HM Treasury’s consultation on the Public Works Loan Board (PWLB) “Future Lending Terms” closes at the end of July. While we wait to find out about new rules, rates and availability, an expanding band of borrowers are asking themselves - is it time to do something different on debt?

We all know and love the PWLB; a great range of products, easy access (for the moment at least), with cash available within two days. But the PWLB has become increasingly unpredictable. While local authority finance officers hope the promised reduction in PWLB margin and rates will be substantial, maybe 0.80% or more, when will it be delivered? September 2020? March 2021? Will they disappoint on rates? Uncertainty makes planning and budgeting difficult, another set of variables to consider in an increasingly uncertain world.

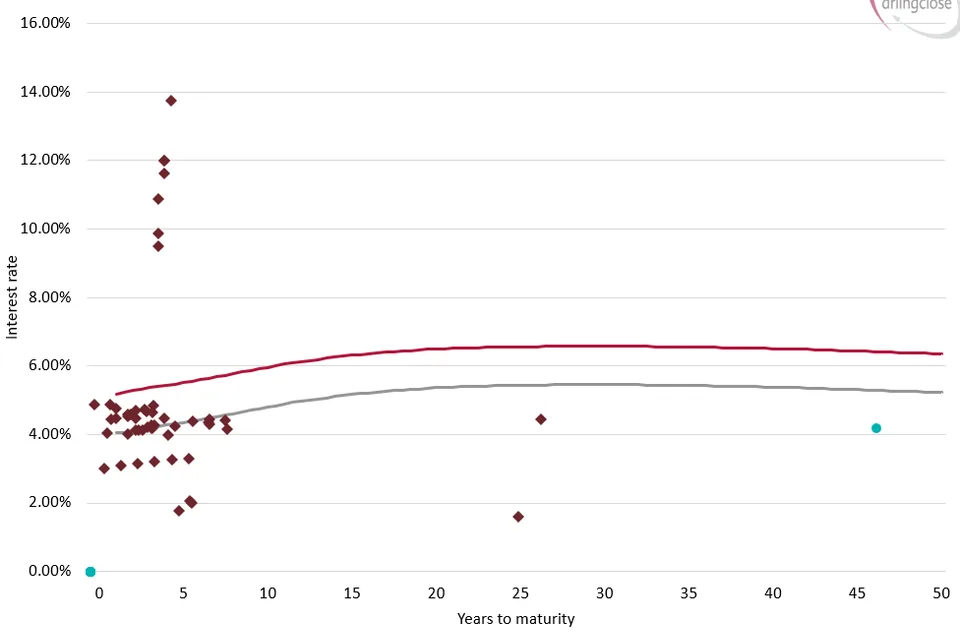

A growing number of local authorities have decided to go their own way. Record low underlying interest rates look attractive, with negative gilt yields out to seven years and a twenty-year yield resting just above 0.50%. Unsurprisingly perhaps, some borrowers want to capture funding at these levels.

However, the past few months have not provided the best conditions in which to raise funding from the private sector. A sovereign rating downgrade, with the potential for further reductions, combined with financial strain across local authorities, means investors are cautious. Some, like many local authorities, have chosen to sit on liquidity during the lock down, deferring long term investment decisions, while the banks have been at capacity delivering government schemes to preserve customer’s liquidity. Most of this activity has been undertaken by staff adapting to working remotely, impacting on their investment capacity and resources.

Conditions are beginning to improve; investors want high quality assets with additional yield. During this period of uncertainty some investors have focussed on Registered Providers, where credit quality is familiar, and returns have jumped higher; there is no PWLB backstop in this market. However, we expect appetite for local authority investment to improve as markets settle. Unfortunately, in the private placement market at least, most will continue to benchmark their pricing against prevailing PWLB rates; we are back to waiting for HM Treasury for the best rates here.

But there are opportunities, the alternative alternatives, with progressive authorities using this time to expand their knowledge base and contacts testing out different funding strategies. West Berkshire Council has launched a Community Municipal Investment, a small issue at £1m, but at around 0.40% below prevailing PWLB certainly a step in the right direction in diversifying funding streams at a reasonable rate. The Municipal Bond Agency (MBA) also continues to refine its offering, it will be interesting to see the results of their planned group bond issues.

The “local to local” market is evolving too, many LA investors grabbed a bargain when rates briefly spiked above 2.0% in March, although a glut of government funding has seen those rates plummet to below 0.1% for shorter dates. Yield can be found in longer durations, but these transactions should be supported by terms that provide flexibility, increased due diligence and documentation.

There are also new debt management solutions that allow authorities to capture current low underlying interest rates while avoiding the higher credit margins that prevail. These solutions provide significant savings; most welcome at a time when local authority budgets are squeezed.

Debt management is evolving, and authorities do not need to wait for HM treasury to take the next step. An increasing number are throwing off the chains and committing time to understanding new ideas, some of which will deliver a substantial boost to the budget and deliver funding at record lows.