Credit cards getting locked-down?

With the release of Bank of England consumer lending figures for March, it is possible to see the immediate and dramatic impact that the COVID-19 pandemic has, and will likely continue to have, on consumer spending and saving.

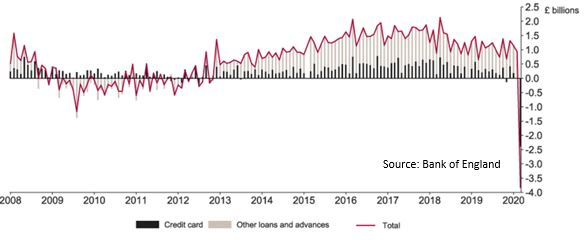

In March consumer credit fell by £3.8 billion, the largest drop since August 2009 when the equivalent figure declined by £1.1 billion. The March 2020 fall in net lending was primarily driven by a reduction in new borrowing (-£5.4bn) compared to February - repayments were actually £1.3bn lower. The impact of weak consumer credit in March meant the annual growth reduced to 3.7%. The annual growth in credit card lending, a subset of overall consumer credit, turned negative at -0.3%, the first negative reading since the series began in 1993.

As various data have shown, the effect of the UK lockdown measures put in place to slow the spread of COVID-19 has prompted a recalibration of economic activity that is similar but on a greater scale than that seen during the financial crisis, 12 years ago. The fall in net lending also mirrors and magnifies the reaction of August 2008 as a response to the financial crisis.

If the situation continues to follow that of the financial crisis, we may see consumer credit continue in negative territory over the next months and maybe years as was the case throughout late 2009 – 2013, following a significant hit to consumer confidence and a rise in unemployment. This is particularly likely when we consider that the massive decline in net lending in March 2020 only encompasses the first two weeks of lockdown measures being in place. It is possible that with the release of April’s figures (when the lockdown measures will have been in place for over a month) that we will see an even more substantial reduction in both lending to consumers and repayments.

While there are similarities between the situation now and in 2008 with dramatically lower levels of consumer confidence and lending, the situation does vary with respect to the availability of credit. Banks were forced to cut lending to individuals and each other due to a lack of liquidity in 2008, whereas now we seem to have an abundance of credit with businesses and local authorities borrowing record amounts in March. The Bank of England has been particularly active in seeking to maintain liquidity and credit flows. So if the issue isn’t supply, then it must be demand. Undoubtedly consumers are less confident, therefore making them less keen to take on debt and make repayments despite effective rates being extremely low. After almost a decade of deflated interest rates, maybe the UK consumer has become desensitised to these low rates as an incentive to borrow.

But with nothing but time on our hands to shop why has credit card lending dropped so dramatically? And what does this £3.8 billion downshift say about our spending and saving decisions? The answer could lie with the simple inability of consumers to make discretionary purchases. With high streets effectively shut, a quarter of UK businesses shut down and those that remain open facing severe supply chain disruptions as well as the difficulty of implementing social distancing measures, spending options are more limited.

With consumers confined to their homes, March’s car sales (typically one of the strongest months of the year) plummeted 44% while Barclays reported other travel expenditure falling by 40.5%. With no holiday destinations to travel to and no high streets to shop on, consumers are forced to find alternatives to satisfy at least some of their usual spending habits. A 17.4% increase in purchases of digital content and subscriptions as well as increased spending in local specialist food and drink stores (including off-licenses) may give some context as to how people are staying entertained and spending during lockdown. But there is only so much TV we can watch. Although some sectors may have seen mild increases in spending, 71% of retailers said that activity was down compared with a year earlier and this lull in activity is reflected in weak net lending.

The varied coronavirus impact is also indicated by the reduction in loan repayments, which is hidden to some extent by the larger fall in new lending. Budgets are stretched thin across the country as businesses are forced to lay off employees and even those who are not let go may find their salary reduced to 80% of normal as part of the government furlough payments. As a result, we are seeing payment holidays being offered by banks and credit card providers as households focus on more immediate concerns and adapt to lower household income. As with the drop in new borrowing, the longer the lockdown continues, the lower debt repayments are likely to be.

The effects of the coronavirus pandemic have certainly been a shock to the consumer economy. With confidence continuing to weaken and many people’s finances moving into perilous territory, we must wait and see if the Prime Minister’s speech at the weekend will provide a clear path to reopening the economy as promised.

-960x640.webp&w=3840&q=75)