Section 114 notices used to be a rare occurrence but Woking, Thurrock, Slough and Croydon have now issued these within the last two years and it is expected that there will be more to come. This has been primarily because of large debt funded investments in commercial property or companies that have not performed as expected and resulted in unmanageable deficits in these authorities. Aside from these four a number of other local authorities have received government assistance in the form of capitalisation directives, or are known to have high debt levels and a high risk of future problems.

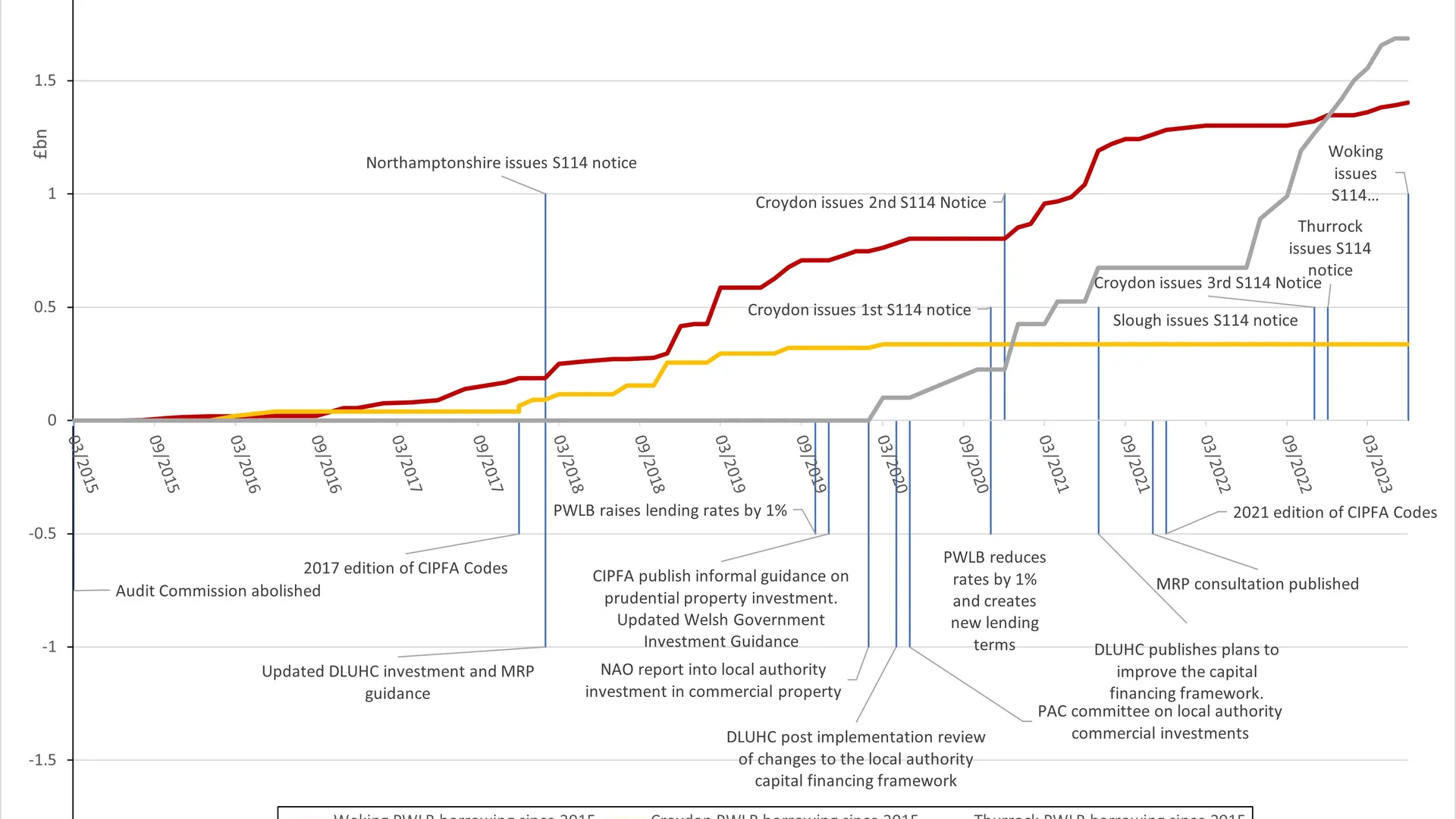

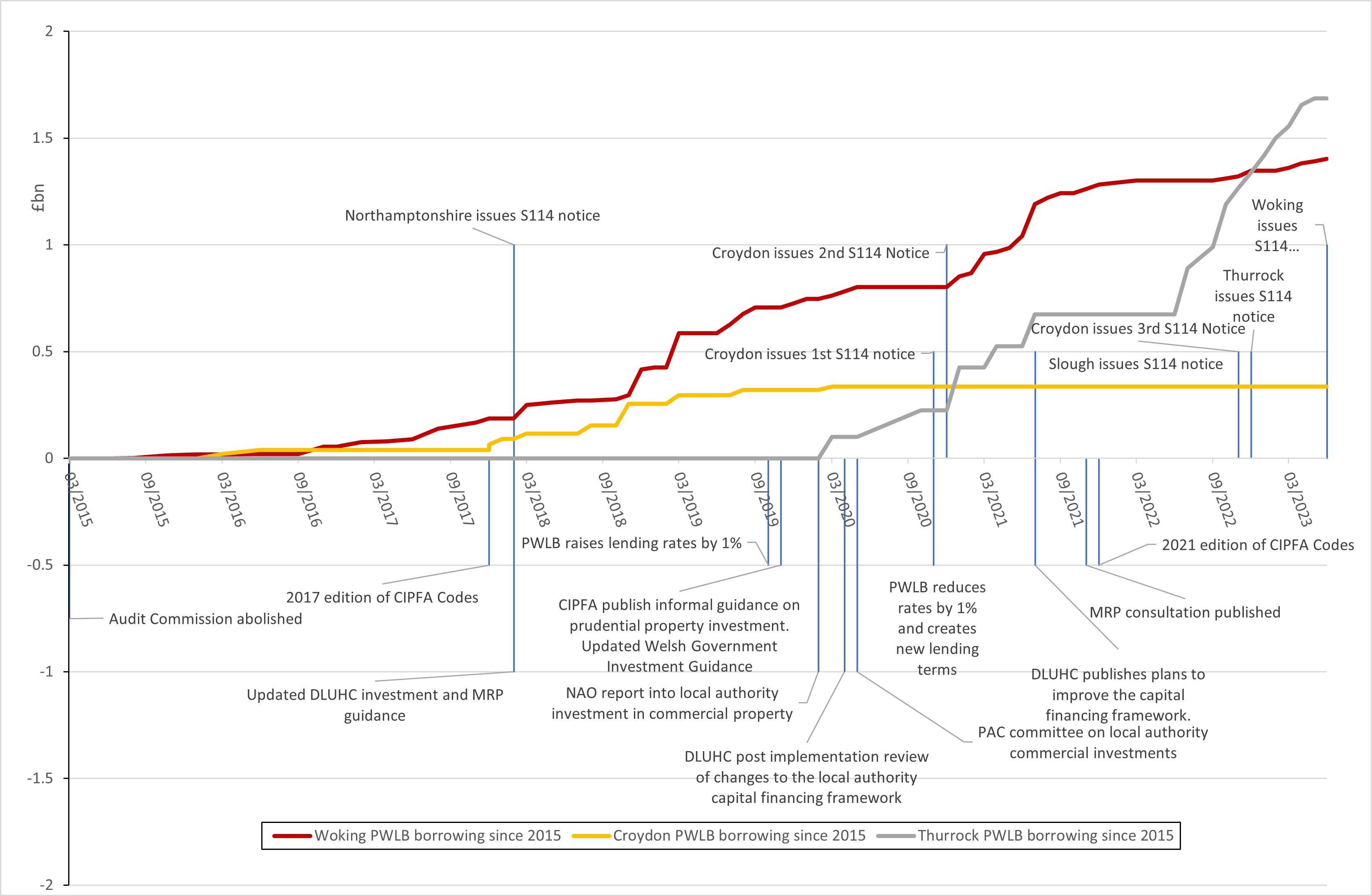

What went wrong? Clearly there are individuals responsible here and poor governance arrangements within departments and councils that have led to these failures. Many of these have been outlined in recently published reports. However, these Councils also represent a failure of regulatory bodies to stop these problems occurring in the first place, or at least stop them getting as bad as they did. Below is a timeline from March 2015 to June 2023 plotting regulatory interventions, Section 114 notices and the PWLB loans borrowed since 2015 for Croydon, Woking, and Thurrock:

This counts 11 interventions by CIPFA, DLUHC, the Welsh Government, the PWLB, the National Audit and the Public Accounts Committee. It included two new versions of CIPFA Codes, new MRP guidance, a consultation on further new MRP guidance and four other reports. How, despite all of this, did things still go so badly for a small number of authorities?

Our story begins in 2010 with the announcement that the Audit Commission was going to be abolished in England. In the new regime that started in April 2015 the auditing of local authority accounts in England was to be done by private firms and much of the other work the Audit Commission undertook was