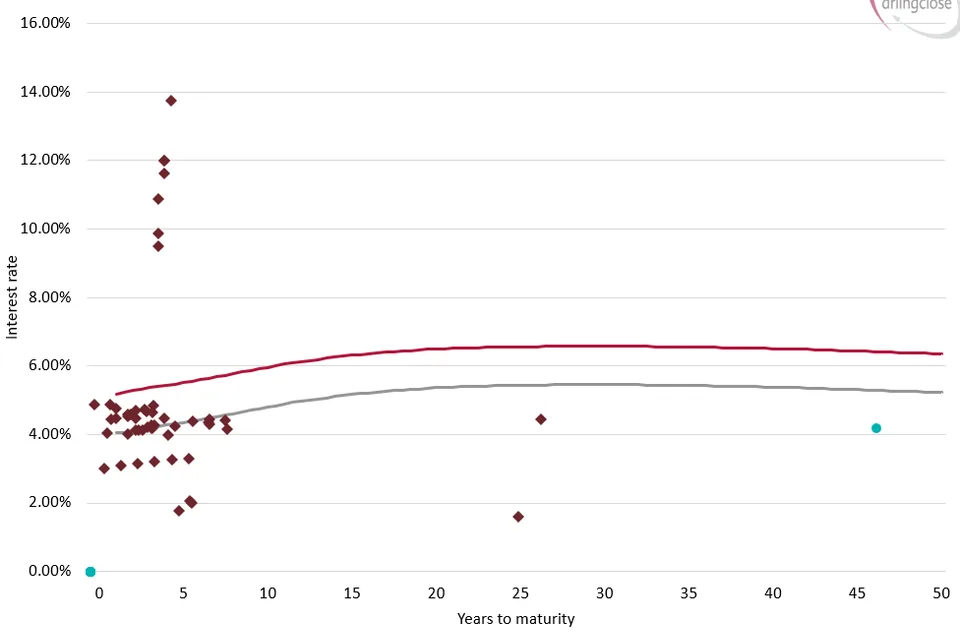

Higher interest rates are not always bad news, bringing with them new investment, debt prepayment and refinancing strategies. Discount rates on some loans are now nudging over 3% (at the time of writing), presenting the opportunity to prepay or refinance debt to generate savings and reduce risk.

The rampant increase in inflation and interest rates has created a conundrum for many treasury managers wrestling with uncertain multi-year funding programmes and a relatively limited range of tools with which to manage rate risk. However, consider authorities with strategic investment balances; latest DLUHC statistics reveal local authorities collectively held investments of £59bn at the end of March 2022, with the majority of this in short-term cash products. Many of these authorities also have outstanding debt, but a combination of very low interest rates and HM Treasury’s penal redemption terms have stifled prepayment of late.

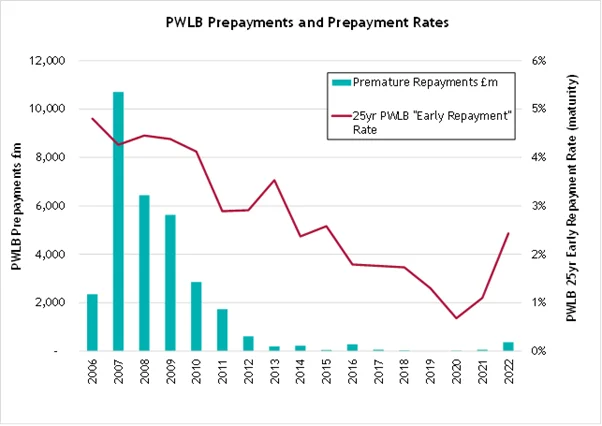

The chart below shows the correlation between interest rates and the level of PWLB prepayments, although this doesn’t tell the whole story, with the spread between PWLB new and early repayment rates, relative investment returns and the global financial crisis all playing a part.

Note: 2012 figures excluded PWLB prepaid as part of housing subsidy reform.

The chart shows how authorities became reluctant to repay debt early as rates plunged below 3%. The additional 1% margin added to new PWLB loans in October 2010 provided another barrier, killing most “PWLB to PWLB” refinancing stone dead. Those refinancing PWLB loans after this date would incur a discount rate below gilt yields and the additional margin HMT include in new loan rates, which has ranged from 60 to 180 basis points over recent years.

Alternative forms of refinancing have prevailed though. Arlingclose has advised on over £1bn of Lenders Option Borrowers’ Option prepayments in recent years, with the latest transactions undertaken by Braintree DC, Liverpool CC and Suffolk CC. Why did these and others work? Because some commercial lenders are keen to offload these assets, allowing negotiated prepayment at discount rates in excess of the PWLB certainty rate. Authorities can refinance LOBOs with PWLB debt, reducing interest cost and removing the unwanted refinancing risk associated with LOBOs, a risk that increases with rising rates.

As rates increase it’s not just LOBO refinancing that may appeal, the prepayments of debt without replacement has come back on the agenda. Authorities with surplus cash balances have eschewed prepayment while interest rates have remained at ultra-low levels. With PWLB discount rates below gilt yields, simply buying a gilt to match the maturity of unwanted debt would be a more economical proposition, at least in theory. Investing surplus cash in alternative asset classes via pooled funds has also proved to be a successful strategy over the past decade, achieving annual returns of up to 4% or more. As current discount rates exceed 3%, straight repayment may be back on the agenda, delivering a “risk free” saving on interest payments, assuming that debt is not required later.

Of course, that’s a big assumption and is where detailed analysis, liability benchmarking and an assessment of the treasury position will be important. Scenario and sensitivity analysis should be undertaken, along with an assessment of required accounting treatment included. The results may conclude there are now some interesting saving opportunities on debt management, something that will be most welcome for local authorities wrestling with current budgetary pressures.

Related Insights

Arlingclose advises on LOBO refinancing for Braintree District Council

LOBOs: The Secrets of Successful Refinancing