This is an Insight written by an external organisation. The following article was written by Insight Investments and represents their views.

The Big Short – winner of an Oscar for ‘Best Adapted Screenplay’ last year – was a fairly accurate retelling of key aspects of the global financial crisis. It was also notable for being the only award-winning film to feature asset-backed securities (ABS) – chiefly ‘toxic’ US subprime mortgage-backed securities – in a starring role alongside Hollywood royalty like Christian Bale.

It is impossible to talk about the ABS market without referring to the financial crisis, as it has affected demand to this day. The ‘toxic’ US subprime assets (rightly) became notorious following the crisis, tarnishing the reputation of an otherwise secure asset class.

ABS in a nutshell

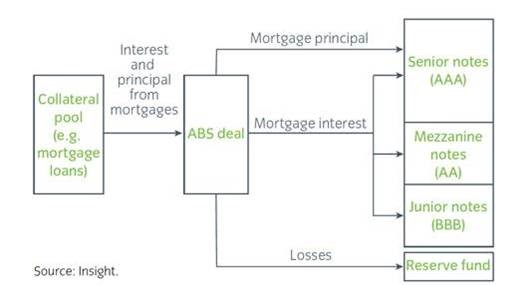

ABS are in essence, bonds whose cash flows come from underlying loans – such as mortgages or credit card obligations. Banks create ABS by taking loans they have written and structuring the loan payments to pass through directly to bondholders. They are structured so that bank’s financial position becomes legally irrelevant. The originating bank can in fact go bust and have no direct effect on the ABS assets. Not all ABS bonds have the same credit ratings. Lower-rated (or ‘junior’) bonds are the first to absorb any losses (and receive higher returns as compensation), while higher rated bonds assume losses only when their more junior bondholders have been wiped out (Figure 1).

Credit risks are therefore based on creditworthiness of the underlying mortgage or credit card borrowers (for example). Investors need to analyse and model the effect of macroeconomic scenarios such changes in economic growth, unemployment rates, property prices and interest rates and balance these results with bottom-up credit assessments of the underlying borrowers.

Not all ABS is equal

It is little-known outside fixed income investing that much of the ABS market can occupy the very opposite end of the toxicity scale from the US subprime. Similar to the public bond markets where the universe goes from high quality government bonds to high yield credit, ABS has a similar spectrum. At the higher-rated end of the spectrum lies AAA-rated UK residential mortgage-backed securities (RMBS) which has never seen a default in the history of the asset class. The UK market is notably different to the US mortgage market, as banks have the ability to pursue borrowers if the value of the house is less than the value of the mortgage (negative equity). Investors therefore have recourse to the underlying borrower, whereas in the US home owners can walk away, leaving the lender with only the underlying property to reclaim their investment.

According to analysis from JP Morgan, senior UK RMBS investments have enough protection to withstand 56 times the maximum losses experienced in the early 1990’s, the largest UK housing crisis in recent memory. A repeat of double-digit unemployment and very high interest rates is unlikely and would probably reflect a very negative environment for wider financial markets. Even in this extreme scenario, senior RMBS investments are well placed to avoid losses.

One of the most well-known UK residential mortgage facilities was set up by beleaguered UK financial institution Northern Rock – before it suffered the UK’s first bank run in 150 years in 2007 and became nationalised. The bank had funded around £50bn of UK mortgages and structured them into a series of RMBS bonds in 2005. They were placed in the market under the name ‘Granite’ – and since then arguably proved to be as tough as the rock itself. Although they suffered severe volatility during the financial crisis – neither the senior nor the junior RMBS bonds ever defaulted. The bonds were redeemed early and in full and sold to a US investor in 2011.

That investor later structured the mortgages and issued securities backed by them again, starting with a £6bn deal in April 2016. The transaction was the largest European ABS deal since the global financial crisis. This illustrates that high quality securities, backed by strong cash flows, robust legal protection and collateral can be available to those able to undertake the rigorous investment analysis that is required.

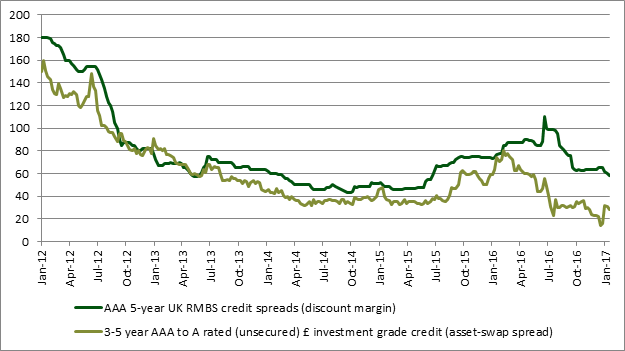

We believe the ABS market can offer arguably the most attractive source of value in liquid credit markets today. The most senior bonds quality can offer the highest credit ratings, security against tangible assets (such as property) and robust structural safeguards to maximise the probability of repayment. Despite this, the asset class frequently offers wider credit spreads than comparable lower-rated investment grade credit – which unlike ABS is a largely unsecured asset class (Figure 2). This indicates excellent relative value that can reward those with the specialist skills required to invest in the ABS market, such as detailed loan-by-loan scenario analysis and diligent credit work. In our view it is an underutilised asset class by local authorities.

{kind=link}

{kind=link}