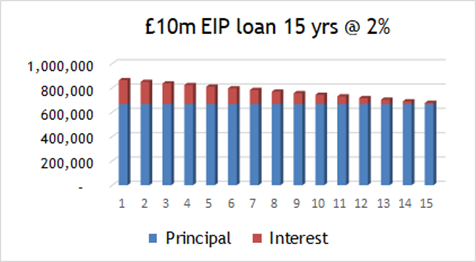

EIP loans are similar to annuity loans as the borrower pays down the principal outstanding over the life of the loan but rather than the total repayment amount being constant, only the principal repayments are fixed. This leads to a structure shown on the chart below where the principal repayments are equal, but the interest paid starts off higher and falls over the life of the loan.

Many local authorities opt for maturity loans as this structure does not require cash over the life of the loan to repay any principal and the loan is usually refinanced upon maturity. Although this is a simple system and doesn’t lead to much of an administrative burden, it does expose the authority to refinancing risk and interest rate risk. When a maturity loan comes due the authority must either have the cash available for repayment or must refinance it by borrowing the money again, this is what leads to repayment risk as interest rates may be higher at the time of repayment, but the authority would be forced to borrow to meet principal repayment.

Herein lies some of the benefit of utilising EIP and annuity loans where some of the principal is repaid each year. This automatically spreads out interest rate risk over the life of the loan as it allows the authority to refinance some of the principal each year at prevailing rates rather than concentrating all that risk in one year.

The recent interest rate environment has been a reminder that rates are not always flat and can move up or down surprisingly. Taking nothing but maturity loans can be a gamble, if a number of your maturities all fall in one of those years where rates have risen you might find your interest costs spiking unexpectedly and putting unnecessary pressure on budgets. Although the use of EIP and annuity loans won’t totally eliminate this risk, a balanced portfolio of debt can certainly help to manage it.

Related Insights