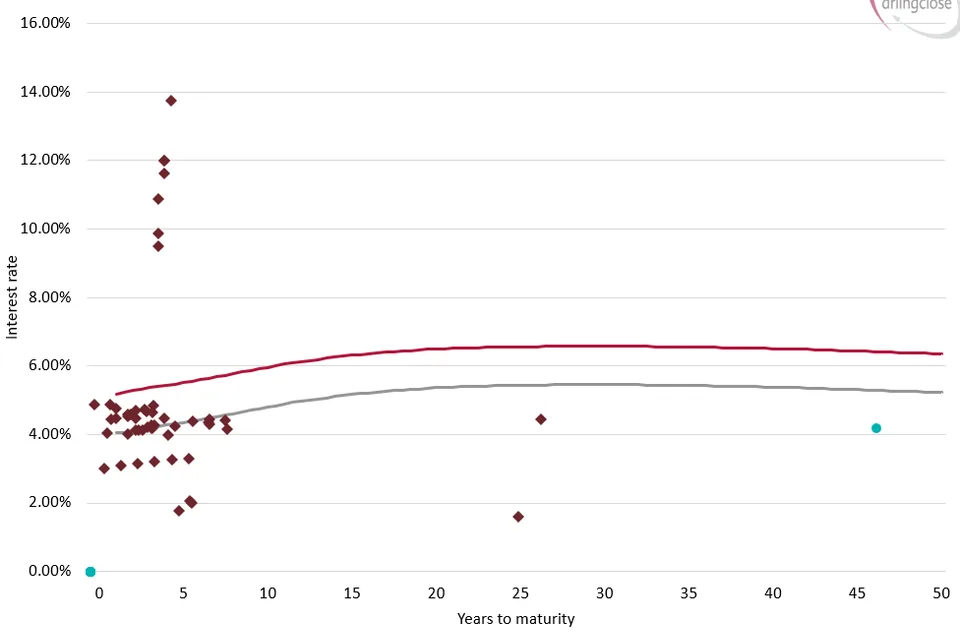

During this period of historically low interest rates there is an opportunity for local authorities with borrowing requirements to fund at levels never seen before and probably never to be seen again. But how long will rates remain this low and if your interest budget is becoming reliant on the current cost of short-term debt what can you do to protect yourself against rising rates?

Local authority debt portfolios are constructed through a mix of long-term fixed rate loans from the PWLB/Banks, short-term variable rate loans from other locals and the use of balances and reserves through internal borrowing. As pointed out above with funding costs this low it would seem counter intuitive to borrow long-term when short-term rates are at rock bottom but what about the risk of rising rates? The traditional way that this has been managed is to take fixed term debt, even when it is priced at nearly 2% above the Government’s own cost of borrowing.

Managing a debt portfolio is one side of an organisation’s Treasury Management function and the definition of Treasury Management in the CIPFA Treasury Management Code (TM Code) is: “The management of the organisation’s investments and cash flows, its banking, money market and capital market transactions; the effective control of the risks associated with those activities; and the pursuit of optimum performance consistent with those risks”. Managing borrowing decisions therefore exposes an organisation to risks and these should be managed within the context of the TM Code.

We are all fully aware of the risks associated with invested funds and take great care in ensuring that the mantra of Security, Liquidity and Yield is followed, but how detailed is the analysis over the risks associated with debt portfolios? Or is the focus only concerned with the average rate on the amount borrowed and therefore the interest paid? If this is the case, then the attraction of borrowing at low rates in the current environment might be too good an opportunity to miss, but are you exposing yourself to the risk of rising rates in doing so and if so how do you envisage managing that risk?

Many commercial organisations manage large debt portfolios, and like local authorities, must choose between borrowing fixed or at a floating (variable) rate. There is risk in deciding the balance between floating rate and fixed rate debt. Too much fixed-rate debt creates an exposure to falling long-term interest rates and too much floating-rate debt creates an exposure to a rise in short-term interest rates. As we are at record lows should you therefore not take advantage of the fixed rates on offer and lock out all your risk? Not when the margin being charged by your principal lender is so high would be our advice.

In addition, corporates face the risk that interest rates will most probably change between the point when the need to borrow is identified and the actual date when the money is spent. This is no different to the local authority treasury manager who may wish to borrow in advance of spend but cannot afford the cost of carry. To manage the risks around interest rates many commercial treasury managers will use derivatives to manage their risks. Common derivatives used include futures contracts, forwards, options, and swaps.

The TM Code, makes specific reference to the use of derivatives: TMP1 Interest rate risk management suggests that a local authority should “manage its exposure to fluctuations in interest rates with a view to containing its interest costs” and mentions derivatives in TMP1 [3] “It will ensure that any hedging tools such as derivatives are only used for the management of risk and the prudent management of financial affairs and that the policy for the use of derivatives is clearly detailed in the annual strategy.”

So, if corporates use them and the TM Code which covers local authority treasury activity makes reference to the use of these instruments why are local authority treasury managers not looking into this area to firstly take advantage of the current low level of interest rates and secondly manage the risk of rates increasing in the future?

We feel that this a result of past actions, the use of derivatives by local authorities is still clouded by the Hammersmith and Fulham case from way back in 1992. Using derivatives to reduce risk (hedging) should be considered by any sensible treasury manager, whilst using them to increase risk (with the hope of increasing returns) is speculation and should be avoided.

Nearly 30 years have passed since the speculative use of derivatives was deemed to be ultra vires. Perhaps it is now time to look at all the opportunities available to manage all the risks in your treasury operations?

If you think you are exposed to undue interest rate risk, then here at Arlingclose we are well placed to suggest and implement suitable hedging strategies. Please contact us if you wish to discuss further.