As we mentioned in one of our recent updates to our clients, earlier this month the Bank of England published its first resolvability assessment of major UK banks. The report is part of its Resolvability Assessment Framework which the Bank, as the resolution authority, undertakes to evaluate whether banks can fail in an orderly way, overcoming the problems of the financial crisis where some banks were deemed ‘too big to fail’.

The report (which can be found here) covers the BoE’s assessment of Barclays, HSBC, Lloyds, Nationwide, NatWest, Santander UK, Standard Chartered, and Virgin Money. It shows that in a resolution, customers would be able to access their accounts and business services as normal, with any losses and the cost of recapitalisation being paid for by shareholders and other investors via a bail-in.

The report showed that while all eight deposit takers are in a much better place than in the global financial crisis, there were still improvements that could be made. There were no pass-or-fail judgements, and different business models and resolutions strategies mean direct comparisons are not possible.

No serious issues were identified, but the report identified areas where some firms were deemed to require additional work to meet BoE expectations. Some were classified as ‘shortcomings’, which may complicate the Bank’s ability to undertake a resolution, and some others an ‘area for further enhancement’ which covers specific areas where extra work is needed to reduce the risks associated with resolution.

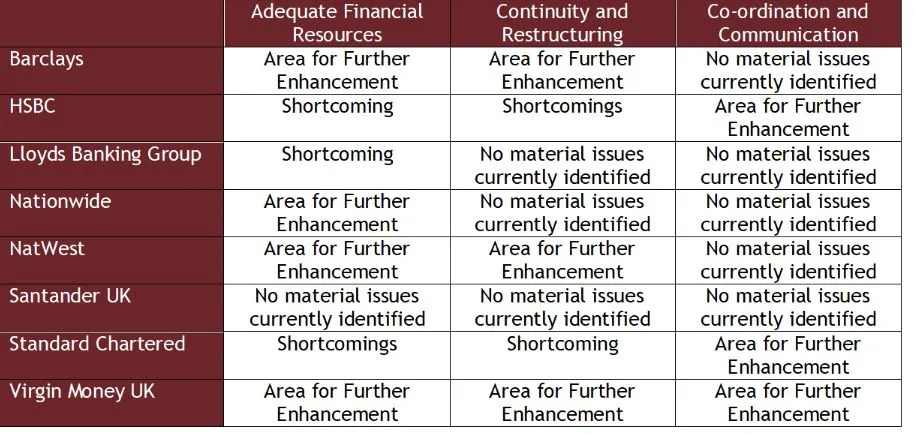

The bank specific findings were broken down into three main areas:

· Adequate financial resources – does the bank have sufficient resolution-ready financial resources to absorb losses and recapitalise itself with exposing public funds to loss?

· Continuity and restructuring – can the bank continue activities while a resolution is executed?

· Co-ordination and communication – can the bank ensure that during a resolution its governance arrangements provide effective oversight and decision-making to deliver suitable and effective communications to staff and other stakeholders?

The results are shown in the table below.

The report represents a snapshot in time but is also part of an ongoing process to ensure the UK resolution regime is and remains effective. The BoE will undertake a similar assessment every two years, ensuring the eight banks address the issues identified and their preparations remain ready if the need to implement the measures ever arise, which of course we all hope is never the case.

Related Insights

Can we bank on the banks? Part 2.