The recent trend of below consensus UK inflation figures had raised hopes for a rapid loosening in monetary policy in 2024, but the ONS inflation data for December 2023 (published in January) made for less pleasant reading. The 4.0% CPI figure, while not significantly different from the prior 3.9% number nor the consensus of 3.8%, was one of many new year datapoints that dampened investors’ hopes for a rapid decline in central bank policy rates. While developments in energy markets mean that UK inflation will ease from Q2 2024, recent news flow, for example the recent surge in shipping costs due to the troubles in the Red Sea, have stoked inflationary concerns.

Annual rates sometimes take time to reflect underlying near-term trends, so it’s worth considering whether the uptick in annual inflation rates in December reflects a build-up in underlying pressures or simply a pause in the continuing downward trend. After all, the headline CPI inflation rate has now been on a downward trend for well over a year, but remains substantially above the Bank of England’s two percent target. There is also the economic picture to consider. The UK economy appears to be bouncing back from a possible shallow technical recession in H2 2023. Could an economic recovery in the UK, similar to that in H1 2023, boost inflationary pressure and make it difficult for the Bank to loosen policy?

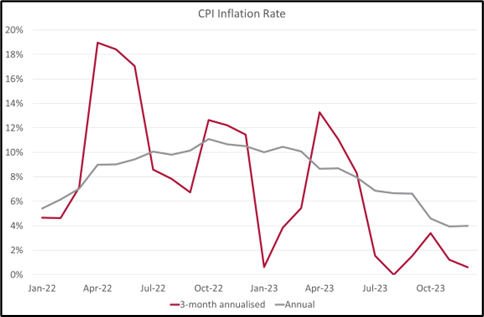

Let’s start with the CPI rate over the short run. The three-month annualised rate for UK CPI was only 0.6% in December despite a relatively chunky 0.4% month-on-month increase and the 4.0% annual increase. Given the decline in the CPI index seen in every January since 1998, this does not point to signs of building inflationary pressures over recent months, at least not yet at the consumer level. As the chart below shows, we can expect the annual rate to resume its decline in Q1, albeit after a possible rise in the annual rate in January due to weak baseline effects.

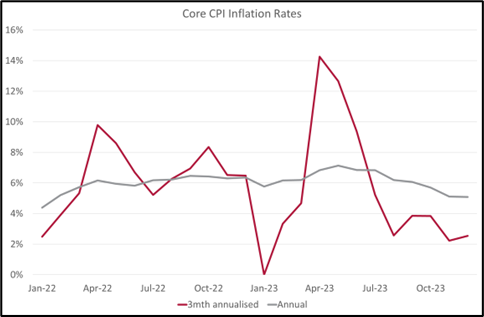

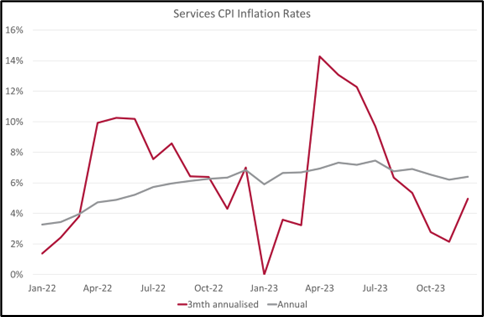

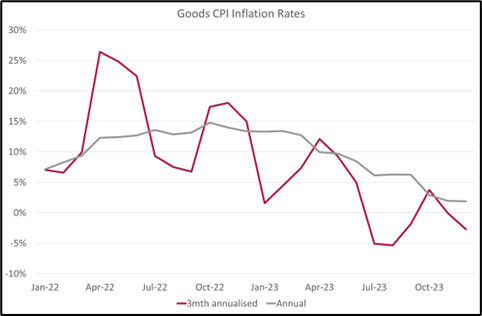

A similar story is evident in the core CPI rate. While the annual core rate remained steady in December at a still high 5.1%, the three-month annualised rate was just 2.5%. However, unlike the headline three-month annualised rate, the core rate remains above target, indicating that much of the recent downward pressure stems from food and energy. Perhaps more concerning is the Services CPI rate, the annual rate for which has been the stickiest of the component groupings. The annual Services CPI rate edged up to 6.4%, while the three-month annualised rate in December was a hefty 5%. Goods inflation is currently having an offsetting effect, but will need to ease further in order to bring overall CPI down; fortunately, this is a likely occurrence, at least in the first half of 2024.

