Investment benchmarking is an exercise that our clients will be very familiar with. We invite our clients to partake in this every quarter with the results published after two weeks of submission.

Which investments are benchmarked? The investments in question are solely investments made for treasury purposes, not investments made for services purpose.

Why partake in this? For starters, this report is an excellent way to view what has been going on in our LA client base for the previous 3 months. New trends that emerge can be spotted and documented not just for the quarter but also when comparing multiple benchmarks. Another reason is that the report gives a clear and concise breakdown as to many facets of your respective investment portfolio. One can look at anything from your average credit score to liquidity levels or to duration to name just a few options.

LA’s come in all shapes and sizes, from a small parish council to a much larger county council. Our investment benchmarking offers the opportunity to compare your results to all other authorities as well as your authority’s respective grouping, for example comparing all district councils. This information may not necessarily influence investment decisions, but it is certainly a useful tool to gain an insight into the LA market.

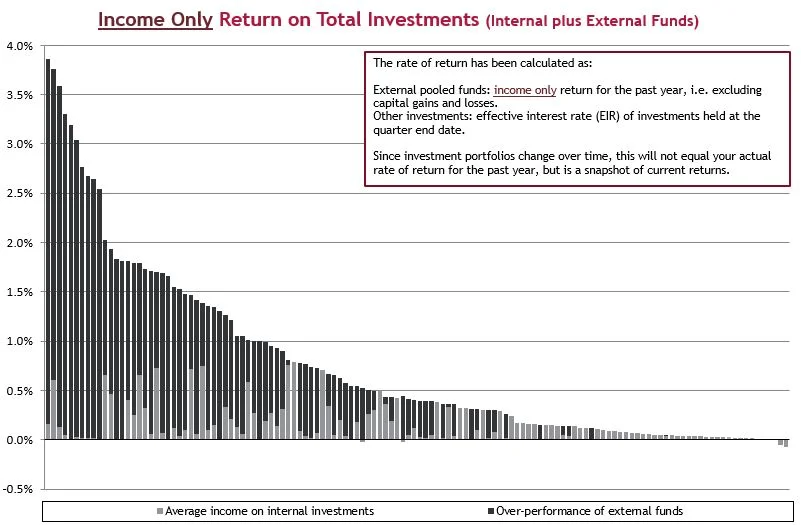

One clear change within the LA market that has occurred over the last year has been the changes within local authorities’ internal investments i.e. excluding externally managed funds. Many local authorities have moved to more liquid investments which include call accounts, Money Market Funds (MMFs) and short-term deposits with the Debt Management Office (DMO). No prizes for guessing but this is due to the COVID-19 pandemic. Local authorities needed access to cash and their investments more so than before and this was reflected in many investment portfolios that were solely in either MMFs or call accounts. For many authorities, this need for instant liquidity was also supplemented by deposits with other local authorities, which is excellent to see. These particular deposits are exempt from bail in.

Some authorities still have concentrated counterparty exposure (often via a solitary call account) and it is important to remember that diversification is very important, especially with the backdrop of the crisis we are facing. MMFs offer the benefit of greater diversification over a single name and investing with multiple MMFs over one takes this one step further.

Another constant theme that has been prevalent for many years is that those authorities that are in externally managed funds can access higher levels of return. Of course, these increased returns come with an increased level of risk (there is no such thing as a free lunch!). These funds also add an element of diversification so there are multiple benefits to going into these funds if the level of risk taken on is appropriate for the investment portfolio. The current pandemic has affected capital values, but these are longer term investments that should be held for many years. On top of this, they remain important sources of income and therefore this capital loss does not have to be realised in this instance.

For enquiries on local authority treasury investments or if you would like to discuss your respective investment benchmarking report, please contact the Arlingclose team on treasury@arlingclose.com.