Do local authority “financial investments” represent a big problem for the sector? During the recent Arlingclose and Room151 webcast on the draft CIPFA codes there was a lively debate on the scale of the issue and the risk entailed.

But what do the figures tell us about this? Let’s explore stats and recent trends in this area.

Punt

The draft Prudential Code states authorities “must not borrow to invest primarily for financial return”. Much has been written about local authority commercial investment, with House of Commons public accounts committee (PAC) identifying 179 authorities that purchased commercial property in the three years to 2018–19.

But what about financial investments? How many authorities are borrowing to invest in externally managed funds?

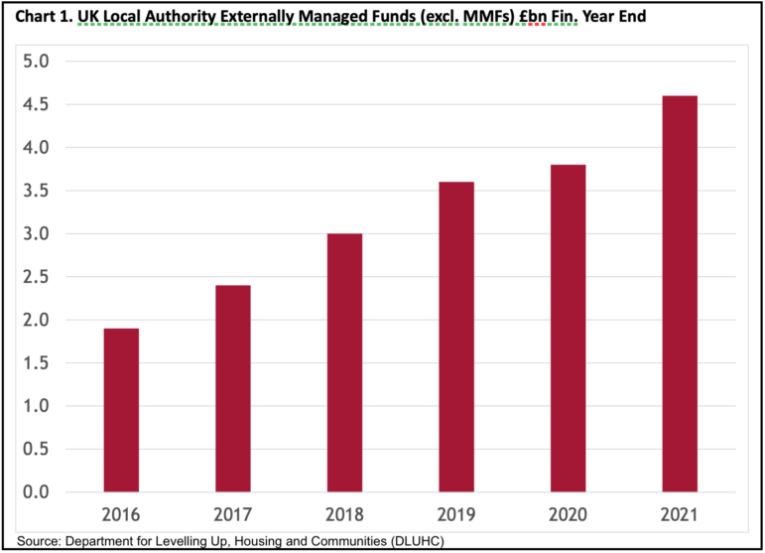

The newly named Department for Levelling UP, Housing and Communities (DLUHC) provides quarterly statistics on local authority borrowing and investments, providing useful insight. According to their figures, the aggregate sum invested in externally managed funds—defined as funds placed with a fund manager, excluding money market funds— was £5.1bn across 89 authorities at the end of June 2021.

The chart below shows steady growth over the past 6 years, as local authorities seek greater diversification of asset classes, counterparties and duration in the face of rock bottom cash deposit rates.

Is this a debt fueled punt into increasingly risky assets or the sensible management of strategic cash? Well, when viewed alongside the borrowing data for individual authorities it becomes clear the majority of authorities do not borrow to invest in these funds.

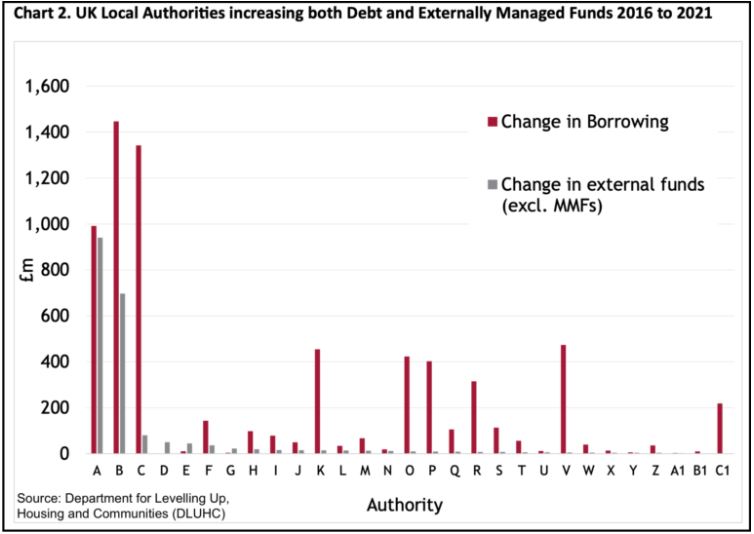

We compared data at March 2016 and March 2021 to give an insight into activity. Over the six-year period aggregate gross debt across all authorities grew by £33bn, with 289 authorities increasing debt during this period. But how many increased debt and invested in pooled funds? The data shows this happened across just 29 authorities, out of a total of more than 500, with aggregate pooled fund investment at these authorities going up by £2.1bn. The chart below provides a breakdown across these individual authorities:

Over £1.6bn of the increase in externally managed funds is attributable to just two authorities. The chart shows the remainder of activity typically involved investment of less than £10m, the minimum sum local authorities are required to hold to opt up to “professional” status under the Market in Financial Instruments Directive (MiFID).

There are some errors in the data; local authorities adopt slightly different approaches when classifying “externally managed funds”, which covers a broad range. There is also the slightly mysterious “other investments” category, described by DLUHC as investments with “rest of world banks, other securities and other investments”.

Arlingclose conducts a quarterly client investment benchmarking exercise, with responses from a quarter of the local authority universe, showing pooled fund investments at around £2bn. A breakdown by fund type is shown below.

This may not be a representative sample of all authorities, the higher investment returns achieved by Arlingclose clients suggests that the use of pooled funds is not universal. However, combined with the DLUHC data, it suggests to us that total strategic fund investments across local authorities is somewhere in the £5bn to £6bn range.

While a precise breakdown of investments is hard to pin down, the trends and figures shown above are consistent with the activity and portfolios we observe daily.

Evidence demonstrating that most local authorities take a prudent approach to debt and investment decisions comes as no surprise. Almost every meeting we hold with clients includes analysis of a carefully prepared liability benchmark and discussion of the long-term cash forecast.

Those that need to borrow do not generally invest in pooled funds, with only 5% of authorities taking out loans and increased fund exposure over the last six years.

Those that do both will usually only be investing a proportion of their strategic reserve in assets that have a longer-term investment horizon. These strategic funds normally have a risk and reward profile that give the investor a realistic chance of ensuring reserves keep pace with inflation while expected capital volatility remains within an acceptable range. The chart below shows the cumulative returns achieved over the past six years across asset classes.

The draft Prudential Code currently includes the suggestion that “authorities must not take new borrowing if financial investments for commercial purposes can reasonably be realised instead”. This suggests a hard line on the concept of “borrowing to invest” and implies authorities should always be targeting a zero cash position.

It does not appear to provide scope for authorities that may have a legitimate desire to both hold debt and a proportionate strategic investment portfolio. Drawing an analogy from personal finance, how many of us have a mortgage and a pension fund? Would we want to net this investment off against the debt?

Local authority regulators appear to concede that unwinding commercial property portfolios funded via PWLB loans will be incredibly difficult. The assets are often slow to sell, may currently be valued below the purchase price and have associated debt that would incur massive premature redemption penalties.

Lost in translation

Switching the focus to “financial investments”, a softer target in the context of relative liquidity and market value, would represent a case of mistaken identity in the investigation into crimes against the balance sheet and prudential code.

Apart from a handful of high-profile authorities, there is limited evidence to suggest the sector has been levering up to invest in externally managed funds. Where investment does take place, the majority of this is backed by a long-term investment horizon, robust investment strategy and an appropriate, and rigorous risk management framework.

When discussing the draft codes CIPFA representatives have made clear it is not their intention to prohibit sensible treasury management decisions in this area, suggesting parts of the document have been lost in translation. With the consultation not closing until 16th November there is plenty of time for stakeholders to contribute to the debate and help shape the new codes to allow sensible risk management, conducted by most authorities, to continue.