New PWLB Policy – a decent result

PWLB “certainty rates” have tumbled to all-time lows following the implementation of HM Treasury’s long-anticipated consultation response. This is a great result for the majority of local authorities that will qualify. Combined with both a relatively light touch application procedure and preservation of the ability to refinance internal borrowing and existing loans, regardless of whether the authority is purchasing an investment asset primarily for investment yield (PIAPFY), the outcome is better than may had feared.

Immediate access to these lower rates is granted, with borrowers simply having to confirm compliance with the rules and expenditure plans submitted via this year’s “certainty rate” form. Authorities can continue their budget setting process with more certainty and in most cases significantly lower assumptions regarding new borrowing costs. Those that have purchased assets before 25th November 2020 announcement will be in the clear, the rules are not retrospective.

To maintain continued access to the PWLB next financial year, local authorities will need to confirm they are complying with the new PWLB guidance and detail spending across each of the following areas:

- Service delivery

- Housing

- Regeneration

- Preventative action

- Treasury management

Any Surprises?

Permitted uses of PWLB loans include the newly announced “treasury management” category, covering the refinancing of internal borrowing and external loans, regardless of activity on PIAPFY. This preserves a key plank of local authority’s liquidity management and therefore credit worthiness. “Preventative action” is another new category, covering urgent expenditure to prevent negative outcomes, where no obvious alternative is available. An example may be the purchase of property in a council’s town centre to stop urban decay, but note that HM treasury do not expect this to happen on a large scale.

What activity is not supported via PWLB loans?

PIAPFY has a relatively narrow definition in the guidance covering buying land or existing buildings:

- To let out at market rate;

- That continue to be operated on a commercial basis without any additional

investment or modification;

- Other than housing, which generate income and are held indefinitely.

How easy is it to demonstrate compliance with the rules?

Much depends on the nature of the project. The decision rests with the section151 or equivalent; HMT has stressed they expect the process to be relatively painless, although they do expect a robust process to be applied to categorising spending and ensuring compliance. The problem will be the grey areas, the projects that combine purchasing assets and generating yield in some form. It is also safe to assume that activities that break the spirit of the guidance, including gaming the system by deliberately conducting PWLB borrowing and PIAPFY in different financial years, may bring enquiries and sanctions. Penalties for misusing the PWLB could include a request that the local authority unwinds problematic transactions, suspension of access to PWLB or, ultimately, repayment of loans with penalties.

Lessons from a year in the wilderness

So, what have we learnt from a year when PWLB become uncompetitive? Clearly the dangers of “policy risk” have been highlighted, but the effects were muted via a vibrant “local to local” market that plugged the gap and the evolution in commercial lending. The period has seen the first interest rate swap transaction by a local authority in 30 years and the municipal bond agency (MBA) finally find its raison d'etre and issued bonds. Hats off to the MBA, Lancashire and others that provided the blueprint and benchmarks that surely prompted HMT to move faster and further than may have otherwise been the case.

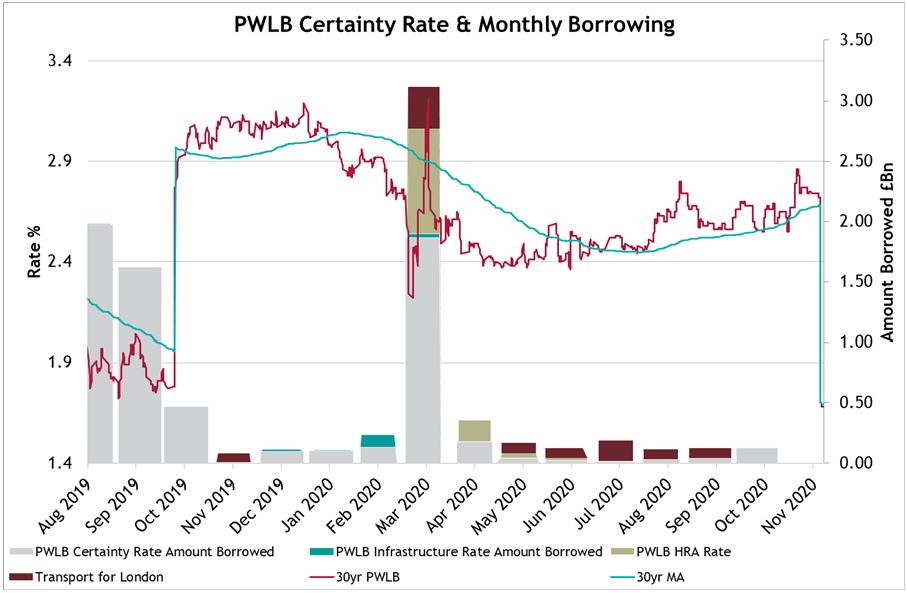

The chart below shows PWLB monthly borrowing over this period and it tells an obvious tale. The PWLB facility has proved important for local authorities, not least during the early part of the COVID 19 pandemic in March 2020, when liquidity seized up in the LA to LA market.

But it also shows how markets adapt and evolve, with banks and institutional investors filling the void left by uncompetitive PWLB rates. These organisations have learned about the local authority credit quality, and as the hunt for yield continues, I expect they will be back for more once they recalibrate yield expectations.

A more diverse future?

What about the future? I hope this evolution continues, with an emphasis on a strategic, balanced approach to funding.

Local authorities that would not perhaps have chosen to fund short from other authorities have got used to the idea, funding at levels that remain 0.70% below the new PWLB rates. The bond agency should be supported, you never know when you may need them again. Ideas such as green bonds and derivatives, common in most other sectors, should be explored. The PWLB’s new terms should be embraced but not misused, or indeed, overused.

Collectively, these strategies have the potential to bring increased flexibility, diversity, risk reduction and savings to local authority treasury management.