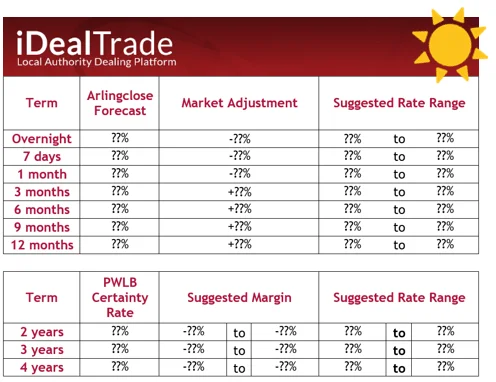

At iDealTrade we release weekly rate guidance which reflects where we believe the market is, and where we think our users will find a match. To calculate our rates, we take our Arlingclose in-house interest rate forecast and add an adjustment to recognise demand and supply factors. As the LA-LA lending market grows there is greater availability of data that we can use to learn how this market moves, allowing us to tailor our adjustment accordingly, with the aim of producing more accurate rate guidance.

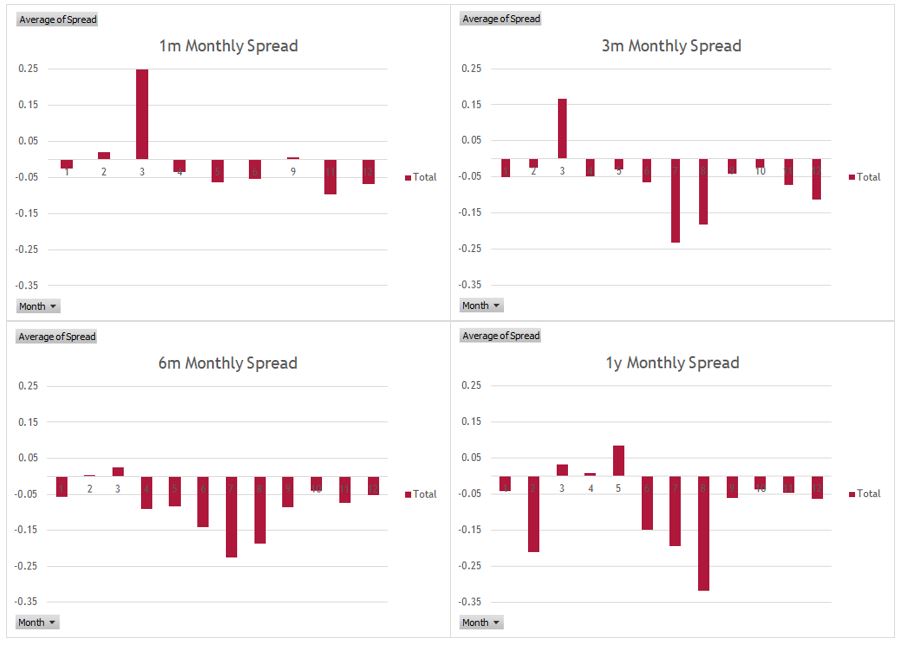

From a sample of local to local trades made in recent years, both through iDealTrade and elsewhere, we have identified a broadly consistent seasonal pattern in the average spread between LA-LA rates and the London Inter-Bank Overnight Rate (LIBOR). This is shown below across four short-term loan durations: 1 month, 3 months, 6 months and 1 year.

For most of the year, we found that rates are below LIBOR, with slightly greater seasonal volatility for 1-year loans. Rates usually fall to a substantially lower spread during late summer. In March, rates are always above LIBOR, and considerably so in the shortest durations.

March is therefore not a great time to borrow, though we understand trades at this time of year are most commonly made out of necessity relating to year end cash flow. However, what it does show is that March is a profitable time for investors that are able to part with the cash. July and August are better for borrowers, particularly for the longer durations, with rates then moving more favourably for investors in the Autumn.

In addition to the current indicators, awareness of this seasonal relationship allows us to tailor our market adjustment to the time of year and generate rate guidance which follows the LA-LA market specifically, with informed differences between durations. We have incorporated the findings of this analysis into our guidance, and will continue to monitor the data as it becomes available.