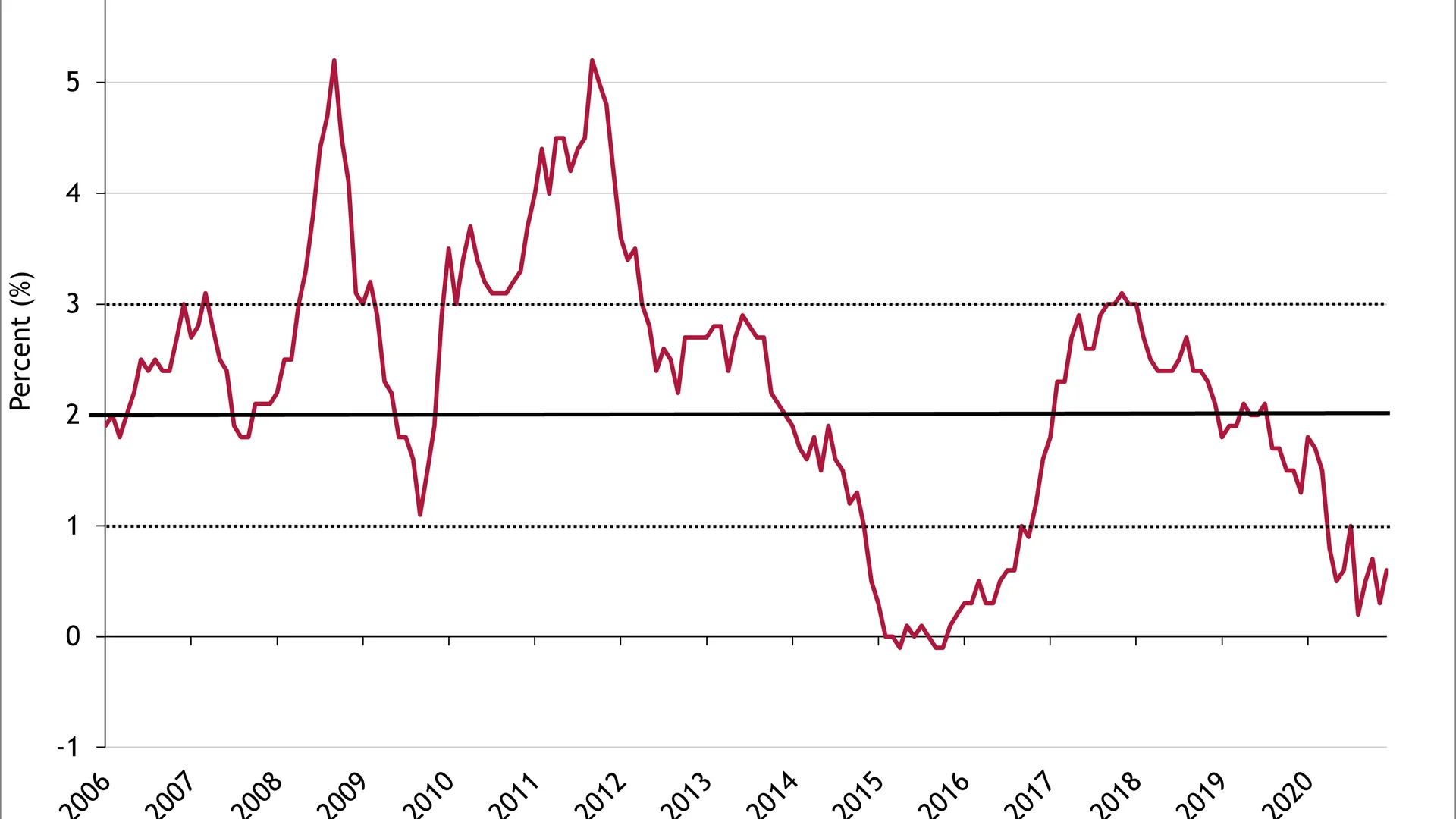

Global inflation expectations have risen since the turn of the year, driven by a culmination of factors, on both the demand and supply sides. These expectations encouraged a move into more risky asset classes, particularly in the first week of the year, where the FTSE 100 rocketed up by 3% or more. On the other hand, global government bonds have had a more challenging start to the year, with inflation expectations pushing yields upwards, particularly in the US. In fact, US 10-year breakeven levels have exceeded pre-coronavirus levels, suggesting that investors believe US inflation will rise to levels not seen during healthier economic times. So, do we have to be concerned about a sustained pick up in inflation and therefore interest rates?

Inflation is certainly going to rise this year. In the UK, inflation weakened during the first lockdown and has been relatively low since, primarily due to both a VAT cut for hospitality and reductions in energy and petrol prices. Looking forward, unless the government extends the VAT cut, hospitality prices will automatically rise from 31 March 2021. Meanwhile, oil and other commodity prices are up significantly since the pandemic lows, while Brexit appears to be prompting a rise in costs on both sides of the Channel. Shipping prices in general have risen over the past few months due to heavy demand, as consumers have moved from service to goods spending due to lockdowns.

The VAT rise will feed directly through into the headline CPI inflation rate, while the rise in oil prices will likely affect petrol prices. The other factors will boost consumer inflation to varying degrees, which will depend partly on the strength of demand.

It is the strength of demand which is so important for a sustained pick-up in inflation. One-off or temporary supply or price shocks do happen, but generally act as a detriment to growth rather than happening due to growth. Central banks certainly won’t be reaching for the interest rate hike button in these events.

Just looking at the impact of coronavirus itself, once government support programmes conclude there is likely to be a substantial number of unemployed or perhaps underemployed, which will weigh on household demand. Some businesses may fail when removed from life support, while the bailiffs will be back to collecting debts.

Much is made of latent demand, due to those workers who have been able to shift easily from workplace to home, saving on travel and other work-related costs. The wall of savings built up by this cohort is presumed to transform into an avalanche of spending following coronavirus. There may well be an element of this as we reacquaint ourselves with holidays, theatres, cinemas and restaurants, but many may be content with simply having a higher level of savings and it is unlikely that an excessive amount of savings will be spent – in fact, there is an argument to suggest that households will continue to be cautious; after all, the next coronavirus, or simply the next mutation, could be just around the corner.

It also overlooks the fact that the working from home experience has not been uniformly beneficial in terms of savings. For some, working from home has been costly, especially if income has been lower or non-existent – for this element, savings have been eaten into rather than built up.

This is not to say that there will not be an economic recovery in the UK at some point in the near future, but rather that the recovery will not drive a sustained pick-up in demand-led inflation, at least not enough to persistently breach the Bank of England’s target.

Much is also made of the monetary and fiscal stimulus in terms of inflationary pressure. One of the main drivers of the rise in US yields is the expected fiscal stimulus unleashed by the Biden-Democrat government, which is projected to directly boost household demand. Cheques to households rather than central banks buying financial assets is certainly more likely to lift spending, which could feed into higher demand-led price inflation. However, these programmes have acted to cushion the drop in private sector demand – they are not adding to already strong private sector demand, although admittedly, timing is a key factor here.

I suspect the pick-up in core inflation across developed economies will be contained and not the start of sustained multi-year push against and above inflation targets. Economic spare capacity will be considerable and changes in ways of working/continued caution will prompt disruption in certain industries, prolonging the move back to full employment. Central banks are unlikely to tighten policy anytime soon. A sustained inflation-led rise in yields, particularly UK yields, looks unlikely.

-960x640.webp&w=3840&q=75)