Since the financial crisis of 2007-08 many sizable economies have seen low growth, investment and inflation. Central Banks (CBs) have therefore increasingly needed to use more unconventional and perhaps forceful forms of monetary policy, an example being the implementation of negative interest rates (NIR). When a cut in interest rates to zero is insufficient to combat deflationary forces in the economy, it may be necessary for CBs to set a negative main policy rate in order to boost output.

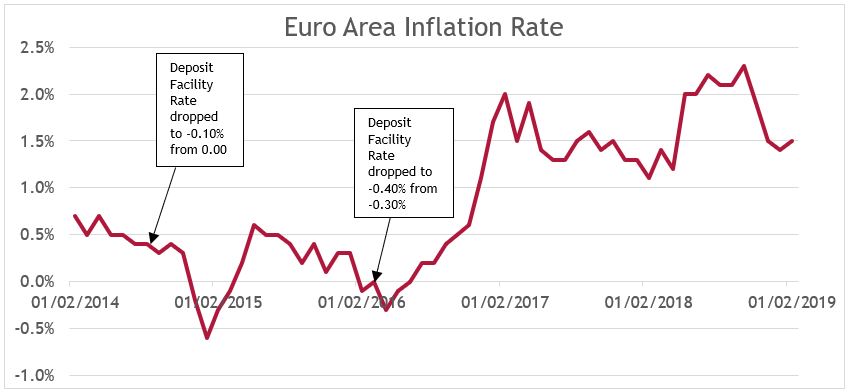

In Europe, low inflation sparked fears that the Euro Area could fall into a deflationary spiral. The main task of the European Central Bank (ECB) is to maintain price stability which they define as a Harmonised Index of Consumer Prices “below, but close to, 2% over the medium term”. The ECB first introduced a negative deposit facility rate of -0.10% in June 2014 as they attempted to counter low inflation – following in the footsteps of the Danish National Bank. By charging banks to hold reserves at the ECB, they encourage these banks to lend more which they believe will boost consumption, investment and drive up wages.

In March 2016 the ECB launched triple stimuli (as growth and inflation remained low) by cutting the rate further to -0.4% (from -0.3%), stepping up QE to €80bn a month while trying to offset risks of negative rates by offering unlimited four-year loans at almost negligible cost to banks. The graph above confirms how the inflation rate has increased since the March 2016 announcement. We don’t know whether NIR policy has had a positive effect, as it is difficult to work out the counterfactual from the increase in Quantitative Easing (QE). QE and NIR policy used together have indeed achieved positive inflation results.

However, there are still theoretical dangers and concerns associated to such unconventional monetary policy. NIR policies stimulate risk-taking as bond yields and interest on deposits decrease; it is conceivable that investors seek better opportunities to invest with the aim of achieving higher returns. If they turn to depreciating assets or real estate, they may generate bubbles which could potentially ‘burst’. Also, Money Market Funds have the potential to be destabilised under the introduction of negative interest rates. Insurance and Pension Fund business models may catastrophically fail due to legacy challenges as heightened concern over long-term saving and investment institutions could encourage even greater saving. Furthermore, there is debate over whether financial market infrastructures can cope with rates turning negative. The ECB states that this issue did not arise, due to intensive technical cooperation between the ECB and market participants, before they introduced a negative main deposit facility rate in 2014.

David Blanchflower, who formerly sat on the MPC, recently labelled Mark Carney “stupid” for stating that interest rates could potentially rise in a disorderly no-deal Brexit. Instead, he is of the view that the BoE may be forced to introduce NIRs to support economic growth. However, a no-deal Brexit would, more than likely, lead to a sharp decline in the value of sterling and as the UK is a net importer this would lead to higher inflation. NIR policy will exacerbate rising inflation above the BoE 2% target. Simply put, it will be very difficult for the BoE to support economic growth and keep inflation under control using monetary policy alone.

Mark Carney has publicly voiced his opposition to NIR policy on many occasions and therefore the BoE setting negative rates soon seems an unlikely proposition. However, as the Governor of the BoE is supposedly stepping down in January 2020, who knows what the future holds. The ECB stating earlier this year that their rates will not move until mid-2020 ensures that NIR policy is a discussion which will not fade anytime soon. This seems to be a marmite-topic; dividing economists almost down the middle. Some will tell you NIRs have been successful in stimulating Denmark, Sweden and Switzerland, but others will point out that Japan experienced no growth and was left with its bond market in tatters.

If the BoE were to implement NIRP, it is important that 1) rates don’t fall too low causing a severe effect on bank profitability and 2) there is a contingency plan to revert rates back above zero. The latter has been a real struggle for the ECB, where a range of countries have Government bonds with negative yields even at long maturities – indicating that the market doesn’t anticipate rates reversing soon. There is certainly an “economic lower bound” to interest rates, whereby it becomes favourable to hold cash. Reaching this point will have detrimental effects on the banking sector, something which the BoE must avoid.