essentially stopped. In Wales, Scotland, and Northern Ireland however the former role was continued by what is now called Audit Wales, Audit Scotland and the Northern Ireland Audit Office: perhaps why the most troubled authorities are all English. Local authorities facing widespread cuts to the income they received from central government were under pressure to reduce their audit fees by as much as possible.

Austerity measures introduced from 2010 led to almost all local authorities needing to make cuts to their services and staffing levels. Faced with this some authorities sought out new forms of income to offset the loss. Relatively modest income generating schemes that also had a social or other benefit in the local area were adopted by a reasonably wide range of authorities: a small few did this on an exceptionally large scale. A small number of authorities also invested in schemes with no local benefit that were purely intended to be income generating. To fund these schemes the authorities borrowed either from the PWLB lending facility or short term from other local authorities. Low interest rates seen since the 2008 financial crisis kept borrowing costs low.

The existing CIPFA Prudential and Treasury Management Codes (those before and after the 2017 edition) had statements pertaining to the fact that security should be emphasised in investing; that any borrowing should be prudent and affordable, and that borrowing purely in order to speculate in the financial markets was not allowed.

One of the key problems was that before the 2017 revisions to the CIPFA Codes, buying say a hotel in another part of the country was regarded as a capital expenditure decision not an investment. So, this could be interpreted as borrowing to fund capital expenditure (allowed), not borrowing to purchase an investment (not allowed). Shares are in most circumstances also regarded as capital expenditure for