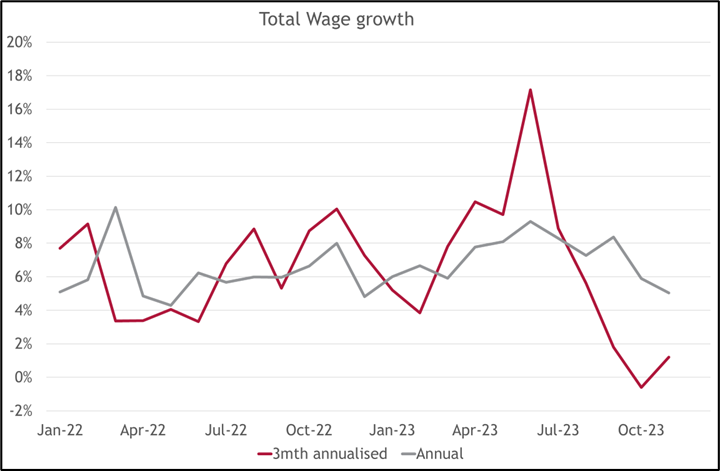

The key influence on services inflation is wages. Official wage growth measures have remained stubbornly high, although other survey measures suggest that it is easing relatively quickly. As the chart below suggests, the single month year-on-year growth rate for total pay in November was 5.1%, but the three-month annualised growth rate was just 1.2%. A more marked decline in annual rates is therefore on the way, although will take longer to show up in the headline three-month year-on-year measure used by the ONS for wage growth.

The more recent short run trends suggest that disinflationary influences in some components will continue to place downward pressure on the headline measure, so we should not get too hung up on slight reversals in data such as that seen in December. The annual headline CPI rate could rise in January, but is subsequently likely to ease rapidly due to both strong base effects and further declines in retail energy and food prices. The analysis also highlights areas of more embedded inflation, such as in the services sector. Policymakers will be hoping that a lower headline measure will bear down on household inflation expectations and ultimately wage growth over time.

We therefore see the rise in the CPI rate in December being a pause in, rather than an end to, the recent downward trend in UK inflation rates. Judging from financial market rate expectations, investors tend to agree, with the recent market volatility reflecting changing views about the timing and extent of monetary loosening. The market is currently pricing around a 60% chance of a Bank Rate cut at the May MPC meeting, but is this likely?

In terms of the direction of the CPI rate, there is a distinct possibility it could be at or below target for April, although that data will not be published until after the May meeting. However, policymakers have made it clear that the services and core rates are better measures of inflation persistence, and both will likely continue to exceed both the headline measure and target over the coming months. The wary mindset of policymakers, scarred by the sharp rise in and stickiness of inflation, suggests there will need to be strong evidence of these measures coming to heel before any monetary loosening, and recent history indicates that Committee members have a predilection to basing decisions on observed data rather than the Bank’s own projections (in which they now seem to have less trust). Finally, although Bank Rate has peaked, monetary policy tightening continues via quantitative tightening. Ending this programme will surely need to be a precursor to cutting rates.

So, despite the very likely decline in the headline CPI rate measure and the probable fall below target later in the year, the more cautious on the Committee will wait until there are clear signs of more moderate growth in the stickier underlying measures before cutting rates. The second half of 2024 looks a better bet.

Related Insights

Capital Flexibilities - A Call for Views