Sequencing risk, also known as the sequence of returns risk, is the concern that the timing of returns and withdrawals from an investment portfolio can have a significant negative impact on the long-term rate of return. Although this risk is often primarily associated with pensions, it is also something that charitable organisations should consider, whether the portfolio is a permanent endowment or aimed at generating regular income to fund grants.

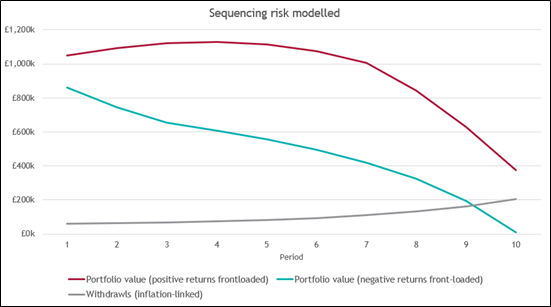

To illustrate how sequencing risk can affect a portfolio, we can compare two £1m portfolios that experience the same series of annual returns, but in reverse order. In the first portfolio, stronger returns occur in the early years and gradually decline, with negative returns appearing later. In the second portfolio, the sequence is reversed, with weaker returns occurring at the beginning and stronger returns later. Both portfolios make withdrawals starting at £20k per year, increasing in line with a long-term inflation rate of 2.3%. The return profiles for the two portfolios are shown below.

As shown in the figure, the portfolio with front-loaded negative returns experiences materially poorer performance than the portfolio with front-loaded positive returns. When negative returns occur early in the period, the capital base falls relative to the withdrawal requirements. As a result, subsequent returns are earned on a smaller amount of capital, reducing their absolute impact on the portfolio and leading to a permanent loss of value over the holding period.

Even if the investment begins to grow in the future, by limiting the capital base early on and continuing to draw down funding there may be limited scope for the investment to recover its full value which could reduce income generation down the line.

This is a difficult risk to manage as investment values will inevitably go down as well as up, and there is not always scope to delay the decision to draw funding. If grants are scheduled months or even years in advance and the timing of the distribution occurs during a market downturn, it is unlikely that the timing of the payment can be changed. Charities whose services tend to be in higher demand during economic downturn are doubly vulnerable to this as the value of investments may be falling at the same time as more funding is required to support higher demand for services.

The first and most simple step to manage sequence risk is often to maintain a reasonable liquidity buffer from which you can make payments as a backup if the value of your investment is in a downturn. This isn’t a long-term solution, of course, as cash is not a long-term investment, and there are downsides to holding excess liquid balances. However, in the short-term, this can help support payments without needing to draw down on investments.

Extending the cash management point, ensuring the maintenance of an accurate cash flow forecast, is another mitigation. Detailed cashflow forecasting can help to better understand the timing of large cash outflows and plan investment drawdowns accordingly. This can allow for the tactical withdrawal of funds early in order to secure funding for scheduled outflows or delaying further investment in order to preserve capital ahead of expenditure.

Portfolio composition and asset selection is another particularly important factor to consider early on to avoid sequencing risk. If an investment portfolio relies on total return to generate cashflows, is heavily weighted toward growth assets, or contains illiquid investments such as property or private markets investments, then additional care needs to be taken when considering the timing of withdrawals. There is often an over-emphasis on these types of investments when financial market conditions are buoyant, but investors need to be cautious where redemptions are necessary to meet outgoings. The current market downturns following the US-Israel-Iran war, occurring after strong growth in UK and global equities, are a timely example here.

Utilising investments that place more of an emphasis on income generation and reliable cashflows, such as high credit quality fixed income, investment grade bonds, multilateral development banks and supranational institution, or diversified equity income funds with an income focus, can establish a baseline of resilient income flows without the need to sell capital.

In practice, a diverse pool of a number of these asset classes is likely to be the best way to diversify risk. A range of assets with low or negative correlations can help to diversify risks during market volatility, as while the price on one portion of the portfolio may be falling, another may not be falling as much or even increasing. Having the contractual payments of income due from fixed income can help to lessen the effects of price risk even further, as these are due regardless of fluctuations in prices.

Overall, a combination of all of these strategies may be appropriate to best manage sequencing risk and preserve capital and income generating capabilities for the long-term. If you would like assistance in developing an investment policy or managing your investment portfolio, please contact jscottsoane@arlingclose.com.

13/03/2026

Related Insights

Is Impact Investing the Right Strategy for Charities?

Should Charities Lend to Local Authorities?

What are the Investment Options and Strategies Available to Charities?