a local authority as are loans made for capital purposes: so, investing in equity in a company or lending a company money could also be interpreted as within the rules. One prudential indicator designed to avoid unnecessary borrowing was that borrowing should not be in excess of an authority’s Capital Financing Requirement (CFR). However, any purchases of property, shares or capital loans raised the CFR at the same rate as any borrowing for them so they were not picked up by this measure.

What was ‘borrowing to invest’ was not clearly defined in the regulatory documents and was regarded as a grey area by many practitioners. The CIPFA Treasury Management Codes frequently referred to authorities not ‘borrowing in advance of need’ which rather missed the point as to what some local authorities were doing. Whilst “borrowing to invest is illegal” was a refrain heard quite frequently, the law only stated that local authorities must ‘have regard’ to the Codes of Practice on this and other subjects. Some local authorities argued that it was essential to their function to generate additional income to fund public services in the wake of central government cuts.

In response to growing concerns CIPFA revised the Treasury and Prudential Codes in December 2017. These brought investments in properties and companies into the scope of being an ‘investment’, created an additional Capital Strategy document and created further guidelines on risk management. However, the new Codes did not expressly ban borrowing to invest for financial return and the grey area around the subject remained. DLUHC published revised investment guidance and minimum revenue provision guidance in February 2018 (the Welsh Government followed suit in November 2019): similarly, these set out additional reporting requirements and brought capital purchases for the purpose of income generation into the definition of an investment.

