Over recent years Arlingclose has worked with many authorities on debt refinancing transactions, often involving a premature repayment premium, but resulting in beneficial savings and risk reduction. However, we’ve seen limited activity in Scotland due to the different rules on accounting for premiums.

The Problem

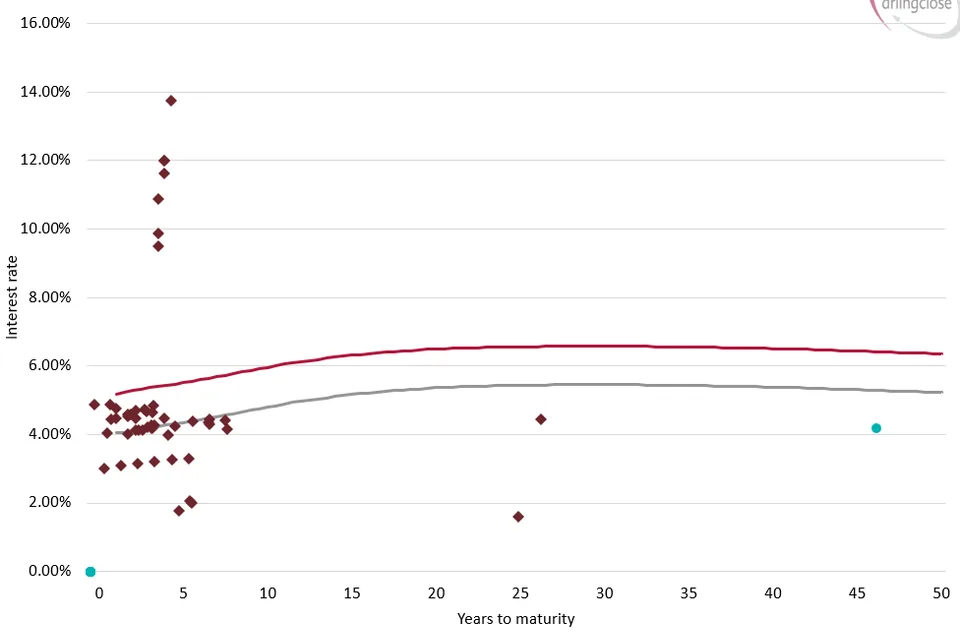

The problem we’ve seen in Scotland relates to repaying long dated debt. In England, Arlingclose clients have actively replaced long-term Lender’s Option Borrower’s Option (LOBO) debt with fixed rate PWLB loans. Removal of lender’s options has reduced refinancing risk, while securing lower cost debt has produced interest savings. Premiums are generally spread over the life of the existing loan. LOBO debt at 4% or 5% has been extinguished and typically replaced with fixed rate debt at 1% or 2%, a great outcome, especially given the now increased probability of LOBO “calls”.

Replacement loans used in refinancing are often shorter than existing loans, with liability benchmarks suggesting that many local authorities are holding more long-term debt than required. Refinancing with amortising loans over a shorter period has helped match the aggregate debt profile to the underlying need to borrow.

This hasn’t happened in Scotland as, in contrast to England, premiums need to be spread in line with interest payments on the replacement loan. Generally, when long dated debt is repaid, spreading premiums over shorter amortising loans will result in costs in the early years, with savings not materialising until much further down the line. In Scotland, the upshot is long-term debt prepaid with a premium would need to be replaced with long-term maturity loans, severely diminishing refinancing choice and benefits.

Modern Treasury Management

Much has changed since the current Scottish statutory guidance were introduced in 2007. The CIPFA Prudential Code, introduction of the liability benchmark, and tighter rules on investments all encourage prudent treasury management, rather than the speculative punts and short-term accounting wheezes that some may have adopted previously.

Time for a change?

Is the system in Scotland still fit for purpose? While some debt restructuring transactions have taken place, for example, the successful conversions of more exotic LOBO structures, there has been limited progress on reducing the pile of “vanilla” LOBOs north of the border. Perhaps it is time that the Scottish Government reviewed existing arrangements to enable authorities to repay and refinance debt more flexibly?

Arlingclose provide a range of services to help authorities develop and implement funding strategies, if you would like to find out more, please contact dblake@arlingclose.com

Related Insights