The growth of passive investing shows no signs of stopping. In 2017 alone, growth in Exchange Traded Funds took global Assets Under Management (AUM) to $4,569 billion according to consultancy firm ETFGI.

Often framed as an argument of one versus the other, but the active or passive decision isn’t a binary one and long-term passive investing should not be completely passive. In much the same way as investors should evaluate and review an actively managed fund on an ongoing basis, there are similar considerations for passive investments - Does it fit with your latest investment objectives and constraints? What’s your desired asset allocation? Is it generating the income or return you need? All strategic investments should be evaluated over a relevant time horizon, regardless of whether you would prefer to pay an active manager to (hopefully) deliver above-market returns after fees or, for instance, you believe the long-term annual growth rate of the FTSE 100 fits with your investment needs and are happy to pay a modest fee to achieve this using a passive index fund.

However, as mentioned at the start of the previous paragraph, investors don’t have to choose between the two but can mix and match, with one approach being what is called core-satellite investing. If you believe that some markets, such as the FTSE 100, are more informally efficient (i.e. new information is quickly incorporated into share prices) and active managers may, on average, struggle to beat the market consistently*, rather pay a manager a higher fee in the hope they can outperform, they should consider investing passively in a cheap index tracker (the core) and earning the return on the market. For markets, sectors or investment strategies where active managers may be able to add value due to their skill and/or a lack of wider coverage in the investment community, such as small cap stocks or emerging markets, then a portion of the portfolio is more aggressively invested in these active funds (the satellite). A core-satellite asset allocation may then consist of 50% in a passive fund with the remaining 50% split between a number of active funds. The ‘core’ helps to keep volatility and costs down while the satellite active funds are employed to outperform their benchmarks and generate alpha for the portfolio.

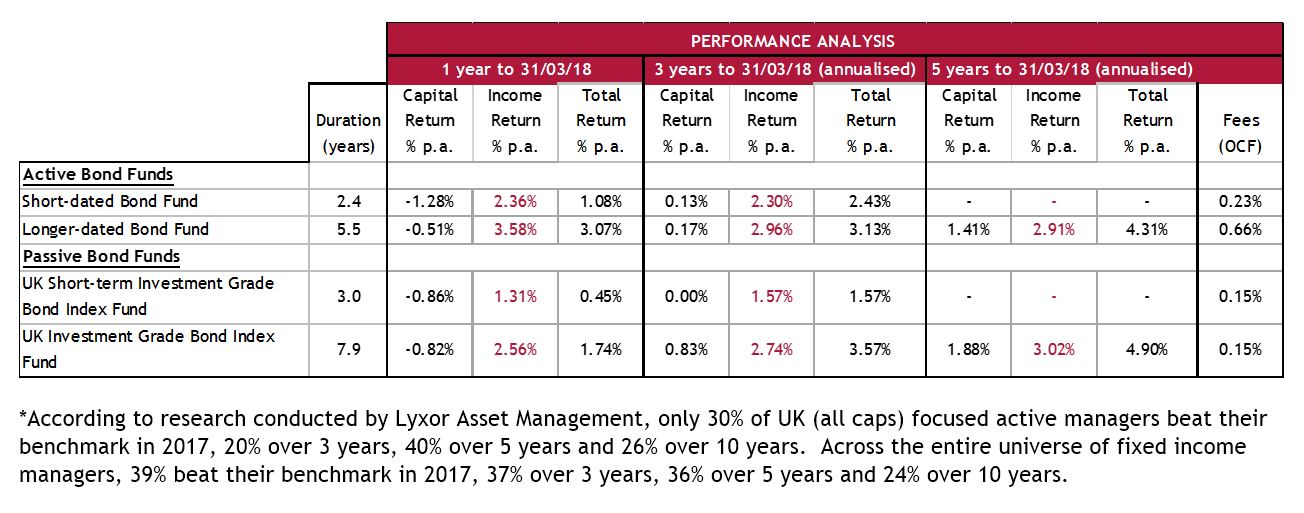

By far from being an exhaustive piece of research, but the table below presents the performance of four well-known funds, two active and two passive, with capital, income and total returns shown on an annualised basis over 1,3 and 5 years (where available). The funds have been chosen for their similar strategies and to allow fair comparisons in terms of duration (i.e. price sensitivity to changes in interest rates).

Looking initially at the two shorter-duration funds and active outperforms over 1 and 3 years. A 1-year income and total return of 2.36% and 1.08% for the active fund comfortably beats the 1.31% and 0.45% achieved by the passive fund. After deducting fees of 0.23% and 0.15% for active and passive respectively, this gives a total return outperformance of 55bp. Over 3 years, our recommended minimum time horizon for a bond fund, the level of active outperformance increases to 78bp. So, active 1 passive 0.

Turning now to the longer-duration funds and the passive more than matches the active performance over the longer time horizon. Granted, over a single year the active fund is ahead, however over 3 years the active fund generated 2.96% income return and 3.13% total return while the passive earned 2.74% and 3.57%. Over 5 years the figures are 2.91% and 4.31% for the active and 3.02% and 4.90% for the passive. Good news for the passive on that basis alone, but now factor in that 0.66% in fees need to be deducted for the active fund but only 0.15% for the passive and the 3-year total returns become 2.47% versus 3.42% and 3.65% versus 4.75% for 5 years, which means around 100 basis points of better performance each year over the period.

This brief analysis highlights how complicated the investment decision can be and is by no means a suggestion that clients move their underperforming active funds into passive investments, but only ever considering the active path, paying higher fees in the hope of higher performance, may not always be the best way forward for long-term portfolio returns.

-960x640.webp&w=3840&q=75)