Minimum Revenue Provision (or loans fund repayments in Scotland) becomes part of the story because local authorities are required to make a charge to revenue for capital assets purchased by borrowing. This is one of the checks and balances designed to limit capital expenditure to within affordable levels. As with the CIPFA Codes however the MRP guidance was open to interpretation with local authorities being allowed to choose their own policy on MRP – including not making any on certain assets – provided it was regarded as ‘prudent’. Some local authorities with large investment portfolios chose not to make MRP on these assets on the grounds that they were income generating and so MRP was not necessary. Changes to the MRP Guidance in 2018 tried to prevent this practice although grey areas remained and the practice continued.

CIPFA and DLUHC may have been busy publishing guidance but there was no real enforcement of them. Whilst many authorities may have looked at the new guidance and decided to change their plans, a small number clearly didn’t and nothing was practically done about this. In the past the Audit Commission would have been much more likely to check adherence to Codes of Practice - by for example looking at if borrowing really was affordable and that MRP was actually being calculated in a prudent manner. The private sector firms auditing local authority accounts in England didn’t have the resources or expertise to understand these highly specialised areas of local government finance. Lack of finance capacity within councils and external audit resources also led to many accounts being published late and audited late. Whilst regulatory bodies should still have been aware of the high debt levels and large investment portfolios of some Councils (this was widely known about by those working in the sector and PWLB lending is published monthly on their website), the lack of published financial statements for these authorities clearly didn’t help the situation.

The first step to practically curbing the high levels of borrowing by some local authorities was when the PWLB lending facility raised rates by 1% in a surprise move in October 2019. This did largely stop local authorities borrowing from the PWLB to fund these investments. However, some local authorities, notably Thurrock, had not been using the PWLB as the primary source of borrowing anyway. Other local authorities switched to borrowing from these alternative sources in the wake of higher PWLB rates. The change also came too late – many authorities had already undertaken largescale borrowing and investing by this date.

The PWLB lowered the certainty rate back to its standard 0.8% above gilts in November 2020 and alongside this published new lending terms that crucially did not allow local authorities to borrow from the PWLB to purchase investment assets primarily for yield. Borrowing to fund income generating assets whose purpose was primarily service related was still permitted. Like the rate rise a year earlier however this still allowed local authorities to use other sources to fund purely commercial investments.

Over a year later in December 2021, CIPFA finally put the nail in the coffin by stating that local authorities must not borrow to invest primarily for financial return. It also stated that any investment decision that raised the CFR and was for purposes not primarily related to the functions of the authority was not prudent. By this point Slough had issued a Section 114 notice and Croydon had issued two, Thurrock and Woking would follow and the wider fallout from the situation continues.

This is a familiar tale of regulators everywhere acting too late, too weakly and not enforcing the rules enough. I believe regulators understood what was happening, but often struggled to word regulation in an effective and clear manner. Regulatory bodies did not always consult each other effectively, leading to confusing and sometimes contradictory rules from different bodies. As anyone will tell you, whilst most people will stick to a rule because they feel they ought to some people will not unless there is enforcement (otherwise we wouldn’t need the police!). Enforcement of the regulations was lacking. There was a trust that authorities would follow the spirit as well as the letter of guidance, which again may have been the case for most authorities but clearly not all of them.

It is a predictable consequence that trying to save money by having less regulatory bodies like the Audit Commission leads to a much higher risk of something untoward happening. I am not trying to make a political statement of the rights and wrongs on the Audit Commission here: but the savings made by its abolition will have to be seen against the costs of the recent failures.

The positives that come out of this is that regulators are now looking at ways to prevent these problems in the future. The Office for Local Government has been introduced in England as a new regulatory body. There is an ongoing project to improve the auditing of local authorities and DLUHC and the PWLB have and are considering how to regulate local authorities better, including more of an emphasis on sanctions for any who break guidelines. Whilst the trade-off between more regulation and less autonomy by local authorities will need to be considered carefully I believe we can look towards a brighter future on this front.

Related Insights