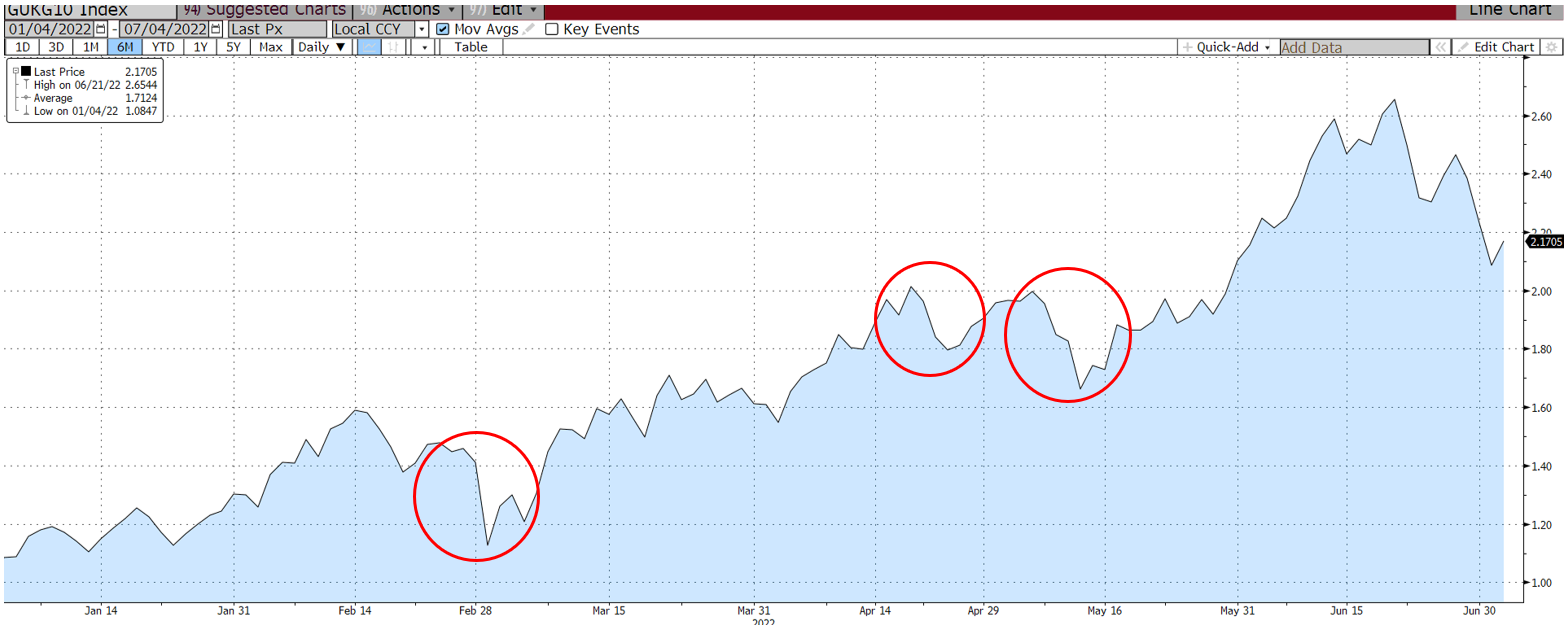

Over the past two weeks, financial markets seemed to finally realise that the global economy is facing difficult times ahead, amid a narrow focus on inflation from central banks that has caused a huge rise in bond yields. This realisation has led to a rather dramatic repricing of assets and interest rate expectations, prompting a very sharp fall in bond yields; the 10-year gilt yield declined from the high close of 2.65% on 21st June to 2.09% on 1st July, while intraday dropped further to 2.03%. For those of us that have been waiting for this penny to drop as market movements looked increasingly erratic and divorced from reality, it was about time.

The decline followed a rather noticeable shift in economic data over the past few months and more recently signs that price pressures in the US may have peaked. It has been clear for some time that global economic growth would struggle amid a synchronised tightening of financial conditions by central banks. Now the mood music appears to have changed, from positivity about central bank intervention on inflation to fears that they will go too far, damaging growth and inflation later on.

However, this is not the first time that yields have fallen sharply, and we also need to put the fall into context. At the close on 30th May, the 10-year gilt yield was 1.99% - the yield would rise 66 basis points over the next three weeks. We have not therefore completely retraced our steps.

Steep reductions in gilt yields have occurred over the past three months but are now small blips in a seemingly unstoppable upward march. In mid- April, the 10yr yield dropped 20 basis points to 1.80%, and around the start of May, another 35 basis point drop over a few days to 1.66%. As noted above, by 30th May yields had recovered the lost ground and were just about to embark on a sustained climb to 2.65%. Going back further, the start of the Russian invasion saw another tumble as investors turned to safe havens. Every time, investor focus, returned to inflation and policy expectations, driving yields higher.

Chart: 10 year gilt yield (source: Bloomberg)

Is the recent plunge going to follow the same path? After all, policymakers have not stopped discussing large rises in policy rates, inflation remains high and labour markets remain tight. Previously, however, hawkish policymaker rhetoric and policy moves were supported by the upward march of inflation data – the combination of the two convincing investors that policy rates would rise further, quickly and significantly. Investors also appeared to believe that US interest rates could rise sharply without a significant economic impact.

Now signs that US inflation appears to be peaking amid slowing growth has shifted investors’ attention to the impact of tighter policy, and the prognosis on growth is much less optimistic. US policymakers now admit that tighter policy will cause economic pain and job losses, while US consumer confidence has plummeted, consumer spending has eased, and growth forecasts have been slashed. Interest rate cuts are being priced in for later years.

However, substantial investor uncertainty about the future will only see a continuation of outsized movements on the back of minimal data, which make it difficult to argue that the decline in gilt yields is the start of a sustained shift to a level based on lower policy expectations. Given the outlook for inflation (still moving higher in the UK for instance) and the targeting of headline measures by policymakers, it is difficult to see the upward pressure on yields ending, particularly if data suggests that inflation is becoming embedded. We can also expect continued hawkish rhetoric by central bankers to show they remain strong on controlling inflation. Even if inflation did ease, there is a possibility that this is interpreted as being more positive for sustained growth, presumably supporting interest rate expectations, albeit with fewer or less aggressive hikes than markets currently price in.

Ultimately, while we’d like to think that the penny has dropped, investor perceptions change quickly, and we should not yet assume that this decline in yields represents a fundamental shift in the recent upward trend. But it is only a matter of time until this shift does occur as global growth continues to deteriorate.

Related Insights

Interest Rate Uncertainty and the MPC’s New Member