Revolving Credit Facilities (RCFs) are an important element of treasury management within the higher education sector. While long-dated debt continues to fund major capital investment programmes, many universities are recognising the strategic value of committed liquidity facilities alongside their structural borrowing.

Traditionally, university borrowing has been focused on long-term funding instruments. Private placements and long-term bank loans are frequently used to finance assets such as teaching facilities, laboratories, and student accommodation. These structures are well suited to assets with long economic lives, but they are not designed to provide short-term liquidity flexibility.

RCFs serve a short-term purpose. A revolving facility provides committed funding that can be drawn, repaid and redrawn as required, allowing university treasury teams to manage temporary funding requirements without increasing structural debt levels. For universities with complex operating models and significant capital programmes, this flexibility can be particularly valuable.

Cash flows within universities are often uneven. Tuition fee income and research funding arrive in concentrated periods, while operating expenditure and capital spending occur throughout the year. A committed RCF can therefore act as a liquidity backstop, ensuring that institutions maintain sufficient financial headroom during periods of cash flow volatility or unexpected expenditure.

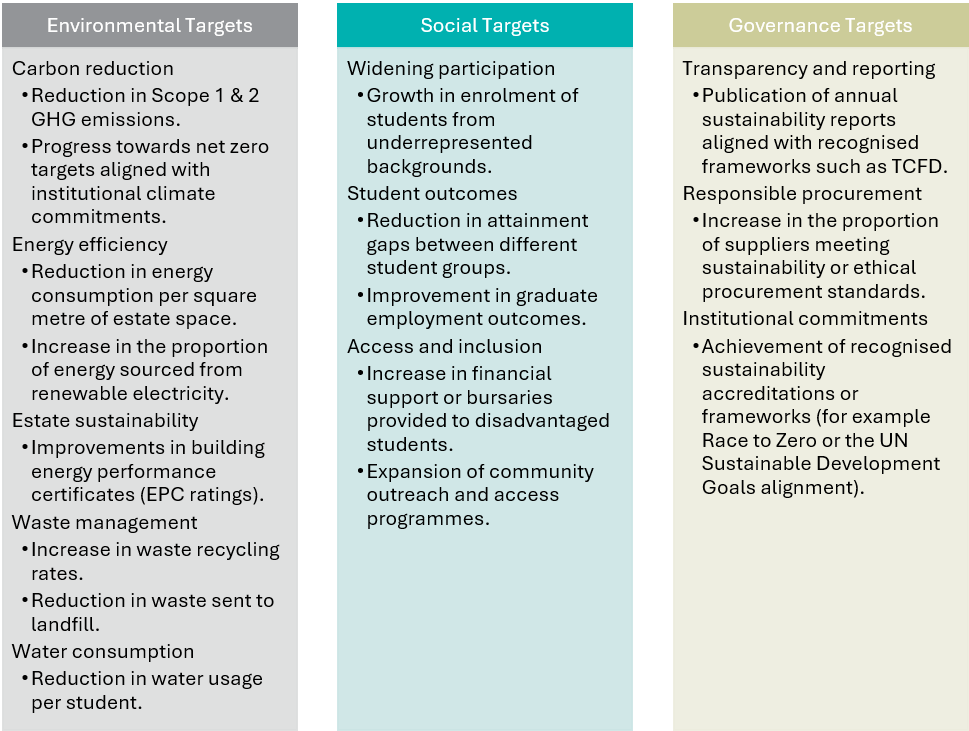

Alongside this growing use of liquidity facilities, another development is the emergence of sustainability-linked revolving credit facilities. Under these arrangements, the margin on the facility is linked to the achievement of predefined environmental or social targets. These may include metrics such as carbon reduction, energy efficiency improvements, or widening participation objectives.

For universities, sustainability-linked financing can support several strategic objectives. First, it aligns treasury activity with institutional commitments to sustainability and responsible governance. Second, it can strengthen relationships with lenders that increasingly prioritise ESG considerations in their lending strategies. Finally, where targets are achieved, institutions may benefit from a reduction in borrowing costs.

Typically, a sustainability-linked RCF will include two to five measurable KPIs, with annual testing. If the university meets or exceeds the targets, the loan margin may reduce by a small number of basis points. If targets are missed, pricing may increase slightly.

The key point is that the targets are usually institution-specific, reflecting the university’s published sustainability strategy rather than imposing a standardised set of metrics. The specific metrics will vary between institutions, but lenders typically monitor a small number of measurable KPIs aligned with the university’s published sustainability strategy.

From a university treasury perspective, sustainability-linked RCFs do not fundamentally change the role of the facility. They remain primarily a liquidity management tool. However, the inclusion of ESG-linked pricing introduces an additional dimension, allowing financial arrangements to reinforce broader institutional priorities.

As financial pressures across the higher education sector continue to evolve, maintaining sufficient liquidity headroom will remain a key treasury priority. Sustainability-linked RCFs allow universities to strengthen liquidity management while embedding institutional sustainability commitments directly within their financing arrangements.

For further information, please contact Stuart Jones at sjones@arlingclose.com.

19/03/2026

Related Insights

Should Universities Lend to Local Authorities?